Latest Developments: Non-Carbon Benefits, Including Biodiversity Credits

This article is an automatically translated version of the original Japanese article. Please refer to the Japanese version for the most accurate information.

This is Sustainacraft Inc.'s Newsletter (Special Edition). This time, focusing on **non-carbon benefits**, we would like to introduce some long-standing discussions on the **diverse values of nature and their valuation**, as well as recent discussions on biodiversity credits and related topics.

First, let's start with the underlying issues. Many projects with high carbon benefits are promoted through the current carbon finance framework using Carbon Credits. However, there are also many activities where carbon benefits alone are not sufficient for the current Carbon Credit trading prices to enable their implementation (i.e., the financing is insufficient).

Specifically, examples include activities such as converting coniferous monoculture plantations to mixed coniferous-broadleaf forests in Japan. Unlike purely coniferous plantations, mixed coniferous-broadleaf forests are reported to have higher value in terms of species composition richness, biodiversity, and water resource conservation compared to monoculture plantations. However, such activities have higher management costs compared to promoting thinning in coniferous plantations, but from a carbon benefit perspective, the difference is not that significant, often leading to a scenario where they are not chosen.

Even in international projects, when comparing monoculture afforestation activities with rainforest restoration or forest Deforestation / Forest Degradation Avoidance projects like REDD+, there are often significant differences from a biodiversity perspective. Even within the current framework, for example, Verra offers a CCB (Climate, Community & Biodiversity Standards) label, and Gold Standard afforestation projects sometimes require the planting of indigenous tree species as part of their Methodology. However, these are merely value-added labels, and whether the value of biodiversity is ultimately reflected in the Credit trading price is questionable, as they don't have that much impact.

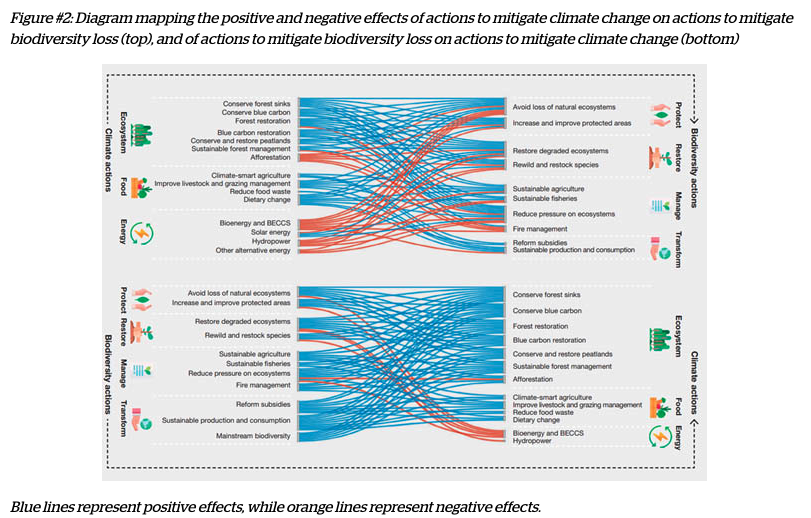

An eco-act article introduces reports from IPCC and IPBES, emphasizing the importance of considering biodiversity, as initiatives solely aimed at decarbonization often lead to biodiversity loss. The graph below indicates that **Climate Action (climate change countermeasures from a decarbonization perspective) often has negative impacts from a biodiversity perspective** (corresponding to the prevalence of orange lines in the upper section), whereas **biodiversity measures often have positive impacts from a decarbonization perspective** (corresponding to the prevalence of blue lines in the lower section).

In this context, discussions on **biodiversity credits**, rather than Carbon Credits, have recently become active. In this newsletter, within the above context, we would like to introduce the following topics.

Diverse Values of Nature and Valuation Methodologies

1) IPBES: Assessment Report on the Diverse Values and Valuation of Nature

2) TEEB: The Economics of Ecosystems and Biodiversity

3) Results of Nature Valuation in Japan

Recent Discussions on Biodiversity Credits

1) Biodiversity Credit Markets —The role of law, regulation and policy—

2) Verra's SD VISta, and the Nature Framework Development Group established under SD VISta

Recently, there was news that a **Swedish bank purchased Europe's first biodiversity credit** (Article on Methodology). The mainstream discussion lately is that biodiversity credits will not be used as Offsets. Unlike Carbon Credits, quantifying non-carbon benefits varies in mechanism by project and is difficult to Monitor. However, we believe it is crucial to create actual transaction examples, even on a small scale, like this case.

