January 2025 VCM Updates: Section B (2024 Review)

This article is an automatically translated version of the original Japanese article. Please refer to the Japanese version for the most accurate information.

This is a newsletter from Sustainacraft Inc. This article is Section B (Trends in major overseas regulations) of VCM Updates (Voluntary Carbon Market Updates).

This article covers the following topic:

- Review of Carbon Credit Transactions in 2024

Please also refer to this month's "Methodology Update", which primarily discusses Methodology revisions, as it provides a qualitative overview of carbon credit market trends in 2024.

Here, we will primarily organize quantitative information related to Carbon Credit transactions.

Introduction

A significant feature of 2024 has been the shift in demand towards "Removal Credits" (or the emergence of new demand segments), with multiple large-scale investments in afforestation projects being announced, unprecedented in scope. Based on our understanding, Offtake Agreements/investment commitments for ARR (Afforestation, Reforestation and Revegetation) projects exceed 50M tCO2, far surpassing the annual Retirement of ARR credits (19M tCO2).

Many companies are likely approaching the procurement of Removal Credits with a mid-to-long-term perspective, in which case it is crucial to assess mid-to-long-term prices and supply potential. Currently, in terms of volume, Removal Credits are almost entirely dominated by ARR projects, and Engineered CDR is predominantly Biochar projects. However, beyond DACCS, BECCS, ARR, and Biochar, there are many Methodologies for creating Removal Credits, with significant differences in "Permanence," "non-carbon Co-benefits such as Biodiversity," "MRV costs," and "land area required." We anticipate that more companies will begin to consider a broader scope of Methodologies and build robust portfolios, especially when thinking about Removal Credit procurement from a mid-to-long-term perspective this year.

Meanwhile, from a climate change mitigation perspective, financing for REDD+ is also crucial in the short term. The past few years have been challenging for REDD+. Towards the end of last year, good news finally began to emerge, with Jurisdictional REDD+ and project-level REDD+ projects from Verra and ART becoming CCP-eligible. As will be explained below, amidst various issues raised concerning REDD+, Verra has been progressing with a multi-year, large-scale Methodology revision, and the new Methodology VM0048 is finally nearing readiness. Regarding the Paris Agreement Article 6.4 mechanism, the "Methodology Standard" agreed upon just before COP29 also includes language anticipating REDD+ in 6.4ERs, raising hopes that REDD+ will be recognized within UN-governed market mechanisms.

