March 2025 VCM Updates: Section B

This article is an automatically translated version of the original Japanese article. Please refer to the Japanese version for the most accurate information.

This is sustainacraft Co., Ltd.'s newsletter. This article is Section B (Trends in major international regulations) of VCM Updates (Voluntary Carbon Market updates).

This article covers the following topics:

- Public Consultation for Verra Scope 3 Standard (S3S) Program Begins

Keywords: Scope 3, Inset

Introduction

Verra has launched a public consultation for its **S3S (Scope 3 Standard) Program**.

The S3S Program, while detailed in the main body below, may give corporate representatives the impression that it involves quite complex procedures. Compared to typical Carbon Credit projects, the **Additionality** requirements are significantly relaxed, and quantification is designed to align with corporate GHG reporting timelines for low-burden annual implementation. However, **Removal** activities still require 40 years of **Reversal** monitoring. For companies not previously involved in Carbon Credit project development, it is anticipated that many will find the utilization of the S3S Program, at least at this stage, to be a high hurdle.

If you are in the beverage, food, or FLAG sector, or a company with **AFOLU**-related Scope 3 emissions considering the use of the S3S Program, please feel free to contact us here.

Why, then, would a carbon standard like Verra implement a Scope 3-related program, which is typically part of a company's internal **GHG Inventory**? Verra has been developing S3S since 2022.

This is related to past criticisms of "**Inset**" (in contrast to "**Offset**"). Specifically, criticisms include a lack of clarity on how to determine whether an activity is "within the **Value Chain**" and how to quantify the impact of interventions on the **Value Chain**, with cases where **Offset** and **Inset** are **Double Counted**.

Based on the "**SBTi**" methodology, if an activity is not considered to be within the **Value Chain**, it should be treated as **BVCM (Beyond Value Chain Mitigation)**. Furthermore, the current global standard for determining whether an activity is considered "within the **Value Chain**" is to follow the "**GHG Protocol**."

The GHG Protocol for the Land Sector is currently scheduled for release in Q4 2025, so we need to await further details. However, based on the materials released so far, a very high level of traceability seems to be required. These traceability requirements will also influence what types of environmental attribute certificates (energy certificates or commodity certificates) are accepted by SBTi.

The above topic was explained to some extent in our previous seminar here, so please refer to it. Additionally, we will be holding a webinar on April 22nd to explain the new **Corporate Net Zero Standard** Version 2 released by SBTi, as detailed below. Please register to attend.

Announcement: SBTi CNZS Version 2 Explanatory Webinar

The **Science Based Targets initiative (SBTi)** has released a draft of its **Corporate Net Zero Standard** Version 2.0. This is the first major update, with revisions being considered from various perspectives, including Scope 3 target setting, the use of environmental attribute certificates including **Carbon Credits**, setting interim targets for **Removal**, and measures to promote **BVCM (Beyond Value Chain Mitigation)**.

Please find more details and register here.

Public Consultation for Verra Scope 3 Standard Program (S3S) Begins

(source)

