November 2025 VCM Updates: Section A

This article is an automatically translated version of the original Japanese article. Please refer to the Japanese version for the most accurate information.

This is the newsletter from Sustainacraft Inc. This article is Section A (Market Trends) of VCM Updates (Voluntary Carbon Market Updates).

«VCM Updates Structure»

A. Voluntary Carbon Credit Market Trends ← Focus of this article

- Credit Issuance, Retirement, and Investment Trends Analysis

- Project Pipeline Analysis

- Detailed Explanation Section

B. Trends in Major International Regulations

Introduction

This month's newsletter covers Carbon Credit Issuance and Retirement data for October 2025.

Credit Issuance Performance

Both Issuance and Retirement volumes in October 2025 show a decreasing trend compared to the same period last year. Regarding trends in labeled Credits, CORSIA label Issuance has been observed for a cookstove project in Rwanda. Article 6 labels have been Issued for projects in Madagascar and Cambodia, in addition to Rwanda.

Project Pipeline Trends

In October, 10 new nature-based and Carbon Dioxide Removal (CDR) projects were newly Registered. Improved Forest Management (IFM) projects in Mexico and the United States are particularly prominent. Regionally, this includes Reducing Emissions from Deforestation and Forest Degradation (REDD) projects in Gabon and Brazil, and Afforestation, Reforestation and Revegetation (ARR) projects in India, among others. The September Pipeline was updated after last month's newsletter was published, with Agricultural Land Management (ALM) projects in Kazakhstan, etc., being added. From a Joint Crediting Mechanism (JCM) perspective, Kazakhstan and Kenya are particularly noteworthy, and the reasons will be discussed later.

Investment Trends

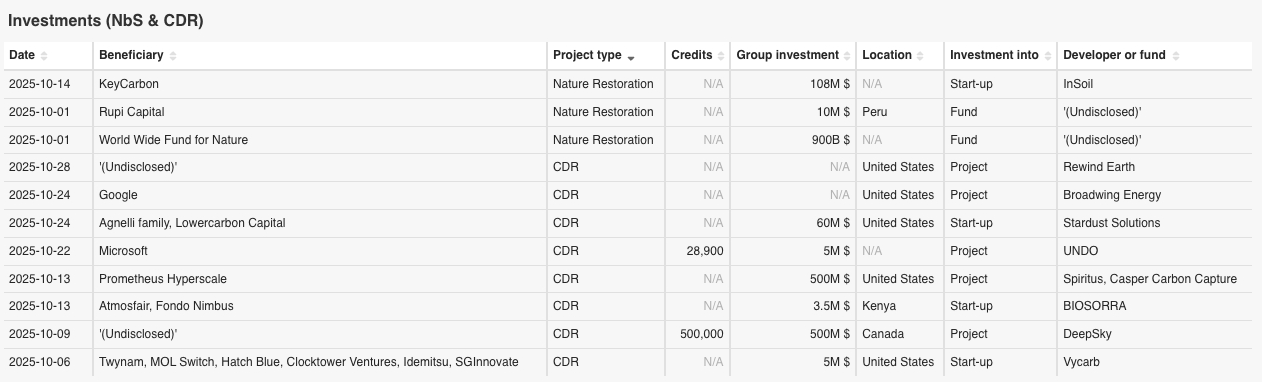

Eleven investments in nature-based and CDR projects were confirmed. For nature-based investments, the expansion of funding for nature-based projects continues, primarily in Latin America and Europe, including a €100 million regenerative agriculture investment by InSoil (a Lithuanian soil tech company) and KeyCarbon (a Canadian Measurement, Reporting and Verification (MRV) solutions provider), and the establishment of a $10 million fund by Peruvian private investment fund Rupi Capital.

Regarding CDR, demand for Carbon Dioxide Removal (CDR) is increasing, exemplified by Microsoft contracting for the largest ever Carbon Dioxide (CO2) Removal purchase for British Carbon Removal company UNDO's Enhanced Rock Weathering (ERW) project. Furthermore, infrastructure investments by both major tech companies and startups are becoming active, such as Canadian CDR Project Developer Deep Sky's $500 million investment in a 500,000-ton capacity facility, and Google's support for US power company Broadwing Energy's Carbon Capture and Storage (CCS) power plant.

