October 2025 VCM Updates: Section A

This article is an automatically translated version of the original Japanese article. Please refer to the Japanese version for the most accurate information.

This is a newsletter from sustainacraft Inc. This article is Section A (Market Trends) of VCM Updates (Voluntary Carbon Market Updates).

«VCM Updates Structure»

A. Voluntary Carbon Credit Market Trends ← Subject of this article

- Carbon Credit Issuance, Retirement, and Investment Trend Analysis

- Project Pipeline Analysis

- Detailed Explanation Section

B. Trends in Major International Regulations

Introduction

In this month's newsletter, we cover Carbon Credit Issuance and Retirement data for September 2025.

Carbon Credit Issuance Performance

Total Issuance in September 2025 recorded its highest level in the past three years, with Issuance increasing by over 40% year-on-year. On the other hand, Retirement volumes are on a downward trend.

Particularly noteworthy is the trend of labeled Carbon Credits. Issuance of Article 6 and CORSIA labels was confirmed for a Cookstoves project in Rwanda, indicating that projects in the East African region continue to play an important role in the market. Furthermore, for CCP labels, a Fugitive Emissions project in Uzbekistan continues to have the highest Issuance volume, while for Removal labels, IFM projects on ACR in the U.S. account for the highest total Issuance volume.

Project Pipeline Trends

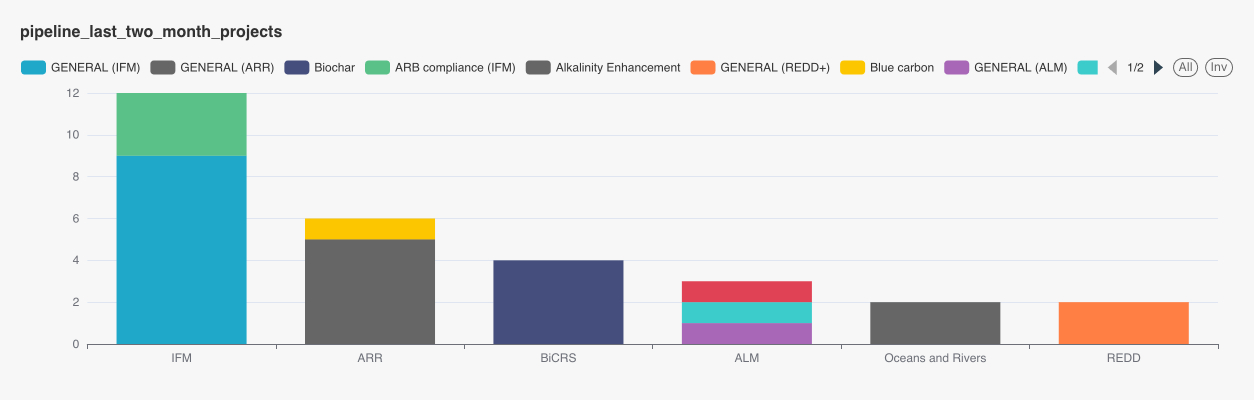

In September, 29 new Nature-based Solutions projects and 3 CDR projects were confirmed as Registered. IFM projects in Mexico and the U.S. are particularly prevalent. Furthermore, ARR projects in Kenya and Sierra Leone, and ALM projects in India, among others, show greater geographical diversity compared to last month's newsletter.

The August Pipeline was updated after last month's newsletter was published, with additional ARR projects including those in Mongolia. While details are provided later, the ARR projects in Mongolia are very large-scale, and the country as a whole is accelerating efforts to explore the potential for Carbon Credit trading under Paris Agreement Article 6, drawing attention as a potential source of JCM Credits.

