September 2025 VCM Updates: Section A

This article is an automatically translated version of the original Japanese article. Please refer to the Japanese version for the most accurate information.

This is a newsletter from sustainacraft Inc. This article is Section A (Market Trends) of VCM Updates (Voluntary Carbon Market Updates).

«VCM Updates Structure»

A. Voluntary Carbon Credit Market Trends ← This article's focus

- Credit Issuance, Retirement, and Investment Trends Analysis

- Project Pipeline Analysis

- Detailed Analysis Section

B. Trends in Major International Regulations

Introduction

From Credit Issuance Performance

Regarding credit issuance performance, we highlight two points from a JCM perspective: "① the issuance of approximately 800,000 tCO2e Removal-labeled Credits from an IFM project in Malaysia," and "② the issuance of approximately 1 million tCO2e CCP (Core Carbon Principles)-labeled Credits from a Fugitive Emission project in Uzbekistan."

Malaysia is also expected to be a potential JCM partner country. Not only in Malaysia but also in Southeast Asian countries, IFM projects have been increasing in recent years. With relatively lower implementation costs compared to ARR (Afforestation, Reforestation and Revegetation) projects, and the potential to be assigned Removal-type labels depending on the activity content, there is significant potential if these projects can be included as Methodologies within JCM. While being "Removal-type" is not a requirement from a GX/ETS perspective in JCM, some companies prioritize Removal-type activities as a climate change measure. Therefore, IFM in Southeast Asia is considered a potential source of scalable Removal-type Credits.

Fugitive Emission projects are a category that has seen an increase in both project numbers and Credit Issuance over the past few years, and in our classification, we include them in the broader category of "Non-CO2 Emission Reduction." The recent signing of a JCM partnership between Japan and India has been a hot topic in this industry (which will also be covered in Section B of this month's article). Currently, India explicitly restricts activities to be included under Paris Agreement Article 6.2 (similar to the participation requirements for Article 6.4). However, for India's supply potential, a certain volume of non-CO2 Emission Reduction projects, including Fugitive Emission, is expected. As Methodologies, some are emerging with CCP labels, making them a reliable activity type for Offtakers and investors, offering a certain volume for transactions.

From Investment Trends

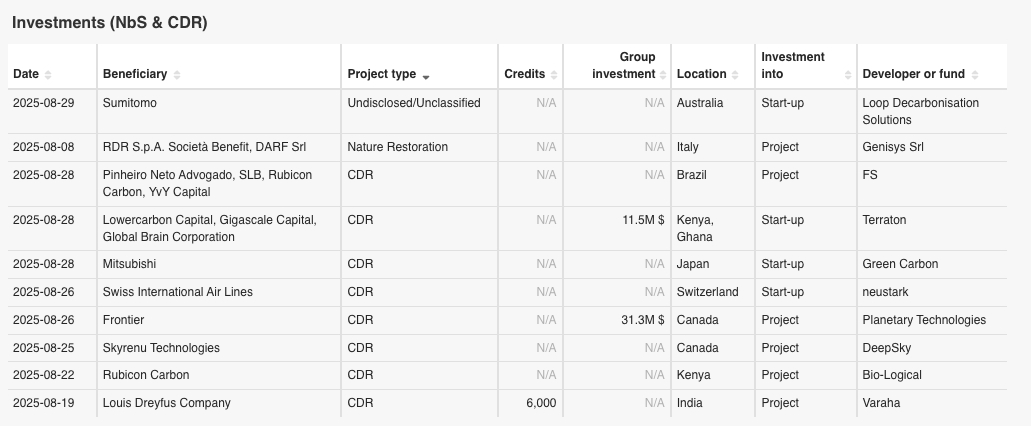

This month, we introduce 10 investment projects, primarily focusing on CDR projects.

Regarding CDR, Biochar projects seem to be becoming mainstream, both as new project Pipelines and investment projects. We believe this is because Durability is emphasized in SBTi's latest Corporate Net Zero Standard, and these projects offer a good balance of Durability and price, as well as being scalable from the perspective of sourcing agricultural and forestry residues. Meanwhile, investments in DAC (Direct Air Capture) businesses and Carbon Credit purchase agreements for Regenerative Agriculture between Louis Dreyfus Company (LDC), one of the world's largest agricultural processors, and Varaha Inc., have also been reported.