Looking at examples like the standalone SD VISta project in London introduced below, by utilizing a framework that considers non-carbon benefits, projects that have positive environmental impacts but were previously difficult to implement due to execution costs or other factors might actually become feasible.

Our ideas can inevitably become narrow if we rely solely on our own perspective. Therefore, we encourage everyone to think flexibly and would be grateful to hear any opinions you may have, such as whether a certain idea could potentially become a project.

Diverse Values of Nature and Valuation Methodologies

First, we will introduce some of the approaches to valuing ecosystems and biodiversity that have been researched to date, as compiled on the Ministry of the Environment's website here.

Discussions on non-carbon benefits and biodiversity credits are flourishing recently, but how have the diverse values of nature been assessed so far? Various approaches have been proposed, each with its own strengths and weaknesses. Although this might delve into a slightly academic perspective, understanding which direction the currently discussed biodiversity credits are heading among these proposed approaches is crucial for considering their business impact.

1) IPBES: Assessment Report on the Diverse Values and Valuation of Nature

(link)

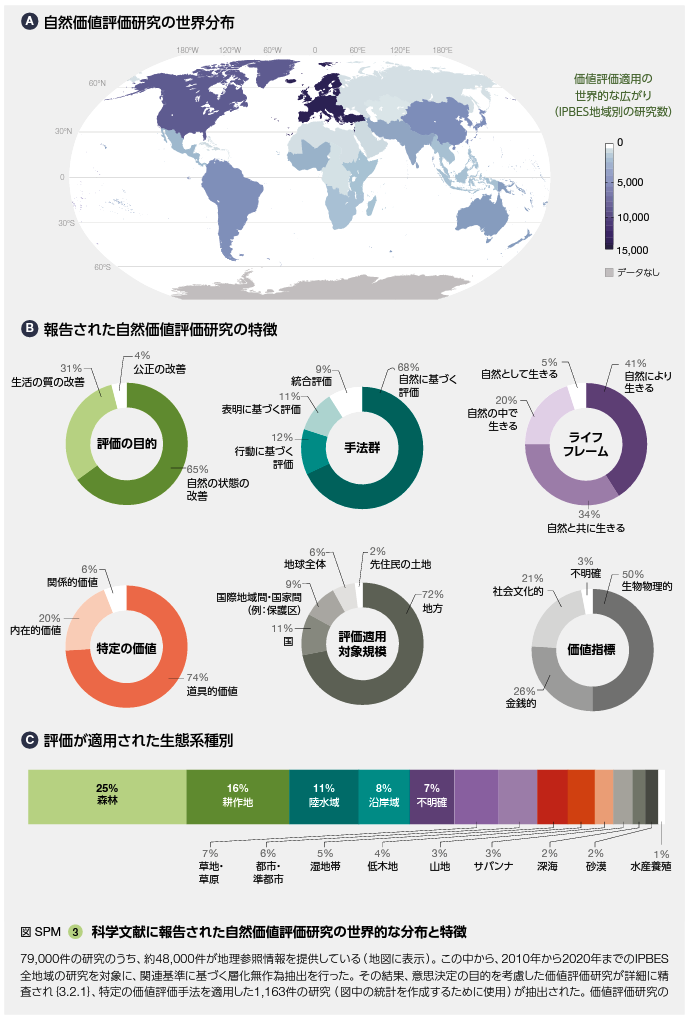

First, we introduce the IPBES report, which systematically organizes various approaches developed to date.

