July 2025 VCM Updates: Section A

This article is an automatically translated version of the original Japanese article. Please refer to the Japanese version for the most accurate information.

Sustainacraft Inc. newsletter. This article is Section A (Market Trends) of VCM Updates (Voluntary Carbon Market Updates).

«VCM Updates Structure»

A. Voluntary Carbon Credit Market Trends ← Subject of this article

- Credit Issuance, Retirement, and Investment Trend Analysis

- Project Pipeline Analysis

- Detailed Explanation Section

B. Trends in Major International Regulations

Introduction

On Credit Issuance, Retirement, Investment Trends, and Project Pipeline Trends

In this month's newsletter, credit issuance and retirement figures cover data from Q2 2025 (April-June).

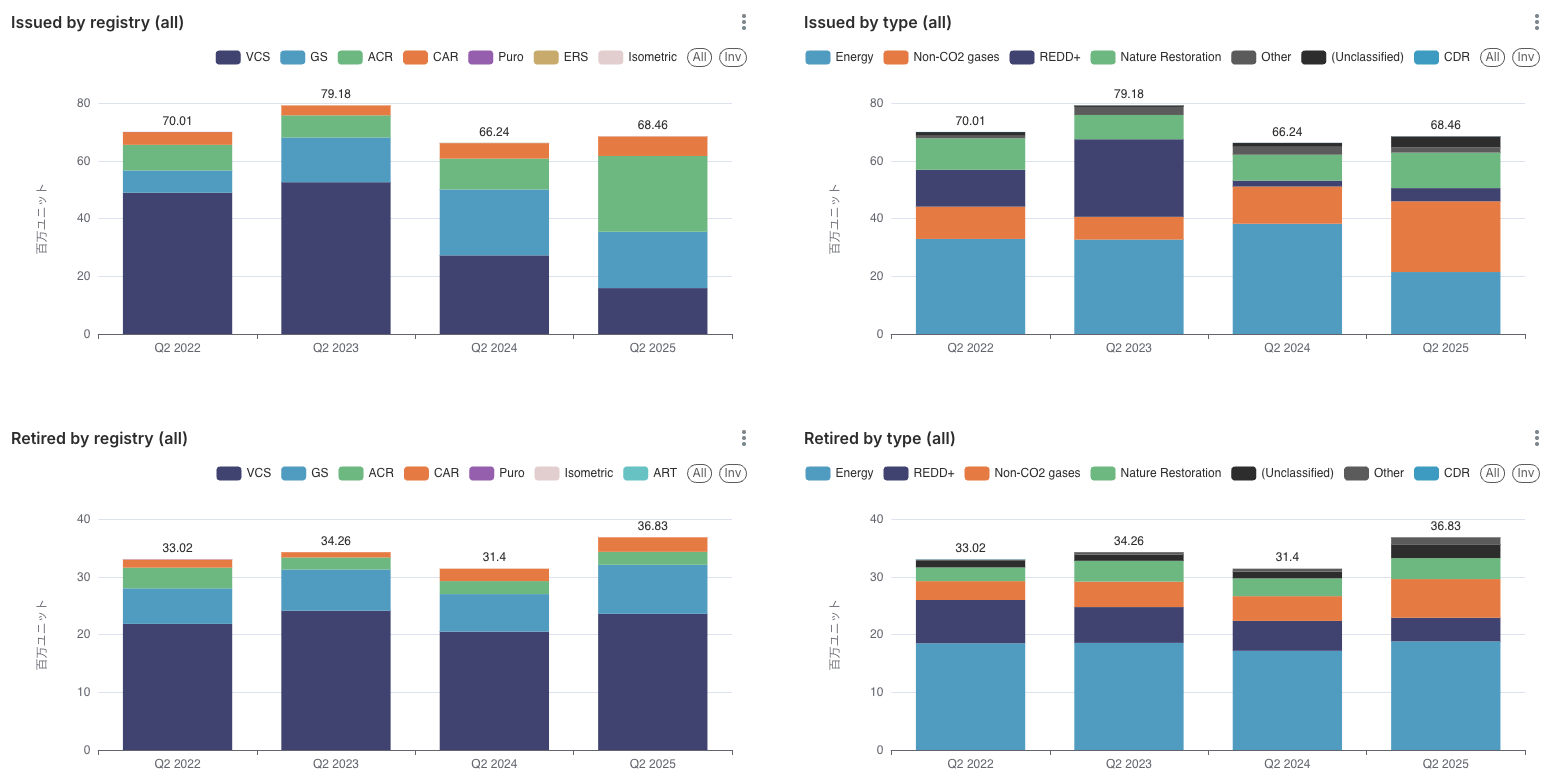

Total issuance in Q2 2025 (April-June) reached 68.46 million units. While this is an increase compared to the previous year, it has not reached the over 70 million units recorded in 2022 and 2023. Looking at the registry breakdown, the proportion of issuances from VCS has decreased since 2024, with ACR accounting for a particularly large share in 2025.

