September 2024 VCM Updates: Section B (1/n)

This article is an automatically translated version of the original Japanese article. Please refer to the Japanese version for the most accurate information.

This is a newsletter from Sustainacraft Inc. This article is Section B (Trends in Major Overseas Regulations) of VCM Updates (Voluntary Carbon Market Updates).

This article covers the following:

- VCMI (Voluntary Carbon Markets Integrity Initiative) Scope 3 Claim Announcement

VCMI has released the Scope 3 Claim, which allows companies struggling with short-term Emission Reductions in Scope 3 to use Carbon Credits to address the gap from their Emission Reduction targets. Public comments on this document will be accepted from September 2nd to October 7th, and the final version, incorporating these comments, is expected to be released in early 2025. The purpose of the Scope 3 Claim is stated to be enabling companies to take meaningful action while they implement the necessary measures to overcome barriers hindering progress in Emission Reductions.

In this article, we will provide the following information regarding the VCMI Scope 3 Claim:

- Background (including a review of VCMI's existing CoP: Claims Code of Practice)

- Contents of the VCMI Scope 3 Claim

- Changes from the Scope 3 Claim draft released last November

- Interpretation (including its relation to SBTi's recent announcement)

This content is also related to the Scope 3 discussion paper recently announced by SBTi (link). We recently hosted a webinar on SBTi's announcement. You can register for the archive distribution here if you are interested. Please note that this webinar assumes a basic understanding of the SBTi framework.

SBTi's recent announcement stated a policy that Emission Reductions and Removal/Sequestration outside the corporate Value Chain, whether through commodity certificates or Carbon Credits, are considered BVCM (Beyond Value Chain Mitigation) and will not be counted towards SBTi's short-term or long-term Scope 3 targets.

In contrast, the content released by VCMI, while reducing the proportion of Carbon Credit use allowed for Scope 3 Emissions compared to last November's draft, is seen by companies as providing guidelines that allow for a time buffer in reducing Scope 3. Furthermore, while Corresponding Adjustment (CA) has not been mandatory in previous VCMI CoPs, the Scope 3 Claim appears to generally require Corresponding Adjustment (CA). This can be considered a reasonable requirement given the nature of the Scope 3 Claim (a temporary Offset-like positioning).