In Japan, demand for JCM Credits in anticipation of GX/ETS is rising, but demand for Engineered CDR Credits is not as high. These investment activities are linked to the institutional designs of various countries. Below, we briefly describe the background.

DAC is relatively simple technologically, and deployable technologies are proposed worldwide, yet currently, most operating facilities (with presumably high OPEX) are in North America. This is largely due to the amendment of the tax credit system Section 45Q by the U.S. Inflation Reduction Act (IRA), which increased the tax credit for implementing DAC to US$180 per ton1. Therefore, while there might be room to consider it as an investment opportunity, it is not currently expected that Japanese companies will actively consider investing in DAC for their own use.

On the other hand, LDC's Credit purchase agreement with Varaha Inc. for an ALM project is from an Inset perspective, and could be a benchmark project directly for Japanese companies (especially those with large FLAG emissions). This case is similar to the partnerships mentioned in last month's newsletter, such as Nestlé with re.green and Barry Callebaut with Afforestation/agroforestry Project Developers. It is reported as an Inset activity that contributes to Emission Reduction within the Value Chain, not an Offset. Regarding what constitutes "within the Value Chain," we need to await the final version of the GHG Protocol's "Land Sector and Removals Guidance" (which is expected this year after several delays). However, recent discussions suggest that the definition of "Value Chain" appears to be moving in a relatively broader direction. For more on this topic, we have previously held a webinar explaining it from an SBTi context; please refer to the archive here if interested.

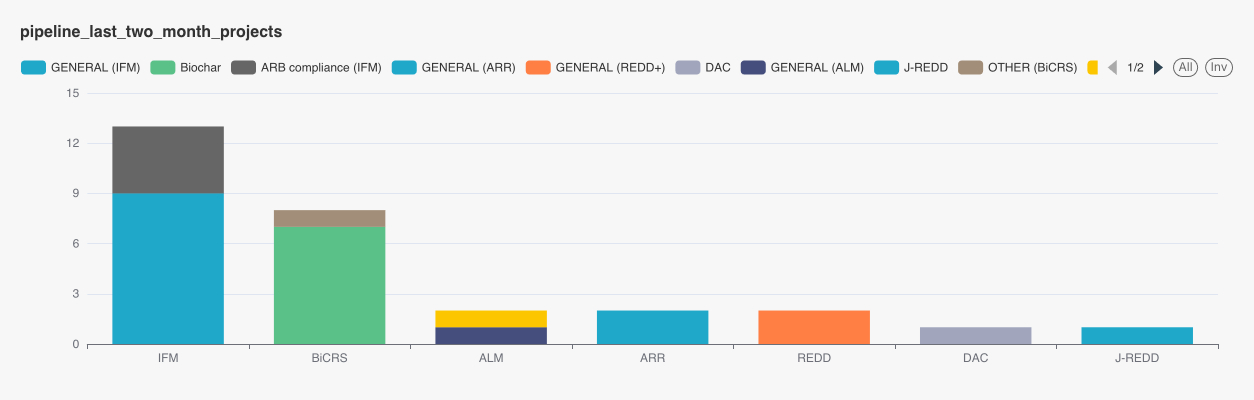

Regarding new project Pipelines, there were 9 Nature-based Solutions projects in August, and the July Pipeline was updated after last month's newsletter publication, now including 20 projects. Additionally, 3 CDR projects were Registered. IFM projects in the U.S. and Mexico (CAR and ACR) have emerged, and this month's Pipeline also saw the addition of REDD+ projects from Colombia and Mexico.