In particular, investments in data centers and Removal technologies such as Direct Air Capture (DAC) are becoming active, primarily in North America, along with the increasing demand for AI power.

A. Voluntary Carbon Credit Market Trends

A-1: Credit Issuance, Retirement, and Investment Trends Analysis

- Target Registries: Verra / Verified Carbon Standard (VCS), Gold Standard (GS), Climate Action Reserve (CAR), American Carbon Registry (ACR), Architecture for REDD+ Transactions (ART-TREES), Puro.earth, Isometric

- Target Period: October 2025

- Notes: Please note that companies that have Retired Credits are not required to register their real names with the registries, so accuracy cannot be guaranteed. Also, there may be delays in reflection on the registries, so please be aware that project numbers and status changes may occur for the target period.

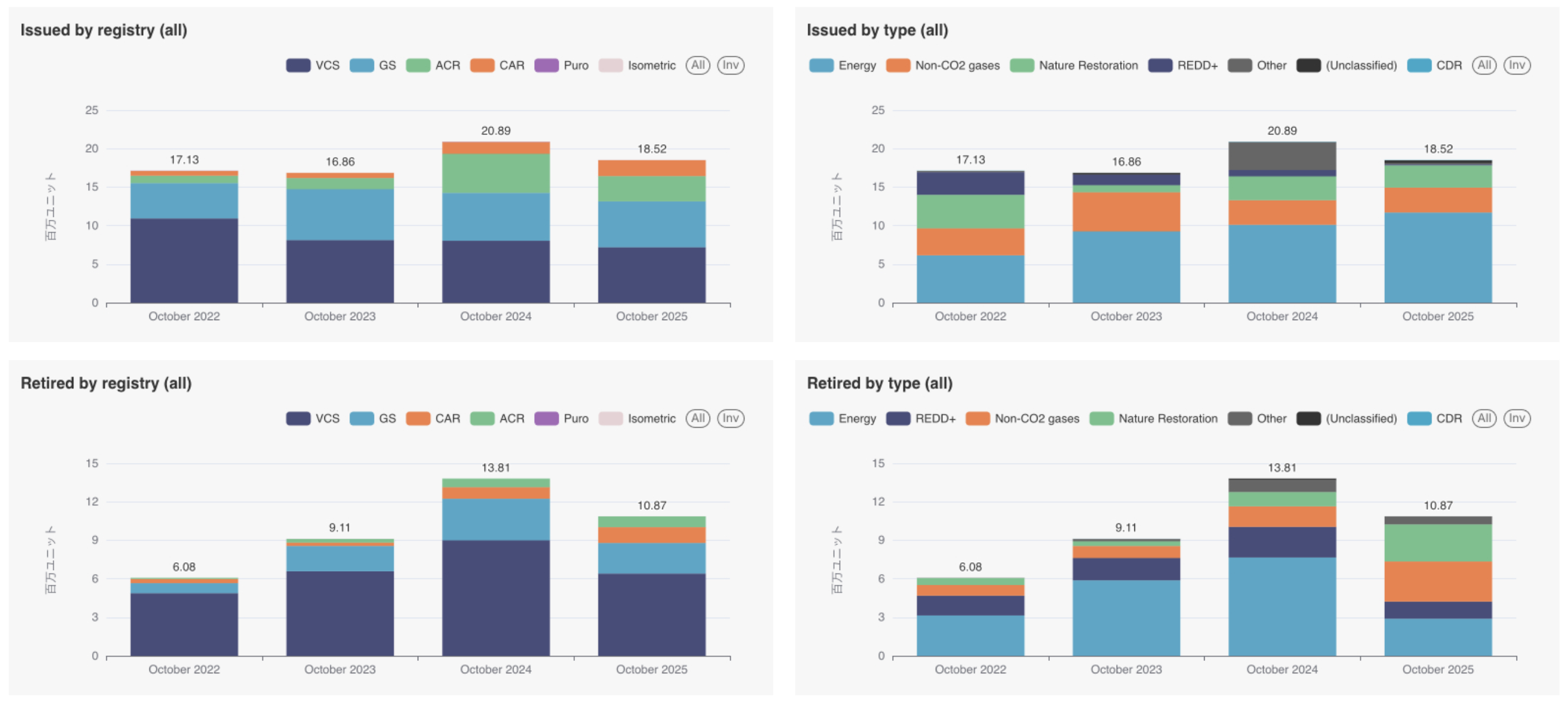

Issuance and Retirement performance for October 2025 is as follows:

- Issuance Performance: 18.52 million (YoY -11.35%)

- The number of Credits Issued during the target period decreased year-on-year, falling below 20 million units.

- Looking at registry-specific data, the proportion of Issuance from VCS and GS accounts for approximately 70% of the total, similar to the previous year. Meanwhile, ACR's Issuance proportion is on a declining trend.

- By type, energy (GS and VCS) is increasing year by year, while non-CO2 gases (CAR and VCS) and nature-based restoration (mainly ACR) had roughly the same Issuance volume as the previous year. In the "Other" category, more Credits were Issued in 2024 than usual, with safe drinking water provision projects accounting for 16.5% of them. In 2025, this type accounted for only 0.74% of the total.

- Retirement Performance: 10.87 million (YoY -21.29%)

- Retirements in October decreased year-on-year, falling below 11 million units.

- Looking at the proportions by registry and project type, VCS again accounts for the majority, but Retirement volume has decreased. While energy-related Retirements decreased to less than 30% of the total, nature-based restoration and non-CO2 gases significantly increased, collectively accounting for approximately 50%.

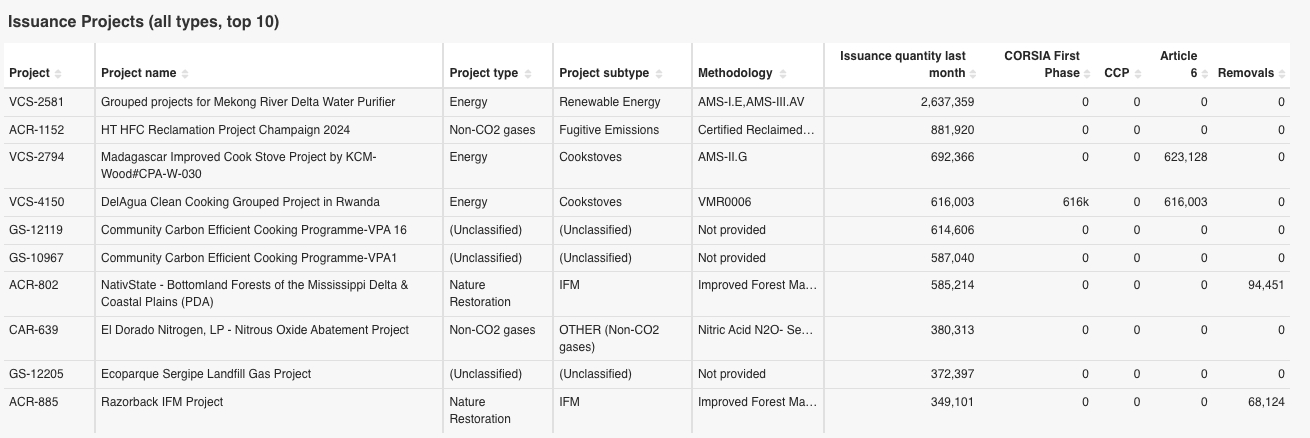

<List of Issued Projects>

The Credit labels displayed below are all based on information provided by each certification body (registry). Therefore, please note the following:

・Even if a Methodology itself is CORSIA eligible or Core Carbon Principles (CCP) approved, Credits will not be counted as labeled in the table above unless the registry's data includes label information.

・Only VCS and GS registries provide Article 6 label information.

Below are the top 10 projects that Issued Credits in October 2025, and a list of projects for which labels (Article 6, CCP, CORSIA, Removal) were Issued.