Total retirements in Q2 2025 (April-June) exceeded 36 million units, setting a new record. However, Q1 retirements were lower than the previous year, and Q4 traditionally sees the largest retirements; therefore, it is too early to conclude that the retirement trend is upward without further data analysis. There were no significant changes in the proportions by registry or project type compared to previous periods.

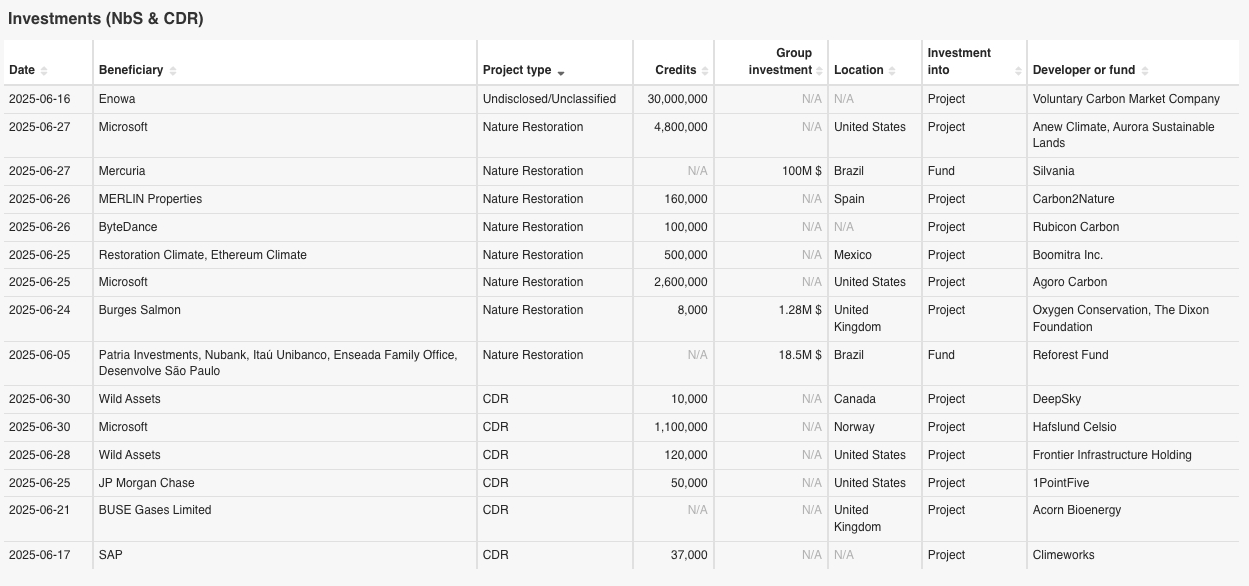

Regarding investment trends, this month we introduce 15 significant investments. Three of these were by Microsoft, involving IFM (4.8 million tons), ALM (2.6 million tons), and BECCS (1.1 million tons). Other notable investments included a large 30-million-ton Offtake Agreement by Enowa, a water and energy sector subsidiary of Saudi Arabia's NEOM, and portfolio-based Credit procurement by SAP and ByteDance through Climeworks and Rubicon Carbon.