A. Voluntary Carbon Credit Market Trends

A-1: Credit Issuance, Retirement, and Investment Trends Analysis

- Target Registries: VCS (Verra), GS (Gold Standard), CAR (Climate Action Reserve), ACR (American Carbon Registry), ART-TREES, Puro (Puro.earth), Isometric

- Target Period: August 2025

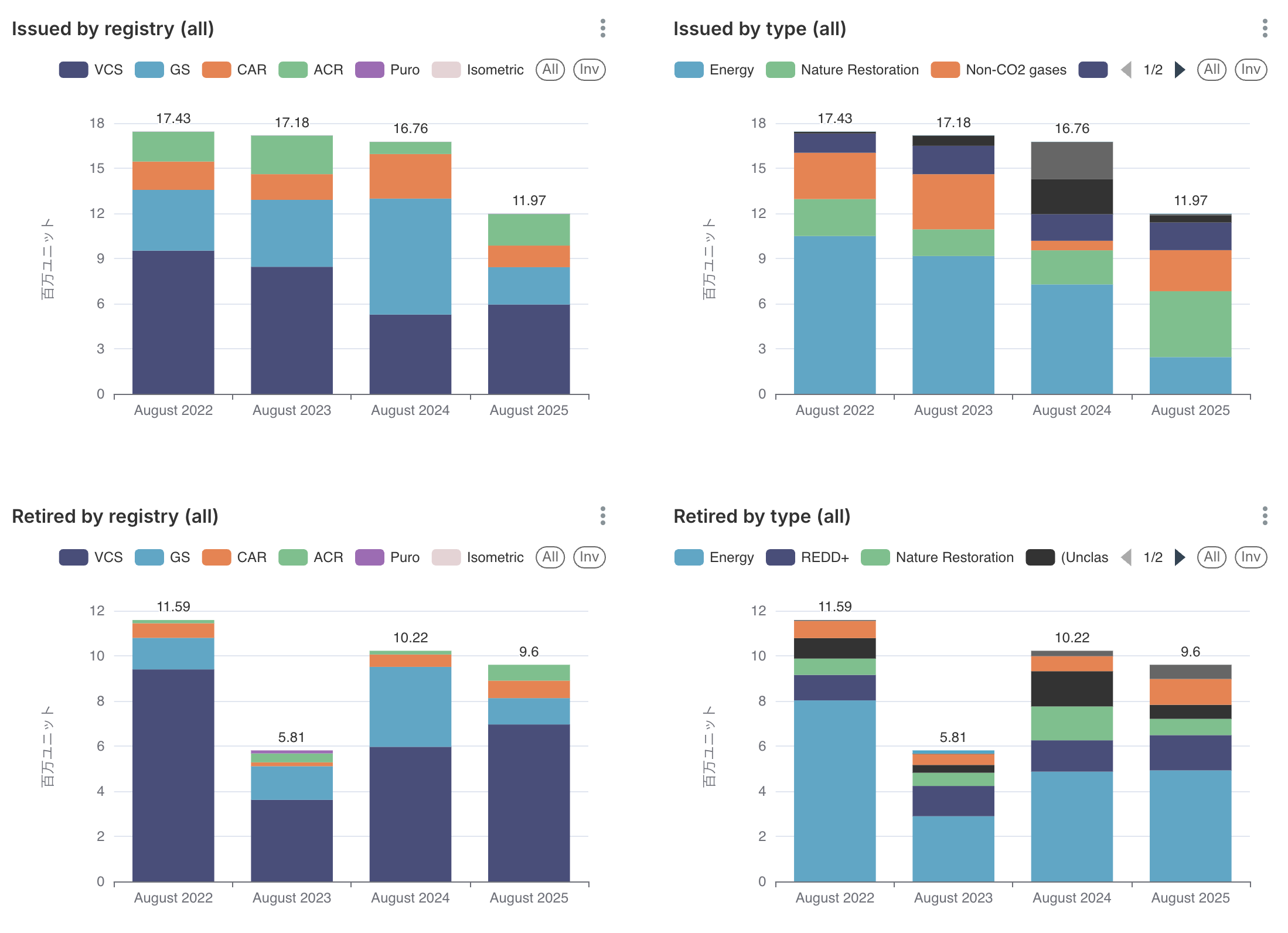

- Notes: Please be aware that companies that have Retired Credits are not required to register their real names with the registries, and therefore, accuracy cannot be guaranteed. Also, there is a delay in reflection to registries, so please note that there may be increases or decreases in projects or changes in their status for the target period going forward.Issuance and Retirement performance for August 2025 is as follows:

Issuance Performance: 11.97 million (YoY -10.27%)

The number of Issuances during the target period significantly decreased compared to the previous year, reaching the lowest volume in the past four years.