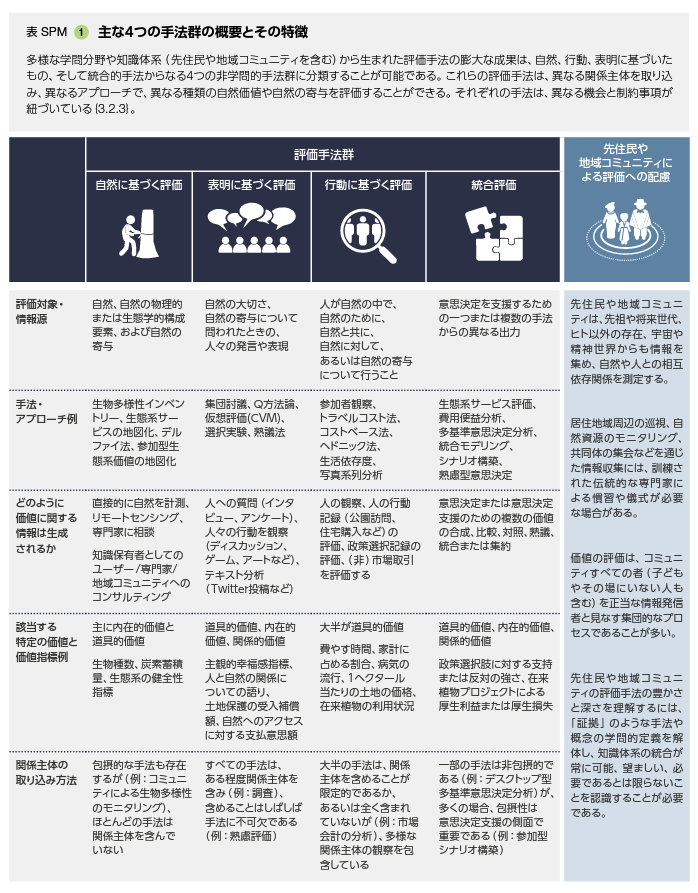

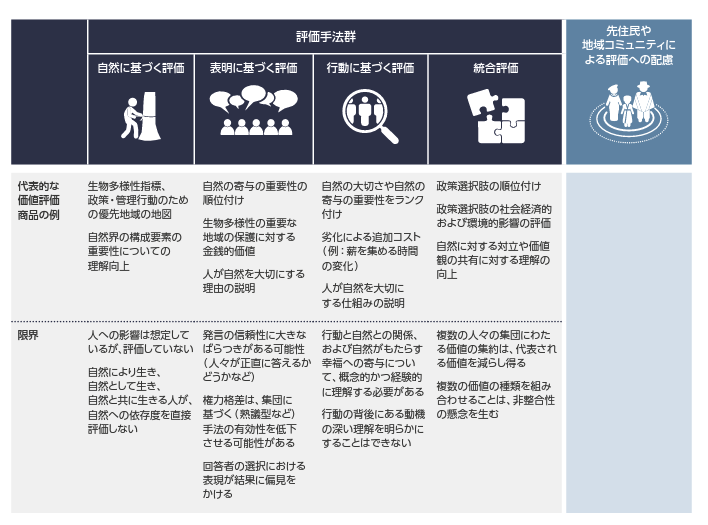

The global distribution of nature valuation, the number of research papers per approach, and an overview of each are clearly organized in the figures and tables below. Here, please pay particular attention to the four methods: **Nature-based Assessment, Expressed Preference Assessment, Revealed Preference Assessment, and Deliberative/Integrative Assessment**, and their respective overviews.