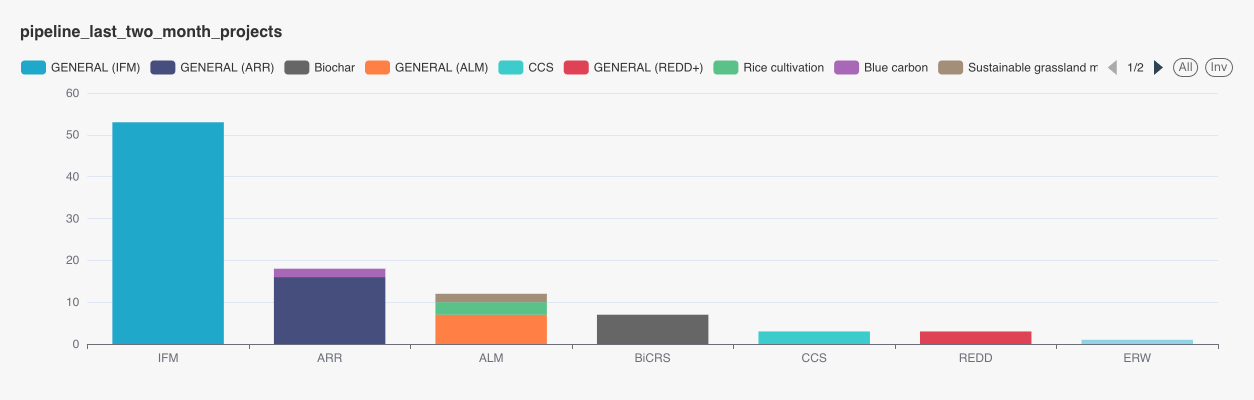

As for new Project Pipelines, June saw the Registration of 24 Nature-based Solutions projects and 1 CDR project. CORSIA-eligible VM0042 (ALM) and VM0033 (Mangrove) projects are emerging from multiple countries. Since some of these are JCM partner countries, we will also discuss project structuring strategies that consider both JCM and CORSIA, and the perspective for evaluating countries in such cases.

A. Voluntary Carbon Credit Market Trends

A-1: Credit Issuance, Retirement, and Investment Trend Analysis

- Target Registries: VCS (Verra), GS (Gold Standard), CAR (Climate Action Reserve), ACR (American Carbon Registry), ART-TREES, Puro (Puro.earth), Isometric

- Target Period: April-June 2025

- Notes: Please be aware that companies that retire Credits are not obligated to register their actual names with the registries, and therefore, accuracy cannot be guaranteed. Also, there may be delays in reflection on the registries, so please note that there is a possibility of changes in the number of projects or their status within the specified period.Issuance and Retirement figures for Q2 2025 (April-June) are as follows:

Issuance Performance: 68.46 million (YoY +3.36%)

Issuances during the period increased compared to the previous year but did not reach the over 70 million units recorded in 2022 and 2023.

Looking at the data by registry, the proportion of issuances from VCS has decreased since 2024, with ACR accounting for a particularly large share in 2025. By type, non-CO2 gas projects have increased (mostly ACR), and Nature-based Solutions (mainly IFM from ACR and CAR) and REDD (all VCS) have slightly increased.

Retirement Performance: 36.83 million (YoY +14.75%)

Retirements in Q2 2025 exceeded 36 million units, setting a new record. However, Q1 retirements were lower than the previous year, and Q4 traditionally sees the largest retirements; therefore, it is too early to conclude that the retirement trend is upward without further data analysis.

Looking at the registry breakdown, VCS and Gold Standard account for the majority. By project type, energy projects are the most numerous, with no significant changes observed in REDD+ or Nature-based Solutions projects compared to the previous year.

