September 2024 VCM Updates: Section A

This article is an automatically translated version of the original Japanese article. Please refer to the Japanese version for the most accurate information.

This is the sustainacraft Inc. newsletter. This article is Section A (Market Trends) of VCM Updates (Voluntary Carbon Market Updates).

«Structure of VCM Updates»

A. Voluntary Carbon Credit Market Trends ← Subject of this article

- Analysis of Credit Issuance, Retirement, and Investment Trends

- Project Pipeline Analysis

B. Trends in Major International Regulations

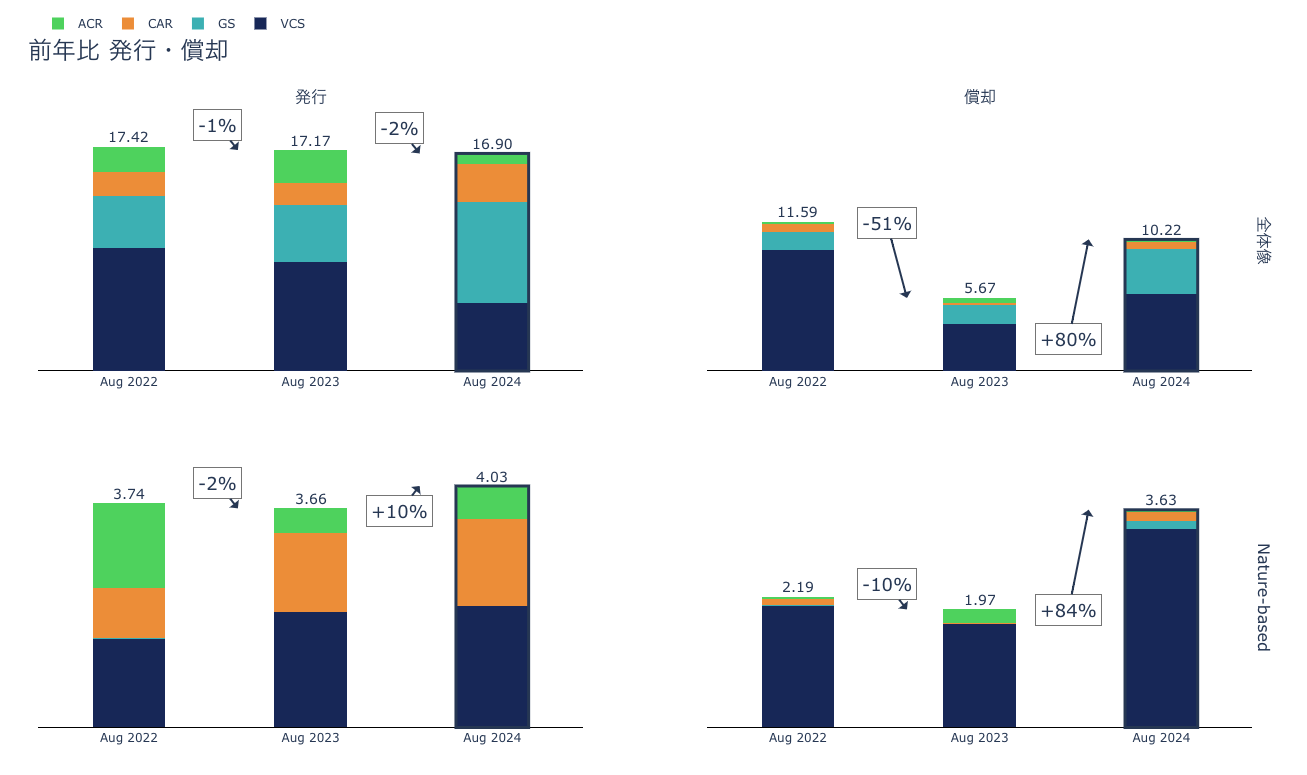

Regarding issuance and Retirement trends, Retirement still largely consists of Verra REDD+ projects, while Issuance from Gold Standard is increasing. Issuance of Nature-based Solutions (NbS) projects, including CAR IFM projects from North America and Mexico, is also increasing, indicating a trend of more "Removal" type Credits entering the market. Furthermore, in terms of Investment trends, significant investments in projects such as forest regeneration have been announced by the energy and aviation sectors, following the high-tech industry.

Regarding Carbon Credits, when we look at these three transactions – Retirement, Issuance, and Investment – for companies utilizing them, 'Retirement' represents past procurement, 'Issuance' represents current (recent) procurement, and 'Investment' represents future-oriented procurement. Without signs of investment, projects cannot secure financing, meaning Credits would not be issued in the first place. The fact that the Issuance of Removal Credits is already increasing suggests that a considerable amount of investment has already begun to flow (especially for Afforestation, Reforestation and Revegetation projects, which require initial financing).

As use cases for Credit Retirement by companies last month (August 2024), we introduce three cases: EY (and general trends in the consulting industry), SkyRiver (a casino resort in California), and the Paris 2024 Olympics.

- The consulting industry is strengthening its procurement of Removal Credits, and multiple companies have obtained the Carbon Integrity Platinum Claim for Buyers issued by VCMI. Regarding VCMI's new claim labels for Scope 3, please refer to this month's newsletter (VCM Section B), where they are introduced.

- SkyRiver uses Credits as mitigation based on the U.S. NEPA (National Environmental Policy Act), making it a different use case from voluntary Credit utilization.

- The Paris 2024 Olympics attracted attention from a Carbon Dioxide Emission perspective, for instance, by discontinuing the use of the term 'Carbon Neutral' (partway through) in its environmental claims. We held a seminar on this topic on August 9th, so if you are interested, please register for the archived webcast from here.