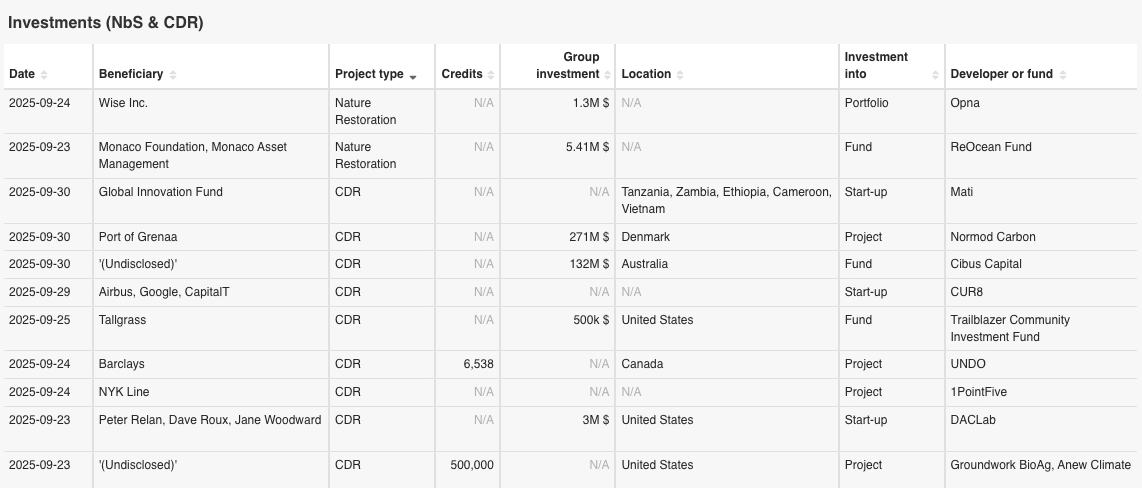

Investment Trends

Eleven investments in Nature-based Solutions and CDR projects were confirmed. Notably, interest in diverse technological fields such as nature restoration, enhanced rock weathering, and DAC is growing through funding and Offtake Agreements. New investments in Nature-based Solutions from entities such as London-based fintech firm Wise and the environmental conservation foundation Monaco Foundation were notable, emphasizing themes like ocean and ecosystem restoration, blue economy, and agroforestry. Among these, Wise shows a shift from traditional Offsets to portfolio-based Removal investments, aiming to establish itself as an early financial intermediary in the Nature-based Solutions and hybrid CDR markets within the fintech sector.

Meanwhile, in the CDR sector, investments and Offtake Agreements in direct Removal technologies (DAC) are progressing from major companies such as U.S. venture capital firm Airbus Ventures, major U.K. bank Barclays, and Nippon Yusen Kaisha (NYK). Notably, this is NYK's second purchase of Carbon Credits from 1PointFive, and DAC Carbon Credits are trading at high prices, averaging over US$500/tCO2. This indicates that the market places significant value on their high Permanence and verifiability.

A. Voluntary Carbon Credit Market Trends

A-1: Carbon Credit Issuance, Retirement, and Investment Trend Analysis

- Target Registries: VCS (Verra), GS (Gold Standard), CAR (Climate Action Reserve), ACR (American Carbon Registry), ART-TREES, Puro (Puro.earth), Isometric

- Target Period: September 2025

- Note: Please be aware that registries are not obligated to register the real names of companies that retire Carbon Credits, and therefore accuracy cannot be guaranteed. Also, there may be delays in reflection on the registries, so please note that the number of projects and their status for this target period may change in the future.

Issuance and Retirement performance for September 2025 is as follows:

Issuance Performance: 32.61 million (YoY +40.37%)

The Issuance volume for the target period was the highest compared to the same period over the past three years, exceeding 300 million.

Looking at data by registry, the proportion of Issuances from VCS, CAR, and GS increased compared to the same period last year, while ACR's proportion decreased. By type, energy (GS and VCS) and nature restoration (VCS, CAR, etc.) increased, while non-CO2 gases decreased.