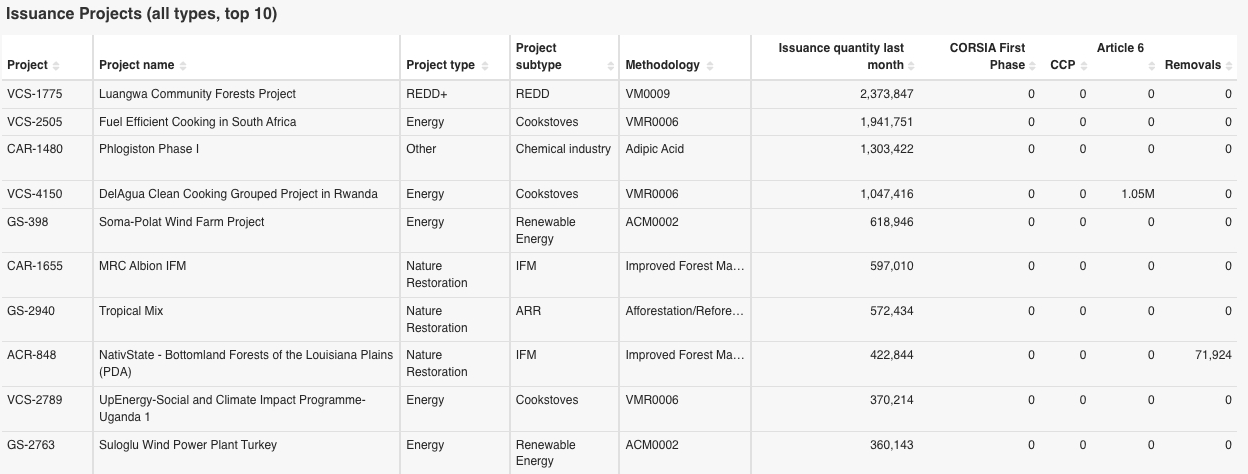

The following is a list of the top 10 projects for which Credits were issued in June 2025.

The labels for Credits shown above (CORSIA, CCP, Article 6, Removals) are all based on information provided by each certification body (registry). Therefore, please note the following:

- Even if a Methodology itself is CORSIA-eligible and CCP-approved, it will not be counted as a labeled Credit in the table above unless the label information is included in the registry's data.

- Only VCS and GS registries provide information for Article 6 labels.

Over 1 million Credits from Rwanda's Cookstoves project (VCS-4150) have been assigned an Article 6 label. Additionally, 70,000 Removals labels have been assigned to a US IFM project (ACR-848).