Looking at data by registry, the proportion of Issuances from VCS has increased compared to the same period last year. By type, energy (GS and VCS) has decreased, but Nature-based Solutions (primarily IFM from ACR and CAR) and non-CO2 gases have increased.

Retirement Performance: 9.6 million (YoY -17.53%)

Retirements in August decreased year-on-year, falling below 10 million units for the first time in two years.

Looking at the proportions by registry and project type, VCS accounts for the majority, while GS has significantly decreased. The composition where energy and REDD+ account for more than half remains unchanged, but non-CO2 gases have increased, and Nature-based Solutions have decreased.

<List of Issued Projects>

The Credit labels displayed below are all based on information provided by each certification body (registry). Therefore, please note the following:

・Even if a Methodology itself is CORSIA eligible or CCP approved, it will not be counted as a labeled Credit in the table above unless the label information is included in the registry's data.

・Only the VCS and GS registries provide information on Article 6 labels.

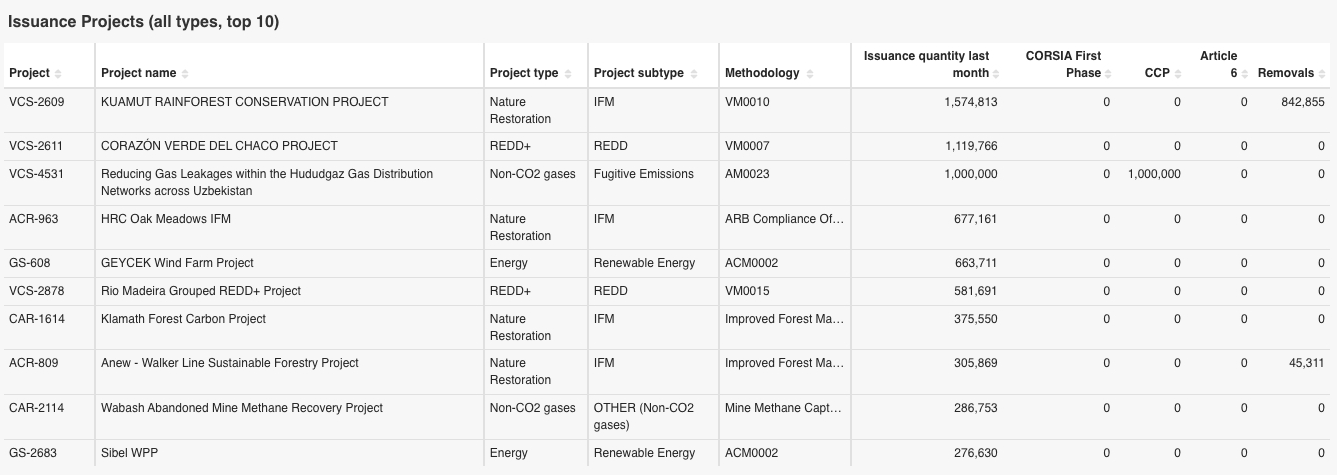

Below are the top 10 projects for which Credits were Issued in August 2025, and a list of projects with labels (Article 6, CCP, CORSIA, Removal) Issued.

Top Issued Projects List

Label Issuance Performance (Article 6)

Last month's newsletter reported that an Article 6 label was Issued for an energy efficiency project in Laos in July, but there were no new Issuances recorded in August.

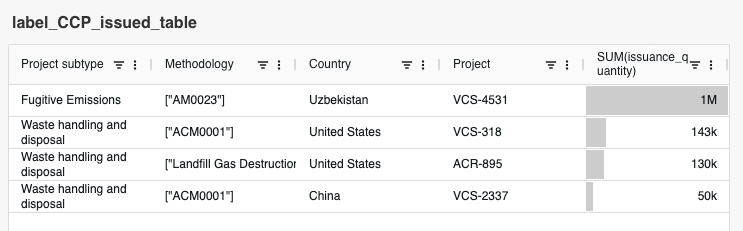

Label Issuance Performance (CCP)

Regarding CCP labels, similar to the previous month, Issuances in August were primarily for Fugitive Emissions projects in Uzbekistan. CCP labels have so far been largely Issued for non-CO2 projects, mainly focusing on Fugitive Emissions.