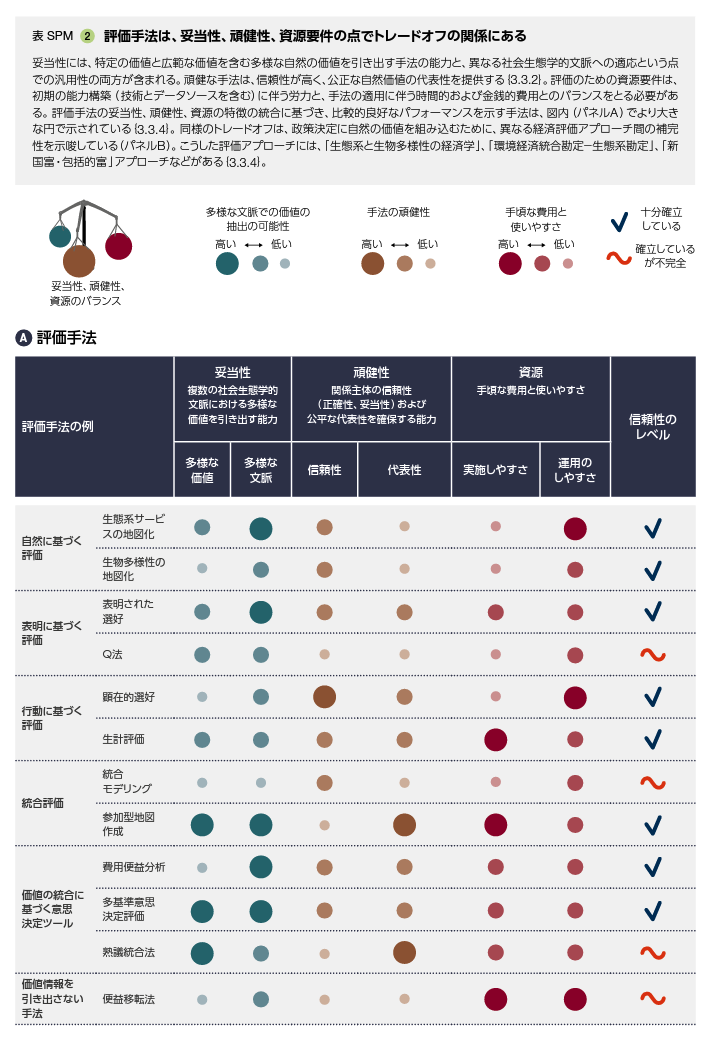

As shown in the last image, it is important to understand that valuation methods involve trade-offs in terms of legitimacy, robustness, and resource requirements.

2) TEEB: The Economics of Ecosystems and Biodiversity

The "Economics of Ecosystems and Biodiversity (TEEB)" report is sometimes referred to as the "biodiversity version of the Stern Review." It compiles the results of global-level research on biodiversity loss from an economic perspective. It is also covered in the IPBES report mentioned above, where TEEB is positioned as having high legitimacy (the ability to elicit diverse values in multiple socio-ecological contexts) but low reliability within robustness (the ability to ensure the credibility (accuracy, validity) and fair representation of stakeholders).

For details, IGES has published a Japanese translation of the TEEB report, which you can refer to via the details link above. The Ministry of the Environment has also compiled a pamphlet, which is recommended. You can refer to the latter via the overview link.

A key feature of the TEEB report is its abundant case studies.

For example, on a global scale, it is estimated that "the value of natural disaster damage mitigated by halving the rate of Deforestation by 2030 is 3.7 trillion USD" and "the economic value from insect pollination of crops in one year in 2005 was 153 billion Euros." Local results also show, for instance, that "the restoration of 12,000 ha of mangrove forests in Vietnam reduced dike maintenance costs by 7.3 million USD (while the cost of mangrove restoration was 1.1 million USD)."

3) Results of Nature Valuation in Japan

(link)