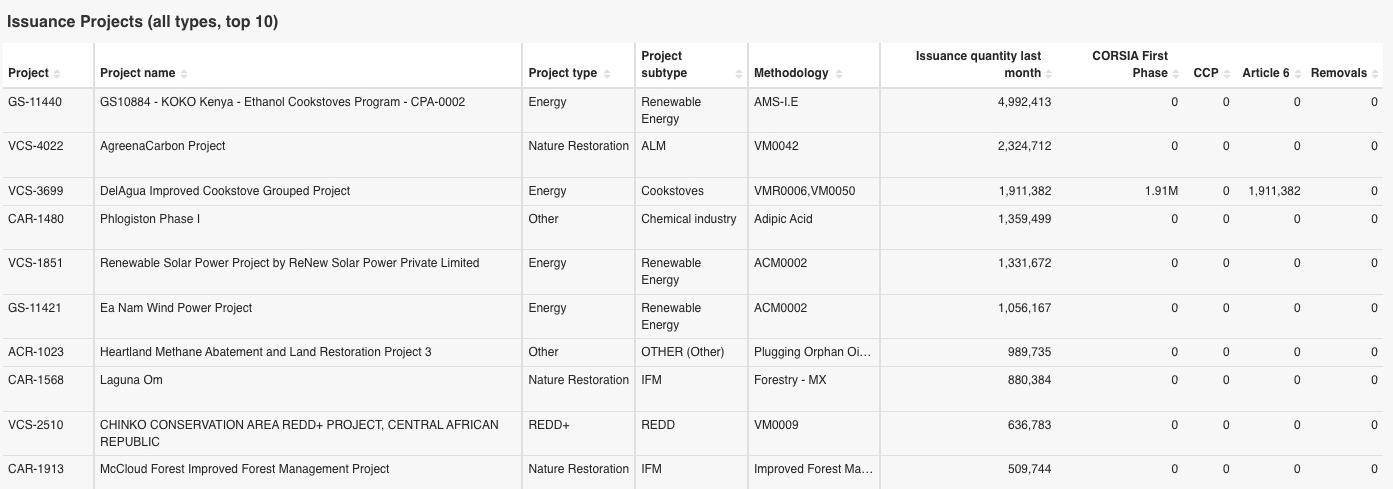

Furthermore, many Carbon Credits were Issued in the "Other" category, totaling approximately 5.8 million tons. Of these, about 1.4 million tons are from the chemical industry (U.S. project, GS-1480), with other categories including safe drinking water supply and construction-related project types.

Retirement Performance: 8.92 million (YoY -8.23%)

Retirements in September slightly decreased year-on-year, falling below 9 million units for the first time in three years.

Looking at the proportions by registry and project type, VCS accounts for the majority, with ACR and CAR increasing. While energy and REDD+ continue to make up half, non-CO2 gases significantly increased.

The Carbon Credit labels displayed below are all based on information provided by each certification body (registry). Therefore, please note the following:

・Even if a Methodology itself is CORSIA eligible or CCP approved, it will not be counted as a labeled Carbon Credit in the table above unless the label information is included in the registry's data.

・Only the VCS and GS registries provide information on Article 6 labels.

Below is a list of the top 10 projects for which Carbon Credits were Issued in September 2025, and a list of projects for which labels (Article 6, CCP, CORSIA, Removal) were Issued.

Top Issued Projects List

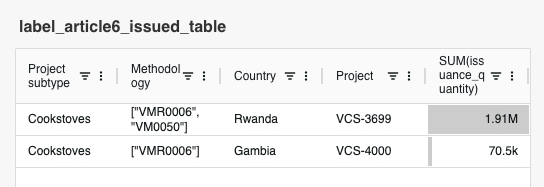

Label Issuance Performance (Article 6)

In September, Article 6 labels were Issued for Cookstoves projects in Rwanda and The Gambia. Looking at past Issuance performance, the same Rwandan Cookstoves project (VCS-3699) accounts for approximately 20% of the total, with Rwandan Cookstoves projects as a whole making up over 80%. The same characteristic applies to CORSIA labels, which will be discussed later: a small number of projects account for a large proportion of the Issuance volume.

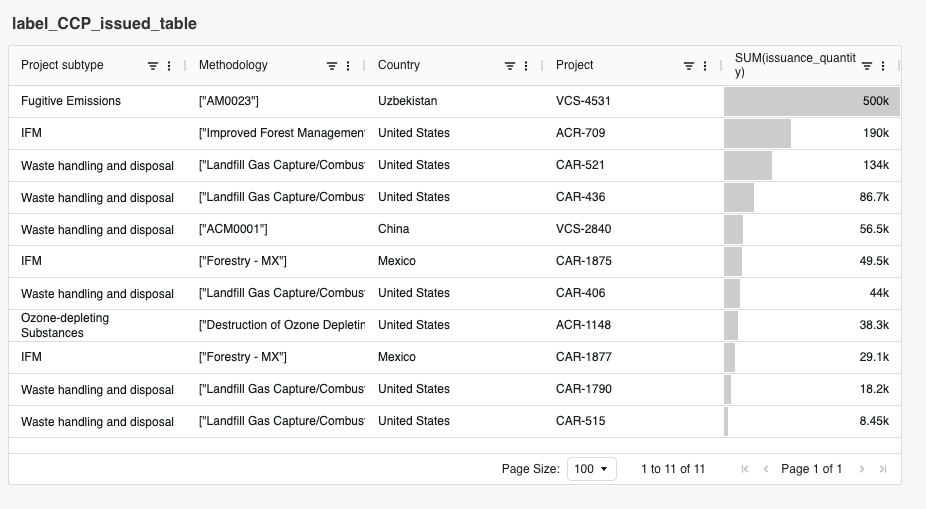

Label Issuance Performance (CCP)

Regarding CCP labels, similar to the previous month, Issuances in September were primarily for Fugitive Emissions projects in Uzbekistan. To date, many Carbon Credits have been Issued for non-CO2 projects, particularly Fugitive Emissions, and among these, the VCS-4531 project has Issued the most CCP-labeled Carbon Credits for three consecutive months.