Top Issued Projects List

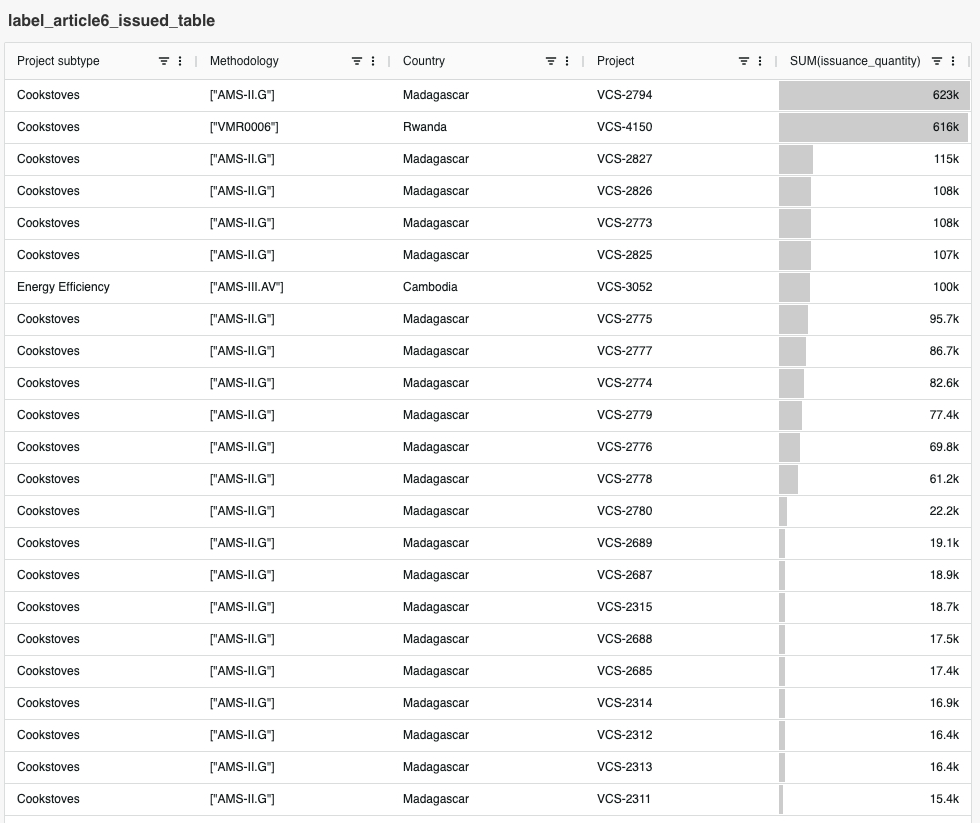

Label Issuance Performance (Article 6)

In October, the number of projects significantly increased compared to the previous month. Article 6 labels have been Issued for cookstove projects in Madagascar and Rwanda, and an energy efficiency project in Cambodia. Looking at cumulative Issuance performance to date, the aforementioned Rwandan cookstove project (VCS-4150) accounts for approximately 50% of the total. Meanwhile, in October, Madagascar's cookstove project Issued the most, with 620,000 units Issued.

Label Issuance Performance (CCP)

Regarding CCP labels, in October, they were Issued only for waste management projects in the United States, China, and Turkey. Cumulatively, Issuance from this project type accounts for approximately 20%. Furthermore, for Uzbekistan's Fugitive Emissions project, which recorded the highest Issuance volume last month, no CCP-labeled Credits were Issued in October for the first time in four months, as of the newsletter's publication.

Label Issuance Performance (CORSIA)

In October, 610,000 CORSIA labels were Issued for the aforementioned Rwandan cookstove project (VCS-4150), which also received Article 6 labels (Phase 1, Vintage 2021-2024). For Phase 1 (2024-2026), a Letter of Authorization (LoA) is required for all Vintages (2021-2026). Since an LoA is required for the Credits confirmed as Issued this time, it was confirmed that the LoA had already been Issued as of 2023.

Label Issuance Performance (Removal)

Finally, regarding Removal labels, in October, they were Issued for five Improved Forest Management (IFM) projects in Canada and the United States (all ACR). This year marks the first time Removal labels have been Issued for a Canadian project, and this instance recorded the largest Issuance volume. To date, all US IFM projects with Removal labels have been ACR projects, accounting for more than half of the Issued Removal Credits.