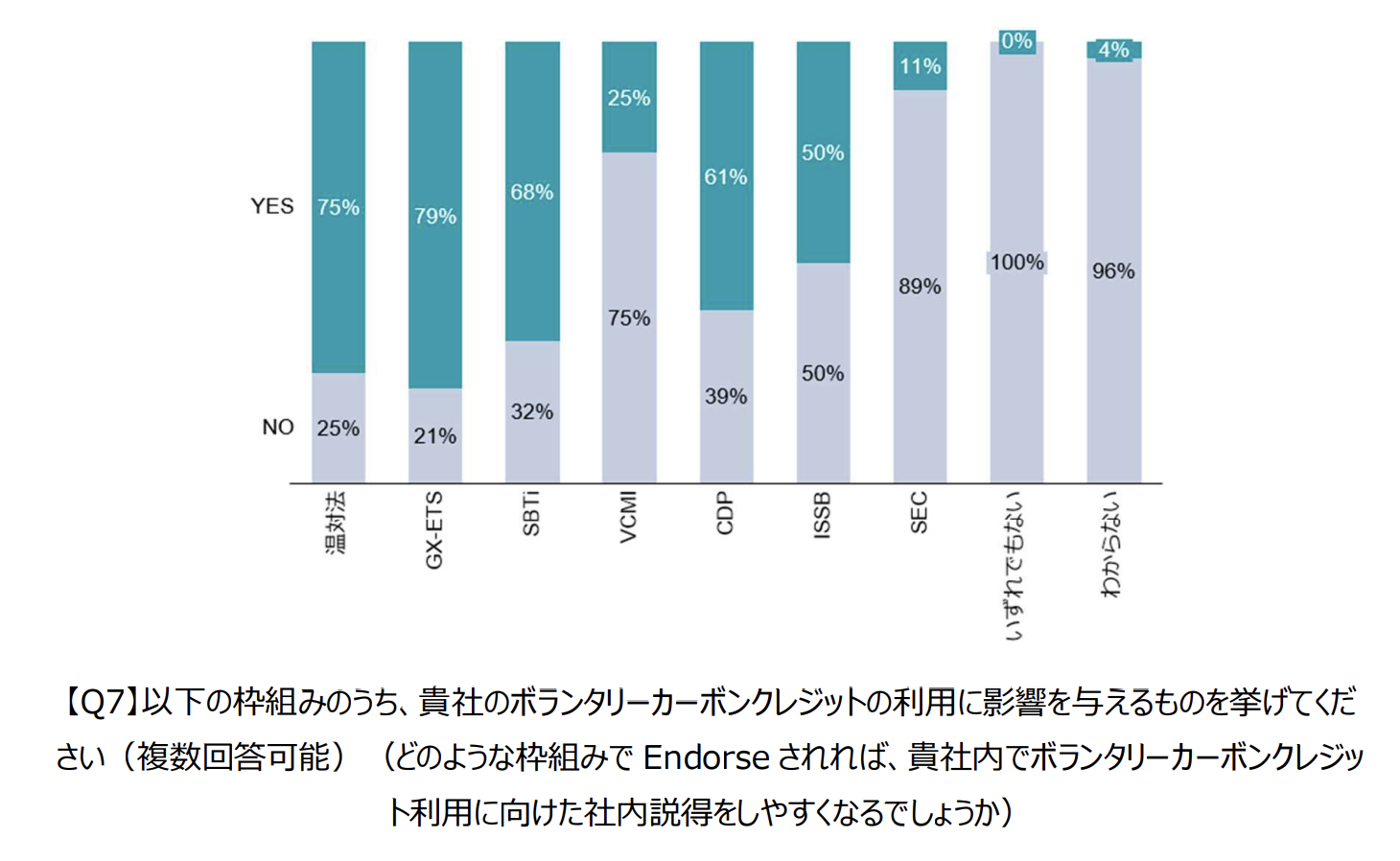

While VCMI currently does not have as much influence as SBTi (*), for companies that feel they "are working on Scope 3 reductions but it takes time," this could serve as a kind of benchmark for external explanations.

(*) For example, please refer to the following survey results (source; from the private sector-led 'Voluntary Credit Disclosure Review WG' report conducted under METI's GX League).

VCMI Scope 3 Claim

(link)

«Positioning of VCMI and CoP»

⚫︎ While IC-VCM's Core Carbon Principles (CCPs) aim to ensure the integrity of the supply side of Carbon Credits, VCMI provides guidelines for the demand side (users).

⚫︎ VCMI's Claims Code of Practice (CoP) offers three types of VCMI claims—Silver, Gold, and Platinum—selectable based on the proportion of Carbon Credits purchased and retired against Emissions, and requires that these Credits are affixed with a CCP label.

⚫︎ This Scope 3 Claim is an evolution of the 'Bronze' claim initially considered in the CoP.

First, let's briefly review VCMI's positioning.

VCMI (Voluntary Carbon Markets Integrity Initiative), as its name suggests, is an initiative concerning the Voluntary Carbon Market. While IC-VCM provides guidelines in the form of Core Carbon Principles (CCPs) to ensure the integrity of the 'supply side' of Credits, VCMI is positioned to provide guidelines for the 'demand side' (users) in the form of its Claims Code of Practice (CoP).

Specifically, the CoP sets basic requirements such as target setting in line with the Paris Agreement's long-term goals and public disclosure of Emissions. Based on this, companies can choose from three types of VCMI claims—Silver, Gold, and Platinum—depending on the proportion of Carbon Credits purchased and retired against their Emissions. This allows companies to externally demonstrate that their decarbonization activities and the use of Carbon Credits within them are recognized by third parties.

Silver, Gold, and Platinum claims under the CoP are not counted as internal to reduction targets but are considered external, i.e., BVCM. They can be viewed as an incentive mechanism for companies to implement BVCM. The initial draft of the CoP also considered a "Bronze" claim, which would have allowed up to 50% of Scope 3 Emissions to be covered by Credits with a deadline of 2030. Although "Bronze" was removed from the final CoP, this Scope 3 Claim is positioned as an evolution of that Bronze claim.