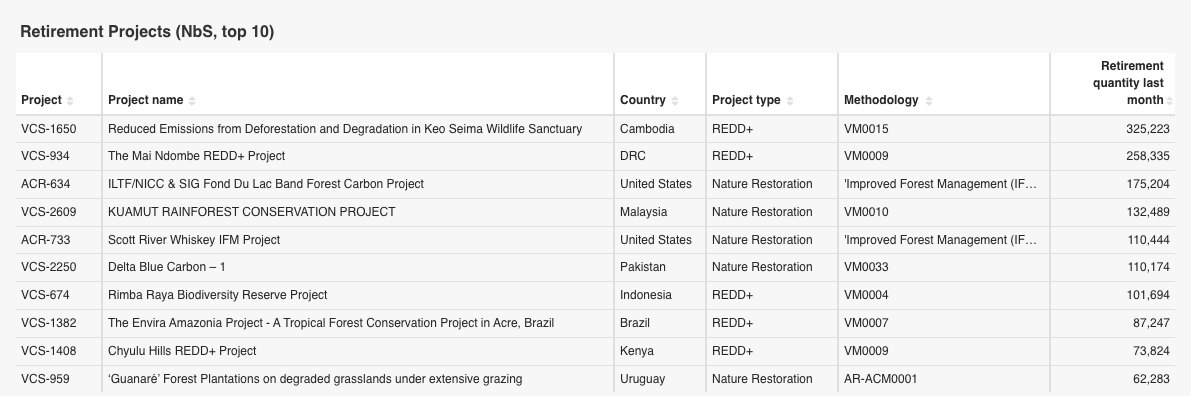

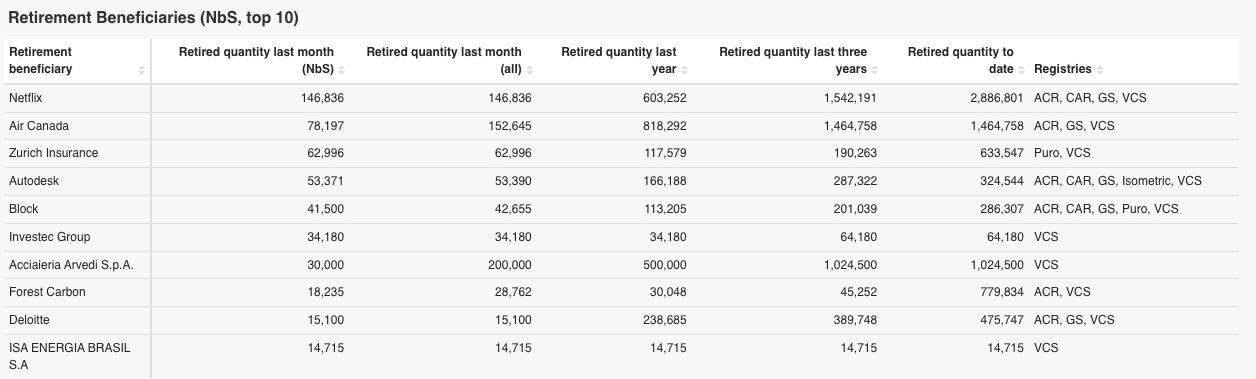

The following is a list of the top 10 Nature-based Solutions projects with the highest number of retirements in June 2025.

The following are the top 10 companies that retired Credits from Nature-based Solutions projects in June 2025.

The company that retired the most Credits was US-based Netflix, with approximately 146,000 units. To date, the company has retired a cumulative 2.76 million units from REDD projects in Kenya and Brazil, an ALM project in Kenya (the Northern Kenya Grassland Carbon Project, which has been the subject of recent criticism), ARR projects in Chile, and Mangrove projects in Pakistan. Netflix has published its carbon Credit project screening criteria in its 2024 ESG Report and 2022 ESG Report, respectively. However, there is no evidence that the criteria have been changed in response to the criticism of the Kenyan project, and as of now, there is no official comment regarding the series of disputes and rulings surrounding the project.

- Target Projects: This section covers investments in Nature-based Solutions and CDR.

- Target Period: June 2025

- Notes: For "Credits" and "Group investment," only publicly announced figures are recorded, so some fields may be blank. In this table, "Beneficiary" refers to the investing company or the company purchasing the Credits, and "Investment into" indicates whether the investment target is a project or a fund.In June, there were 15 significant investments in Nature-based Solutions and CDR projects. For more details on these, please refer to Section A-3: Detailed Explanation Section.

A-2: Project Pipeline Analysis

- Target Registries: VCS (Verra), GS (Gold Standard), CAR (Climate Action Reserve), ACR (American Carbon Registry), ART-TREES, Puro (Puro.earth), Isometric

- Target Projects: Pipeline related to Nature-based Solutions and CDR

- Target Period: May-June 2025

- Notes: Please be aware that there may be a slight time lag in reflection on registries, so there is a possibility of changes in the number of projects or their status for this target period in the future.

- Terminology: Annual ER refers to annual Emission Reductions or Sequestrations (tCO₂e).This section covers new Pipeline projects related to Nature-based Solutions and CDR from last month, as well as updates to the pipeline from two months ago, which were introduced in the previous newsletter.

Please note that the Listing Date in this database is either obtained directly from the registries or estimated. Therefore, we do not guarantee the comprehensiveness or accuracy of the data.

The Pipeline for June 2025 includes 24 projects, and the Pipeline for May, updated after last month's newsletter, now includes 73 projects.