<List of Retired Projects>

The following is a list of the top 10 nature-based projects with the highest Retirement volume in October 2025.

The largest Retirement was observed for an Afforestation project in Uruguay (VCS-960), with over 720,000 units Retired. This marks the largest Retirement volume for this particular project to date.

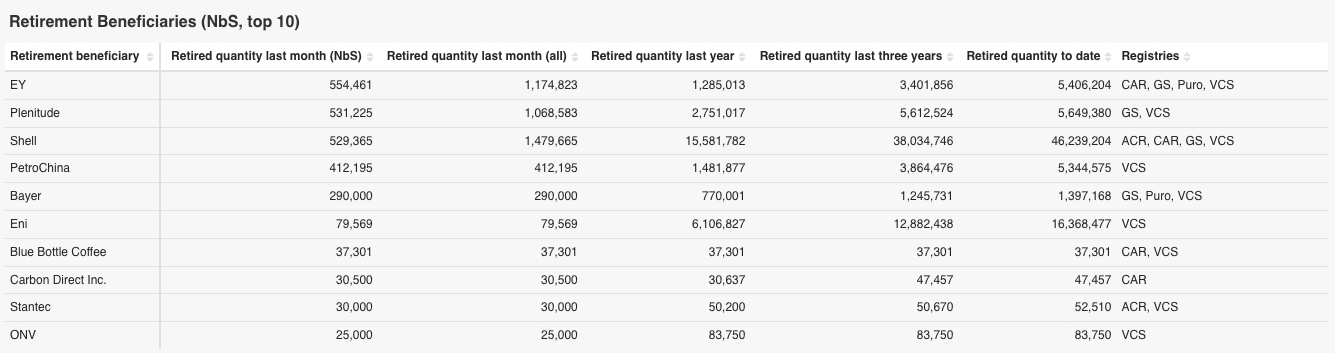

<List of Retiring Companies>

The top 10 companies that Retired nature-based project Credits in October 2025 are as follows:

The company that Retired the most was EY, a professional services firm in the UK, with a quantity of 550,000 units. To date, the company has cumulatively Retired 2.92 million units in REDD and nature-based restoration projects. This includes large-scale projects such as the Katingan project in Indonesia (VCS-1477) and the Guanaré project in Uruguay (VCS-959).

<Investment Trends in Nature-based and CDR Projects>

- Target Projects: Focuses on investments in nature-based and CDR projects.

- Target Period: October 2025

- Notes: For "Credits" and "Group investment," only publicly announced figures are recorded, so there may be blank fields. Also, in this table, "Beneficiary" refers to the investing company or the company purchasing Credits, and "Investment into" indicates whether the investment target is a project or a fund.

In October, there were 11 significant investments in nature-based and CDR projects. For details, please refer to Section A-3: Detailed Explanation.

A-2: Project Pipeline Analysis

- Target Registries: Verra / Verified Carbon Standard (VCS), Gold Standard (GS), Climate Action Reserve (CAR), American Carbon Registry (ACR), Architecture for REDD+ Transactions (ART-TREES), Puro.earth, Isometric

- Target Projects: Nature-based and CDR Pipelines

- Target Period: September-October 2025

- Notes: Please be aware that there may be a slight time lag in reflection on registries, so project numbers and status changes may occur for this target period in the future.

- Terminology: Annual ER refers to annual Emission Reductions / Sequestrations (tCO₂e).