A. Voluntary Carbon Credit Market Trends (Verra)

A-1: Credit Issuance and Retirement Trends

``` - Registries analyzed: Verra, GS (Gold Standard), CAR (Climate Action Reserve), ACR (American Carbon Registry) - Period: August 2024 - Note: Please be aware that companies are not obligated to register their actual names with registries for Retirement, so accuracy cannot be guaranteed. Also, there may be delays in reflection to registries, so please note that there is a possibility of changes in the number of projects or their status during the current period. ``` Issuance and Retirement figures for the current period are as follows (year-on-year comparison in parentheses). Regarding Issuance volume, the proportion from VCS has become quite small, while Gold Standard (GS) has increased overall, and NbS Issuance from ACR and CAR IFM projects has risen.- Issuance: 16.90 million (-2%), of which Nature-based Solutions 4.03 million (+10%)

- Retirement: 10.22 million (+80%), of which Nature-based Solutions 3.63 million (+84%)

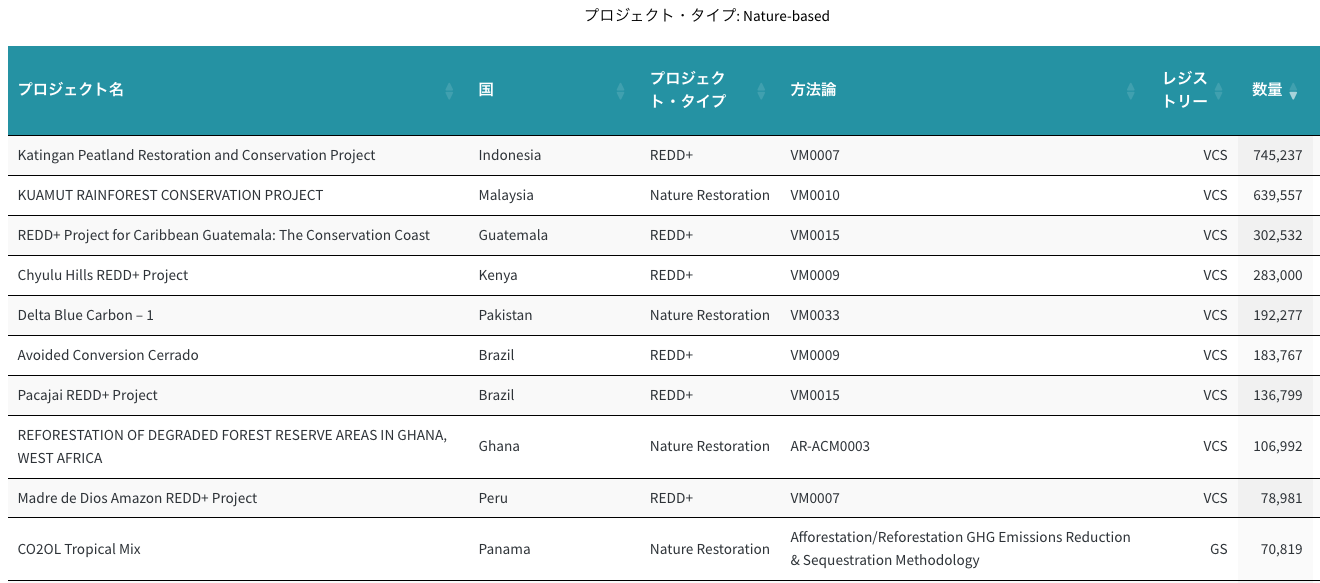

Below are the top 10 projects for which Credits were issued during the current period.

Below is a list of the top 10 Nature-based Solutions projects with the highest Retirement volume during the current period.

In August, two investments in Nature-based Solutions Carbon Credit creation projects were reported. This section focuses solely on investments in natural regeneration and REDD+; other projects such as CCS are not included.

In the second investment, TotalEnergies has committed US$100 million to 20 IFM projects across 10 U.S. states [4]. This is in cooperation with Aurora Sustainable Lands and Anew Climate, the latter of which was already mentioned in the context of Microsoft's transaction in the June newsletter. The projects focus on reducing timber harvesting, improving water quality and soil, and protecting Biodiversity. TotalEnergies plans to retire Carbon Credits after 2030 to voluntarily Offset a portion of its remaining Scope 1 and 2 Emissions, prioritizing Emission Avoidance and Reduction.

<List of Retiring Companies>

Below are the top 10 companies that retired Credits from Nature-based Solutions projects during the period. EY is covered in this newsletter, and Sky River Casino and the Paris 2024 Olympics are also briefly mentioned. PetroChina was already covered in the August newsletter.

- [1] : https://www.reuters.com/sustainability/bhp-rio-tinto-qantas-invest-53-mln-australian-carbon-credit-fund-2024-08-12/

- [2] : https://www.agriinvestor.com/roc-partners-jv-targets-a250-million-for-carbon-credit-fund/

- [3] : https://silvacapital.com.au/faqs/

- [4] : https://totalenergies.com/news/press-releases/united-states-totalenergies-invests-sustainable-forestry-operations-preserve

Company Case Study

**About EY** (For primary sources, please refer to [1] below.)EY (formally Ernst & Young) is a consulting company headquartered in the UK. In 2022, EY announced that it had achieved Carbon Negative status in 2021 and declared its aim to reduce Scope 1, 2, and 3 Emissions by 40% by 2025 compared to 2019, striving for Net Zero. Within this goal, EY has committed to reducing Scope 1 and 2 Emissions by 93% and Scope 3 Emissions by 32% [1].