Label Issuance Performance (CORSIA)

Regarding CORSIA labels, last month's newsletter reported that labels were Issued for an IFM project in Mexico and an energy efficiency project in Brazil in July, but there were no new Issuances recorded in August.

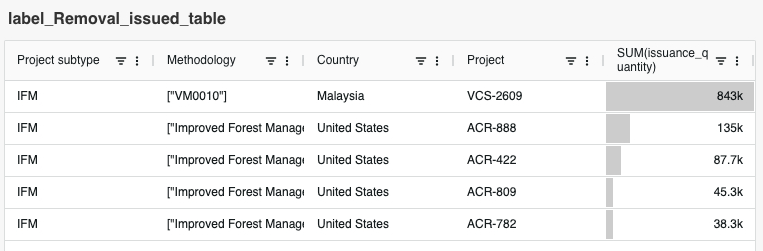

Label Issuance Performance (Removal)

Finally, regarding Removal labels, Issuances occurred in August for four IFM projects in the U.S. (all ACR) and one IFM project in Malaysia (VCS). While Issuances have previously focused on ACR's IFM and ARR projects in the U.S., this time, 843,000 units were Issued by a Malaysian IFM project using VM0010, which is more than double the total Issuance volume of U.S. IFM projects. This project is Malaysia's first Removal-labeled project and the second largest Issuance volume among all Removal-labeled projects to date.

<List of Retired Projects>

The list of the top 10 Nature-based Solutions projects with the most Retirements in August 2025 is as follows:

The largest Retirement was observed for the REDD project in Paraguay (VCS-2611), which also had the largest Issuance volume as mentioned above, with over 800,000 units Retired.

<List of Retiring Companies>

The top 10 companies that Retired Credits from Nature-based Solutions projects in August 2025 are as follows:

The company that Retired the most was Bayer of Germany, with a volume of 300,000 units. To date, the company has cumulatively Retired 1.1 million units for REDD and Nature-based Solutions projects. This includes the REDD project in Paraguay (VCS-2611), which was highlighted in the section above as having the largest Issuance and Retirement volumes.

<Investment Trends in Nature-based Solutions and CDR Projects>

- Target Projects: Investments in Nature-based Solutions and CDR are covered.

- Target Period: August 2025

Notes: For "Credits" and "Group investment," only publicly announced figures are recorded, so there may be blank fields. Also, "Beneficiary" in this table refers to the investing company or the Credit Buyer, and "Investment into" indicates whether the investment target is a project or a fund.

In August, there were 10 significant investments in Nature-based Solutions and CDR projects. For details, please refer to Section A-3: Detailed Analysis Section.

A-2: Project Pipeline Analysis

- Target Registries: VCS (Verra), GS (Gold Standard), CAR (Climate Action Reserve), ACR (American Carbon Registry), ART-TREES, Puro (Puro.earth), Isometric

Target Projects: Nature-based Solutions and CDR Pipelines

Target Period: July-August 2025

Notes: Please note that there is a slight time lag in reflection to registries, so there may be increases or decreases in projects or changes in their status for this target period going forward.

Terminology: Annual ER refers to the annual Emission Reductions and/or Sequestrations (tCO₂e).This section covers new Pipeline projects for Nature-based Solutions and CDR from last month, as well as updates to the Pipeline from the month before last, which were introduced in the previous newsletter.

Please note that the application dates (Listing Dates) in our database are either directly obtained from registries or estimated. Therefore, the completeness and accuracy of the data are not guaranteed.

The August 2025 Pipeline includes 9 projects, and the July Pipeline was updated after last month's newsletter publication, now including 20 projects.

<Nature-based Solutions Project Pipeline>

Over these two months, IFM projects have been the most numerous. Many of these are CAR projects in Mexico and the U.S.