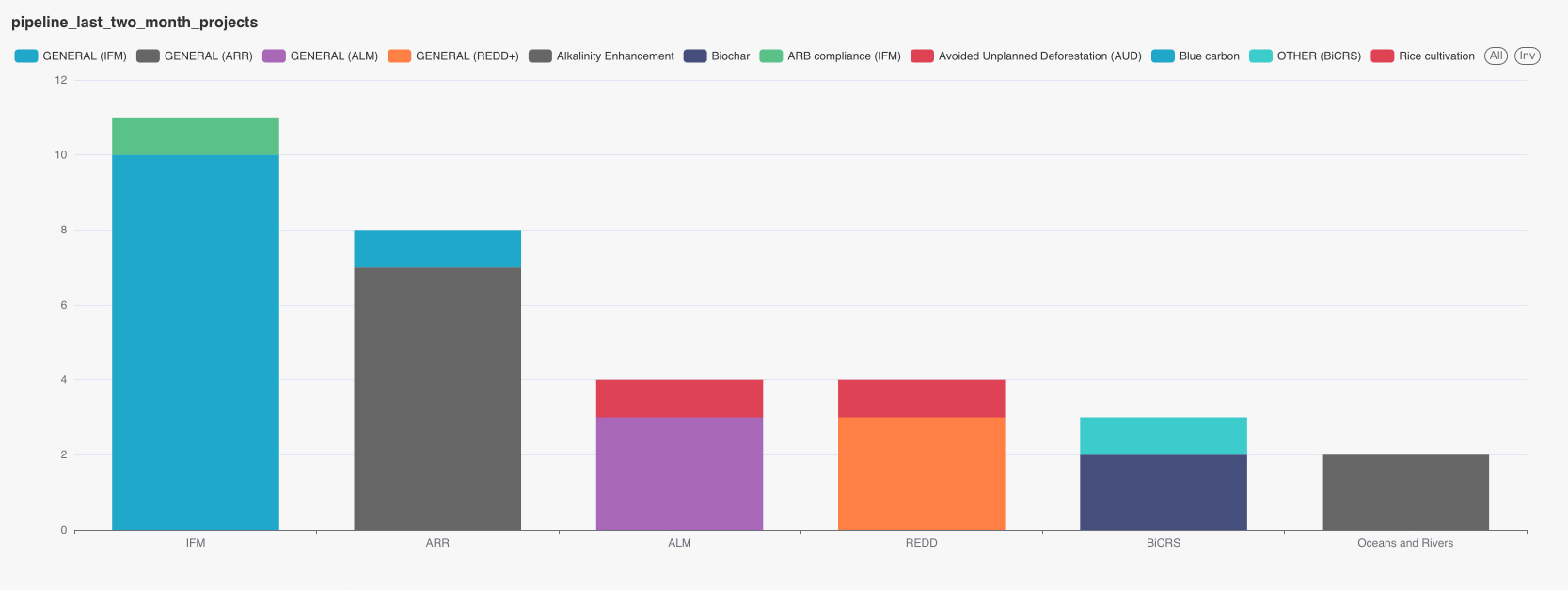

This section covers new nature-based and CDR Pipeline projects from last month, as well as updates to the Pipeline from two months ago, which was introduced in the previous newsletter.

Please note that the application dates (Listing Dates) in our database are either directly obtained from registries or estimated. Therefore, the comprehensiveness and accuracy of the data cannot be guaranteed.

<Nature-based Project Pipeline>

The October 2025 Pipeline includes 11 projects, and the September Pipeline was updated after last month's newsletter was published and now includes 21 projects.

Over these two months, Improved Forest Management (IFM) projects have been the most numerous. Most of these are CAR projects in Mexico (5 projects) and ACR projects in the United States (4 projects), followed by projects in Canada and India.

The October Pipeline includes REDD projects in Gabon and Brazil, and Afforestation, Reforestation and Revegetation (ARR) projects in Mongolia, Argentina, and India, among others. Due to potential time lags in information sharing by registries, an additional 8 projects were added to the September Pipeline since the previous month's newsletter was written. These additions include Agricultural Land Management (ALM) projects in Kazakhstan, IFM projects in Indonesia and the United States, ARR/REDD projects in Malawi, and ARR projects in Madagascar and Kenya.

Kazakhstan's ALM projects account for the largest volume of Emission Reductions (ER) in the September Pipeline. Although Kazakhstan became a Joint Crediting Mechanism (JCM) signatory country in 2023, there are currently no approved or under-discussion Methodologies. However, discussions with Japan have progressed this year. For instance, the first Joint Committee meeting was held in January, and discussions for promoting JCM utilization took place during the Foreign Ministers' meeting in August. Furthermore, a new Project Idea Note (PIN) format was released on November 1, suggesting preparations for future project proposals are underway.

Meanwhile, Kenya is also worth noting.