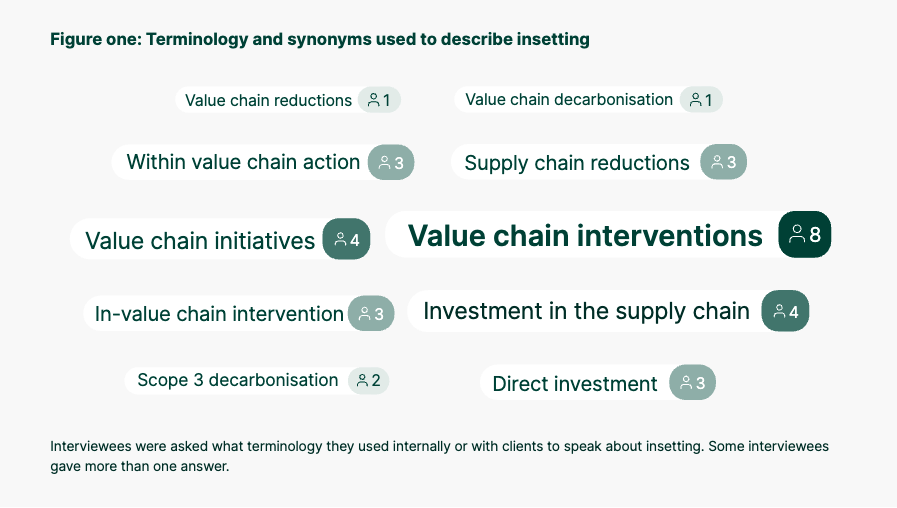

Recap on Scope 3 / Inset

The lack of progress in Scope 3 reductions has been noted across many industries. Scope 3 reductions are part of a company's internal **GHG Inventory**, and interventions within the **Value Chain** (aimed at reducing emissions) to achieve Scope 3 reductions are referred to as "**Inset**."

**Inset** is a term coined in contrast to "**Offset**," but the lack of a clear definition has been identified as a problem.

For example, the following observations:

From New Climate Institute & Carbon Market Watch: Corporate Climate Responsibility Monitor (2023) (link):

"Offsets disguised as 'insets' are gaining traction and legitimacy, but this practice leads to **low credibility for offset claims and Double Counting of Emission Reductions**... (omission)... 'Inset' is a business-driven concept with **no universally accepted definition**. While some companies advocate 'insetting' as an alternative to offsets, the insetting we have observed effectively amounts to unregulated offsets for emissions."

From Mongabay: “Companies eye ‘carbon insetting’ as winning climate solution, but critics are wary” (link):

"Companies currently using insets, such as Nestlé and PepsiCo, state that this approach allows for better control to reduce **GHG** emissions, fosters greater responsibility and accountability, and helps reduce their **Carbon Footprint**. Independent researchers question whether this process, similar to issues surrounding **Carbon Offsets**, **lacks independent oversight, unified high standards, and scientific rigor**. Some even suggest that insets could be weaker than traditional offsets."

"Both offsets and insets risk utilizing erroneous accounting methods, leading to **Double Counting** of accumulated carbon."

With these challenges in mind, **Carbon Credit** standards like Verra and Gold Standard have been developing programs designed to use **Carbon Credits** to enhance the integrity of Scope 3 (**Value Chain**) reductions.

For Verra, this is the **S3S (Scope 3 Standard) Program** introduced here. A significant amount of work has been invested in S3S, and the program is still expected to take some time before it launches.

Interim Measure: Introduction of "corporate emissions inventory accounting" as a Retirement Reason

As a provisional measure until the S3S Program becomes operational, the option of "**corporate emissions inventory accounting**" was introduced as a **Retirement** Reason in October 2023 (link).

This is an **interim measure** until S3S begins. By selecting this reason, companies can indicate that the **Emission Reductions** or **Removals** represented by the retired VCUs are being used for their corporate emissions **Inventory** accounting. This is intended to reduce the risk of **Double Counting** (where the same VCU is used as an **Offset** and accounted for in a company's emissions **Inventory**).

However, a disclaimer is also included, stating that "it does not verify that the **Emission Reductions** or **Removals** occurred within a specific company’s emissions inventory boundary, nor that the **Emission Reductions** or **Removals** were appropriately accounted for within the company’s emissions inventory. As an independent standard setter, Verra does not provide any assurance or **Verification** of any claims made regarding the use of retired or canceled VCUs." This remains merely a provisional measure.

This **Retirement** reason has not been used very actively so far; as shown below, retirements amount to only about 20-25k **tCO2** per year. Furthermore, the majority of these are unlikely to have occurred within the **Inventory** boundaries of the retiring company.

As an example of its intended use, Nestlé, which has long been engaged in **Inset** activities, can be cited. Based on project information, it appears that Nestlé is retiring **Carbon Credits** generated from projects that reduce **Methane (CH4)** emissions from livestock within its **Value Chain** processes. In this way, companies can demonstrate that the **Greenhouse Gas Emission Reduction** effects obtained from interventions within their **Value Chain** are processed in accordance with **Carbon Standard Methodology** and undergo third-party **Verification**(*).

(*) However, as mentioned above, this **Retirement** reason does not guarantee whether it is correctly accounted for in carbon accounting.

About the S3S Program