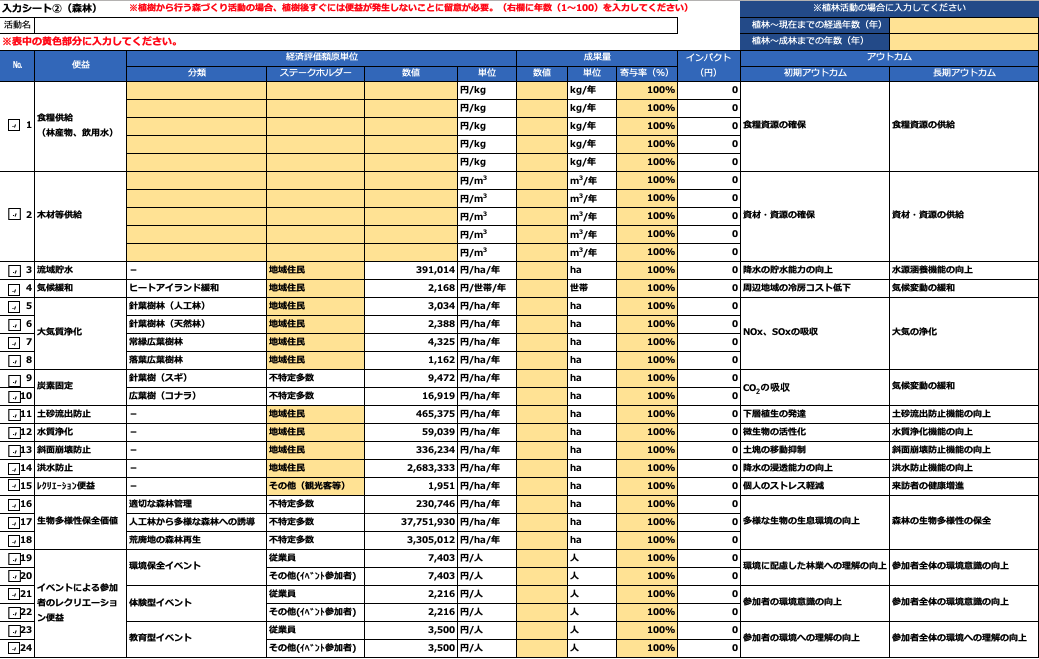

Here, we will primarily introduce the section "FY2017 Valuation of Ecosystem Services Related to Corporate Biodiversity Conservation Activities (March 31, 2019)" regarding the valuation of ecosystem services related to corporate biodiversity conservation activities, prepared by the Ministry of the Environment.

Here, multiple approaches such as Nature-based Assessment and Expressed Preference Assessment are incorporated and evaluated for each item. The assessment and calculation sheet published at the link above is as follows for forests, for example.

Here, the targets for "Carbon Credit" and `Climate` in TCFD refer to benefits equivalent to "carbon sequestration" benefits. The remaining parts are non-carbon benefits, falling under the `Nature` domain as defined by TNFD. As this sheet illustrates, carbon benefits constitute only a small fraction of the total.

While details can be found in the report mentioned above, here we will briefly introduce how some of these benefits are calculated and evaluated.

For example, the item "Carbon Sequestration Benefit > CO2 Storage Function by Forests" is calculated using a commonly seen approach in forest credits (multiplying trunk volume growth by various parameters, here calculated at ¥2,890/tCO2) as follows:

Coniferous trees (Sugi): 2.9×0.314×1.57×1.25×0.5×44/12×2,891 =9,472 JPY/ha/year

Broadleaf trees (Konara): 2.9×0.624×1.40×1.26×0.5×44/12×2,891 =16,919 JPY/ha/year

On the other hand, the item "Biodiversity Conservation Value > Securing Habitat for Wildlife (Appropriate Forest Management)" is calculated at **230,746 JPY/ha/year** using a "Expressed Preference Assessment" method called Contingent Valuation Method (CVM).

Among forests, the next item, "Biodiversity Conservation Value > Securing Habitat for Wildlife (Guiding from Plantations to Diverse Forests)," shows a particularly large figure, which is also based on the Contingent Valuation Method (CVM), with a value set at **37,751,930 JPY/ha/year**.

As described above, the valuation and calculation involve a combination of multiple approaches. As introduced earlier, we recommend using this tool after understanding the overview of each approach.

Recent Discussions on Biodiversity Credits

1) Biodiversity Credit Markets —The role of law, regulation and policy—

(link)

We introduce a report released by the Taskforce on Nature Markets in April 2023. This report discusses the requirements for creating and governing a high-integrity biodiversity credit market. While much of the discussion is high-level, here we will introduce the concept of a "basket of metrics"1.