The Credits usable here are those affixed with a CCP label as defined by IC-VCM. However, given the limited availability of CCP-labeled Credits recently, CORSIA-eligible Credits or Credits deemed to meet requirements equivalent to those set by CCPs, with disclosed rationale for that determination, are also expected to be used. These are temporary measures, and for CoP claims made from 2026 onwards, the use of CCP-labeled Credits will be required.

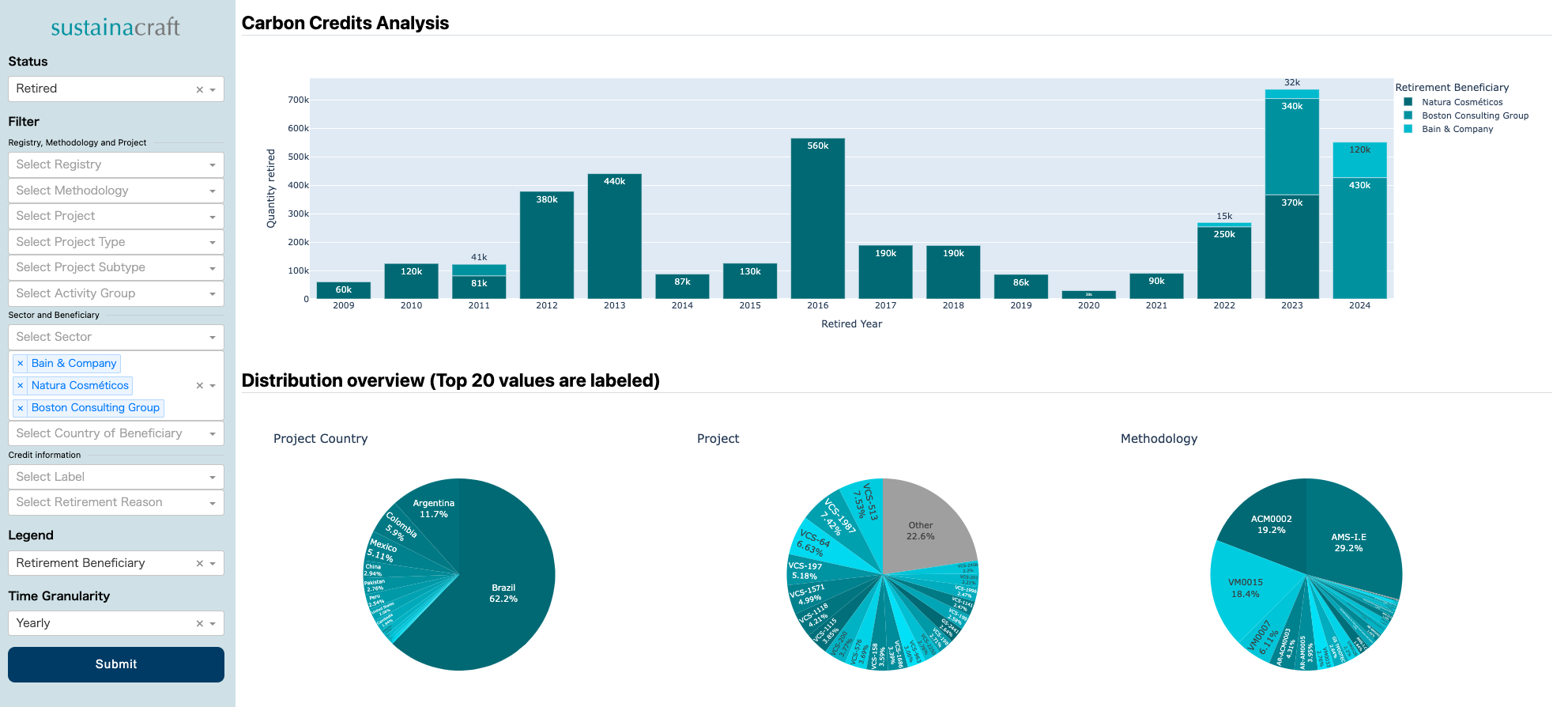

To date, consulting firms Bain & Company and BCG, and Brazilian cosmetics company Natura Cosmetics, have achieved Platinum claims under VCMI.

The Credit Retirement records of these three companies are as follows, with the majority of Credits used being from VCS. Notably, the Retirements by the two consulting firms predominantly involve Nature-based Solutions projects, and a significant portion utilizes Removal/Sequestration Credits from high-priced categories such as ARR.

«Background»