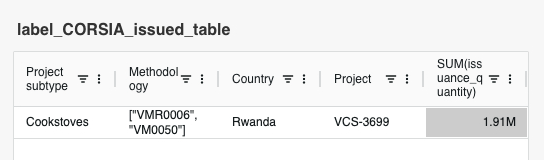

Label Issuance Performance (CORSIA)

In September, CORSIA labels were Issued for the aforementioned Rwandan Cookstoves project that also received Article 6 labels (Phase 1, Vintage 2023 and 2024). Currently Issued CORSIA labels include those from the Pilot Phase and Phase 1. For Phase 1 (2024-2026), a Letter of Authorization (LoA) is required for all Vintages (2021-2026). As an LoA is also required for the Carbon Credits confirmed for Issuance this time, we confirmed that an LoA has already been Issued.

Label Issuance Performance (Removal)

Finally, regarding Removal labels, Issuances occurred in September for five U.S. IFM projects (all on ACR). To date, all U.S. IFM projects with Removal labels have been Registered on ACR, accounting for over half of all Issued Removal Carbon Credits.

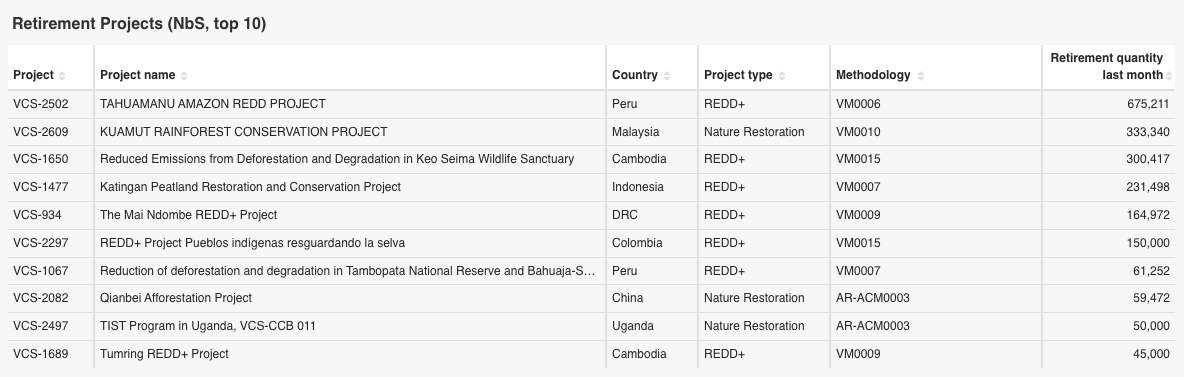

The list of the top 10 Nature-based Solutions projects with the highest Retirement volumes in September 2025 is as follows:

The largest Retirement was observed for a REDD project in Peru (VCS-2502), with over 670,000 units Retired. Carbon Credits from this project were Retired for the first time this year, while the previous Retirement occurred in June 2024, with over 800,000 units being Retired.

The top 10 companies that Retired Carbon Credits from Nature-based Solutions projects in September 2025 are as follows:

The company that Retired the most was PetroChina, with a volume of 230,000 units. To date, the company has cumulatively Retired 4.84 million units from REDD and nature restoration projects. This includes the large-scale Katingan project in Indonesia (VCS-1477).

- Target Projects: We cover investments in Nature-based Solutions and CDR.

- Target Period: September 2025

- Note: For "Credits" and "Group investment," only publicly announced figures are recorded, so there may be blank fields. In this table, "Beneficiary" refers to the investing company or the company purchasing Carbon Credits, and "Investment into" indicates whether the investment target is a project or a fund.

In September, there were 11 significant investments in Nature-based Solutions and CDR projects. For details on these, please refer to Section A-3: Detailed Explanation.

A-2: Project Pipeline Analysis

- Target Registries: VCS (Verra), GS (Gold Standard), CAR (Climate Action Reserve), ACR (American Carbon Registry), ART-TREES, Puro (Puro.earth), Isometric

- Target Projects: Pipeline for Nature-based Solutions and CDR

- Target Period: August-September 2025

- Note: Please be aware that there may be a slight time lag in reflection on the registries, so please note that the number of projects and their status for this target period may change in the future.

- Terminology: Annual ER refers to the annual Emission Reductions or Sequestration (tCO₂e).

This section covers new Pipeline projects for Nature-based Solutions and CDR from last month, as well as updates to the Pipeline from two months ago, which was introduced in the previous newsletter.

Please note that the application dates (Listing Dates) in this database are either directly obtained from registries or estimated. Therefore, please be aware that the comprehensiveness and accuracy of the data are not guaranteed.

The September 2025 Pipeline includes 29 projects, and the August Pipeline, updated after last month's newsletter was published, now includes 17 projects.

Across these two months, IFM projects account for the highest number of projects. Many of these are CAR projects in Mexico and the U.S.