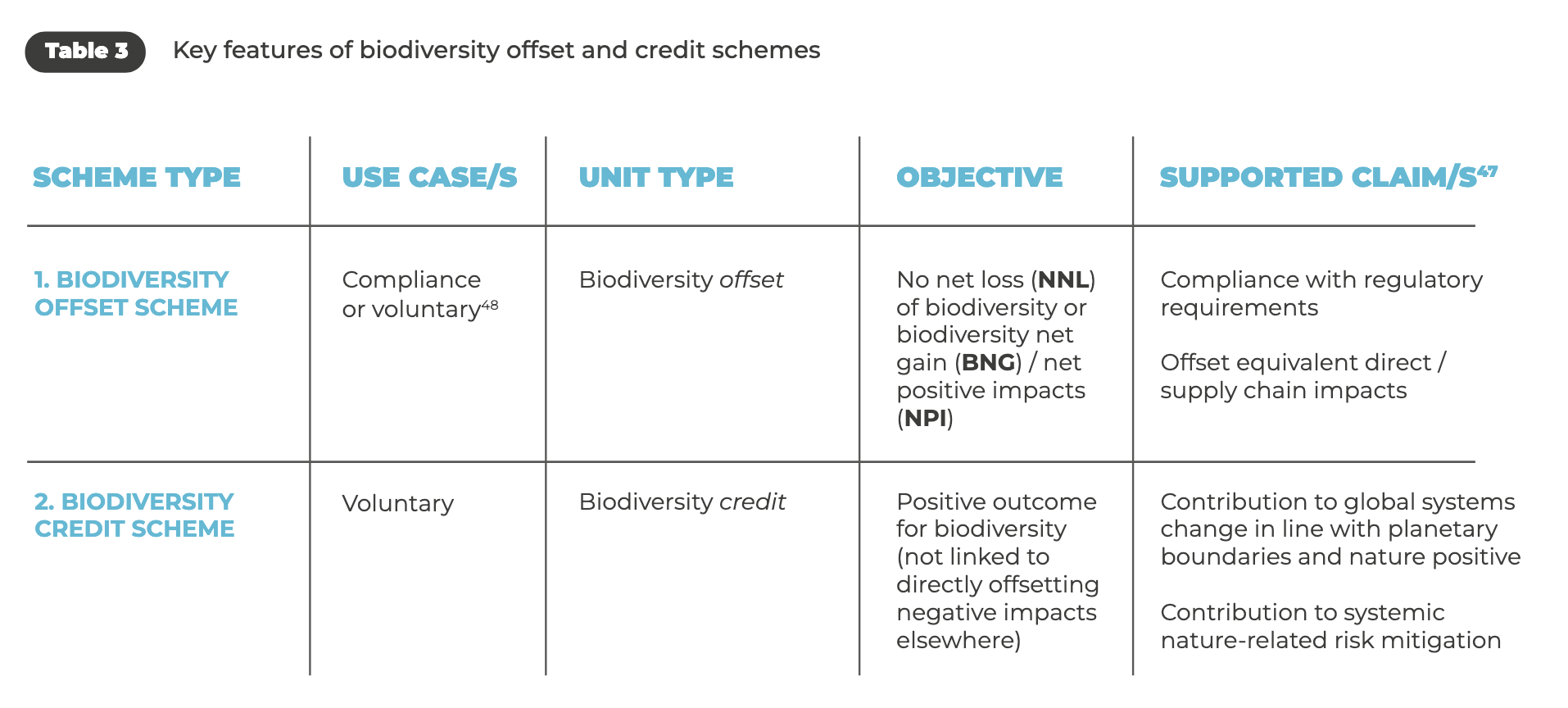

First, before that, an explanation of "**Offset Schemes**" and "**Credit Schemes**." In an "Offset Scheme," the idea is to "offset" a negative impact on biodiversity in one location by purchasing biodiversity units corresponding to a positive impact on biodiversity in another location. In a "Credit Scheme," offsetting is not intended; rather, it aims to secure "true" biodiversity benefits that are not linked to negative impacts elsewhere. The mainstream discussion currently is that biodiversity credits are not Offsets. Unlike carbon, biodiversity is local, and offsetting biodiversity loss in one place with biodiversity gain in another is inherently problematic. There is also the challenge of relatively assessing the degree of biodiversity in different locations.

As summarized in Table 3 below, Offset Schemes set "Net" objectives, such as NNL (No Net Loss) or BNG (Biodiversity Net Gain), which presuppose offsetting. In contrast, Credit Schemes aim for a Positive Outcome (not Net).

As mentioned above, it is difficult to relatively evaluate the degree of biodiversity in different locations. In response, the concept of a **basket of metrics** has been proposed. Regarding the "basket of metrics," rePlanet describes it as something akin to a consumer price index (CPI) for the natural world. CPIs, while measuring different goods and services in each country, account for what is actually purchased in those countries, and by indexing their time-series changes, they become globally comparable. A similar idea is thought to be applicable to biodiversity units. Even if the set of metrics differs by location, quantifying their changes over time is believed to create a globally usable biodiversity indicator.

2) Verra's SD VISta: The Sustainable Development Verified Impact Standard

(SD VISta)

In this newsletter, we have often covered Verra's VCS (Verified Carbon Standard). Here, we will introduce **SD VISta (Sustainable Development Verified Impact Standard)**, a program announced in 2019 for projects aimed at delivering sustainable development benefits.

SD VISta can generate three types of outcomes, but the mainstream approach so far has been its use as a **Label**, where a **SD VISta label** is attached to the issued VCU (Verified Carbon Unit). As of the time of writing, there is no track record of tradable **Assets** being issued as standalone units.