Review of Carbon Credit Transactions in 2024

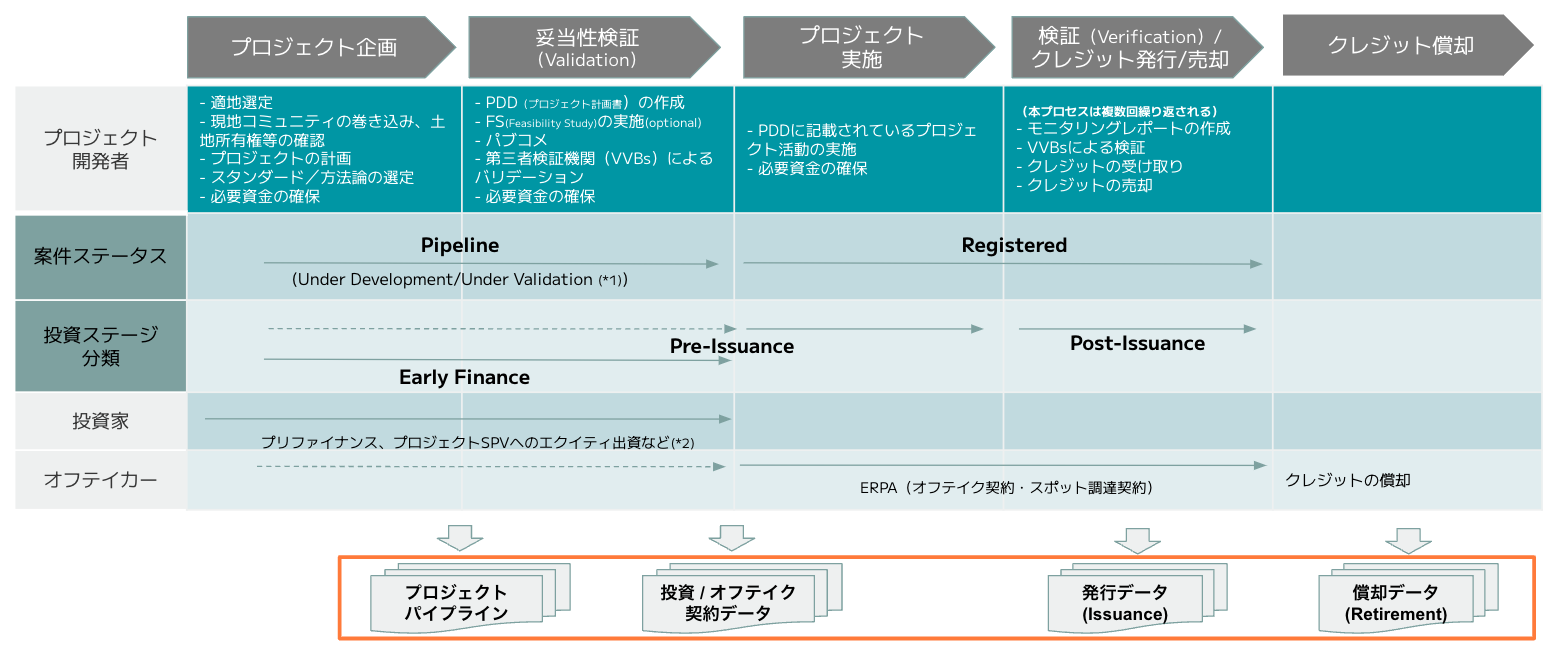

Here, we primarily review the year 2024, organizing quantitative information regarding transactions (Issuance, Retirement, investment/Offtake Agreements, project Pipeline) in the Voluntary Carbon Market.

First, as shown in the figure below, it is important to be aware of the temporal relationships between these data points. Simply put, Retirement reflects the past, Issuance represents the present, and investments, Offtake Agreements, and project Pipelines are useful for forecasting future Credit Issuance.

Please note that companies undertaking Retirement are not required to register their names with the registries, so accuracy cannot be guaranteed. Furthermore, there may be delays in data reflection on registries, so please be aware that transaction volumes, project increases/decreases, and status changes may occur in the future.

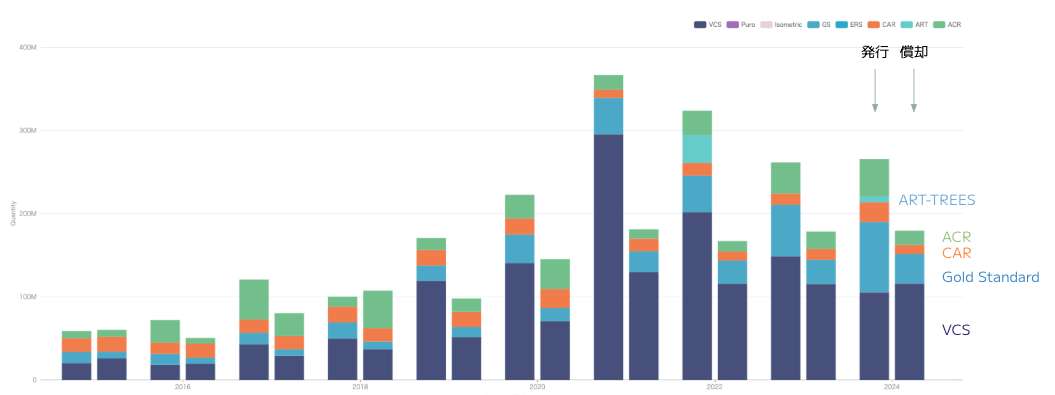

Issuance and Retirement Volumes by Registry

* Period: 2015-2024

* Target Registries: VCS(Verra)、GS(Gold Standard)、CAR(Climate Action Reserve)、ACR(American Carbon Registry)、Puro (Puro.earth), Isometric

For the full year 2024, Retirement volume was 163 M tCO2 (roughly equivalent to 2023 levels), and Issuance volume was 265M tCO2 (based on registry data as of January 7, 2025). Overall, the market continues to see Issuance outpace Retirement.

Looking at the breakdown by registry, Verra's REDD+ Issuance, which previously accounted for the majority of its Issuance, has decreased in recent years as it progresses with large-scale Methodology revisions. Conversely, Issuance from registries other than Verra has increased, resulting in Verra's share based on Issuance volume halving over the past four years (80% (2021) ⇨ 40% (2024)).

Retirement Volumes by Project Type

* Period: 2015-2024

* Target Registries: VCS(Verra)、GS(Gold Standard)、CAR(Climate Action Reserve)、ACR(American Carbon Registry)、Puro (Puro.earth), Isometric

When examining Retirement by project type, energy-related and REDD+ projects still account for the majority of the volume. However, the volume from Nature Restoration projects is steadily rising, reaching approximately 19M tCO2 in 2024.

A key takeaway from the 2024 Retirement review is the emergence of new demand segments seeking "Removal Credits." In contrast to traditional oil & gas and airline companies, firms in the high-tech sector (such as Microsoft), consumer goods and services industries (like Disney and Netflix), professional services (such as EY and Deloitte), and financial institutions (like JP Morgan and Standard Chartered) are actively accelerating their procurement of higher-priced Removal Credits.

This newsletter has frequently covered these use cases. Our monthly "VCM Update Section A" features several case studies of companies retiring Carbon Credits.