Claims: A claim is a verified statement of a project’s measured benefits. All SD VISta projects may generate claims about their contributions to sustainable development. Verified claims enable credibility, facilitate investment, and safeguard against accusations of greenwashing.Labels: A label is a marker affixed to a social or environmental credit. It demonstrates that the project that generated the credit is also verified to SD VISta, thus increasing the unit’s market value.Assets: An asset is a tradeable credit that represents a unique sustainable development benefit that has been quantified through an SD VISta methodology. Asset buyers can make verifiable claims for impact or SDG reporting.

A summary flyer available here states that over **29 million** SD VISta-**labeled** VCUs (Verified Carbon Units) have been issued to date. The majority of these are from the following three large-scale AFOLU (Agriculture, Forestry and Other Land Use) projects, with Indonesia's Rimba Raya project alone accounting for over **17 million**, more than half of the total.

- 674: RIMBA RAYA BIODIVERSITY RESERVE PROJECT (Indonesia)

- 607: Darkwoods Forest Carbon Project (Canada)

- 1748: Southern Cardamom REDD+ Project (Cambodia)

Rimba Raya has a project area of approximately 65,000 ha, with annual Emission Reductions of about 3.5 million tCO2, resulting in an annual Credit Issuance of around **50 tCO2** per hectare. This large amount of Emission Reductions per hectare is a characteristic of Peatland Restoration and Conservation (WRC) projects. Although it carries the SD VISta label, most of its economic value is attributed to carbon benefits, suggesting it is a type of activity where the existing framework of Carbon Credits is effectively working.

Meanwhile, new developments are emerging. Notably, as introduced here, a standalone SD VISta project has been registered. This project (2488), named The Human Forest Mobility Project, is being carried out by Human Forest in the UK and is not an AFOLU project. Since this project does not issue VCUs, the value for carbon benefits will not be traded; instead, it is expected that SD VISta Assets will be traded.

HumanForest , an electric bicycle hire operates in the United Kingdom in the city of London, specifically in the boroughs of Islington and more recently Camden. HumanForest allows the user to borrow an e bike for free for short journeys thus helping the user avoid crowded public transport or taking a more carbon intensive mode of transport such as the car. The purpose of the project is to share and transport people efficiently in an environmentally friendly manner. HumanForest is a unique project that may generate benefits in terms of the planet, people, and their prosperity.

Additionally, SD VISta has currently launched the SD VISta Nature Framework Advisory Group, which is developing biodiversity Methodologies.

Closing remarks

This time, we introduced the topic of how to value the diverse benefits of nature, focusing on non-carbon benefits.

The "basket of metrics" in biodiversity credits, introduced in the latter half, appears to be moving more towards a "Nature-based Assessment" approach, rather than "Revealed Preference Assessment" or "Expressed Preference Assessment" approaches introduced earlier.

However, on the other hand, the Biodiversity Credit Alliance, launched at last year's CBD COP15 (15th Conference of the Parties to the Convention on Biological Diversity), states that VBCs (Voluntary Biodiversity Credits) do not put a price on nature itself, but rather "put a price on the human labour and technology cost to cause biodiversity conservation and/or enhancement."

VBCs do not put a price on nature, but instead put a price on the human labour and technology cost to cause biodiversity conservation and/or enhancement.

Furthermore, how will the "basket of metrics" to be used for each project be determined? And can it be uniformly decided for each ecoregion, in a way that effectively expresses the individuality of each project? Moreover, how will the market be shaped so that Buyers can also understand it? Many things need to be considered.

However, what is important is to start such initiatives now. It is clear that there are activities where carbon benefits alone do not generate sufficient funding. Quantifying non-carbon benefits is challenging, and the meaning for companies to purchase biodiversity credits that are not Offsets is still unclear. However, this is precisely the role a "**Voluntary**" market should play, we believe. It is crucial to start concrete projects, even small ones, and have Buyers perceive value and send price signals to the market, thereby creating a framework where funding also circulates for non-carbon benefits.

In summary, this time we introduced discussions concerning non-carbon benefits.

Our company profile materials are available here, please refer to them.

Disclaimers:

This newsletter is not financial advice. So do your own research and due diligence.

The report also introduces many case studies of existing Offset/Credit Schemes, so please refer to it if interested. ↩