January 2026 Voluntary Carbon Market Updates: Section A

This article is an automatically translated version of the original Japanese article. Please refer to the Japanese version for the most accurate information.

VCM Updates Section A: Voluntary Carbon Credit Market Trends

This newsletter is brought to you by Sustainacraft Inc. This article is Section A (Market Trends) of VCM Updates (Voluntary Carbon Market Updates).

«VCM Updates Structure»

A. Voluntary Carbon Credit Market Trends ← Covered in this article

- Credit Issuance, Retirement, and Investment Trends Analysis

- Project Pipeline Analysis

- Detailed Commentary Section

B. Trends in Major Overseas Regulations

Introduction

In this month's newsletter, we cover Carbon Credit Issuance and Retirement data for December 2025.

Carbon Credit Issuance Performance

While December 2025 Issuance volumes remained consistent with the previous year, Retirement volumes showed a declining trend year-on-year. Regarding trends in labeled Credits, Carbon Offsetting and Reduction Scheme for International Aviation (CORSIA) labels were confirmed issued for Cookstoves projects in Laos and Gambia. Article 6 labels were confirmed issued for Cookstoves projects in Laos and Gambia, as well as for a renewable energy project in Togo. Removal labels were only issued for Improved Forest Management (IFM) projects in the US, while Core Carbon Principles (CCP) labels were issued for the same US IFM projects, in addition to waste management projects in Brazil and China, and renewable energy projects in Turkey, among others.

Project Pipeline Trends

In December, 57 new nature-based projects were registered in the Pipeline, while there were no Carbon Dioxide Removal (CDR) projects. These included Afforestation, Reforestation and Revegetation (ARR) projects in Senegal and Indonesia, and Reducing Emissions from Deforestation and Forest Degradation (REDD) projects in Brazil. The November Pipeline was updated after last month's newsletter was published, with 10 additional projects, including a REDD project in Paraguay. From a Carbon market perspective, Brazil, Zambia, and Rwanda are particularly noteworthy, and the reasons will be discussed later.

Investment Trends

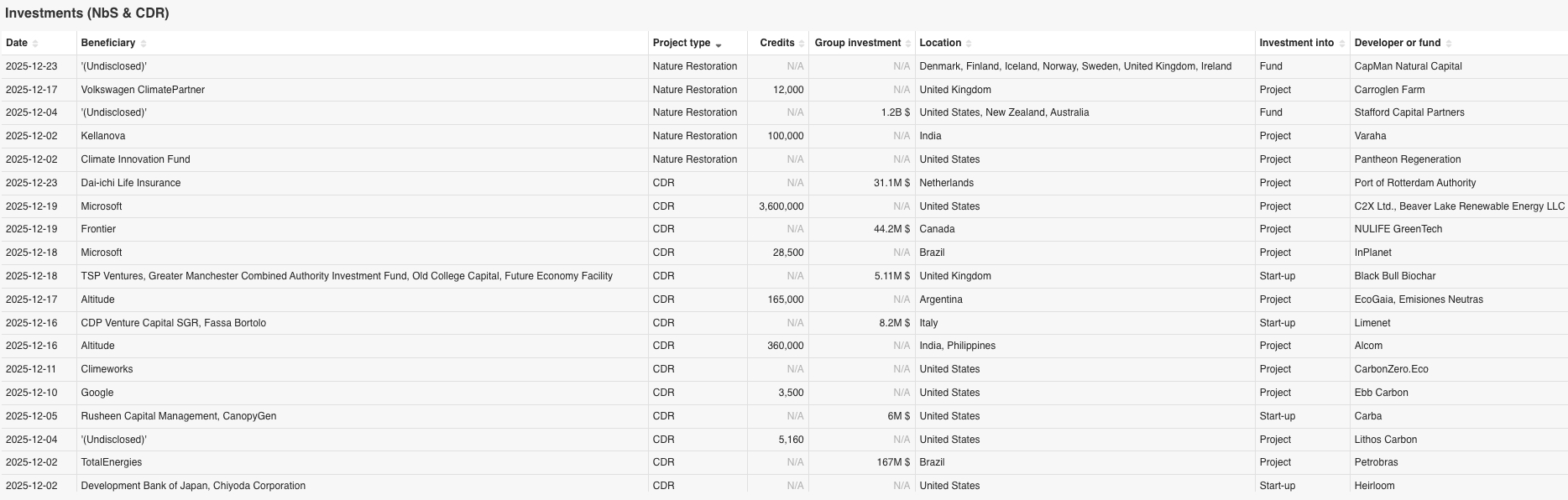

Nineteen investments in nature restoration and Carbon Dioxide Removal (CDR) projects were confirmed, showing strategic capital inflows from diverse entities such as asset management firms, tech giants, institutional investors, and energy companies. In the nature restoration sector, there was the establishment of a new $1.2 billion forest fund by British investment firm Stafford Capital, and the closing of a forest investment fund by Nordic forest investment fund manager CapMan Dasos. Furthermore, Volkswagen and Microsoft supported Peatland restoration, and major US food industry player Kellanova engaged in regenerative agriculture initiatives to support smallholder farmers in India.

Meanwhile, in the CDR sector, Offtake Agreements by major Buyers are driving technological innovation, such as the $44.2 million contract with NULIFE, a Canadian waste management and Carbon removal technology company, via Frontier, and a 12-year long-term Removal contract between Microsoft and British green methanol developer C2X. Investment targets have diversified and portfolio development has progressed, including Biochar (Altitude, Carba), enhanced rock weathering (Lithos Carbon, InPlanet), ocean CDR (Ebb Carbon, Limenet), and direct air capture technology (Heirloom). Furthermore, Dai-ichi Life's investment in CCS-specific corporate bonds and TotalEnergies' $167 million investment in Brazilian CCS exploration symbolize strong capital injection from financial and energy companies towards the social implementation of Emission Reduction infrastructure.

A. Voluntary Carbon Credit Market Trends

A-1: Carbon Credit Issuance, Retirement, and Investment Trends Analysis

- Target Registries: Verra / Verified Carbon Standard (VCS), Gold Standard (GS), Climate Action Reserve (CAR), American Carbon Registry (ACR), Architecture for REDD+ Transactions (ART-TREES), Puro.earth, Isometric

- Target Period: December 2025

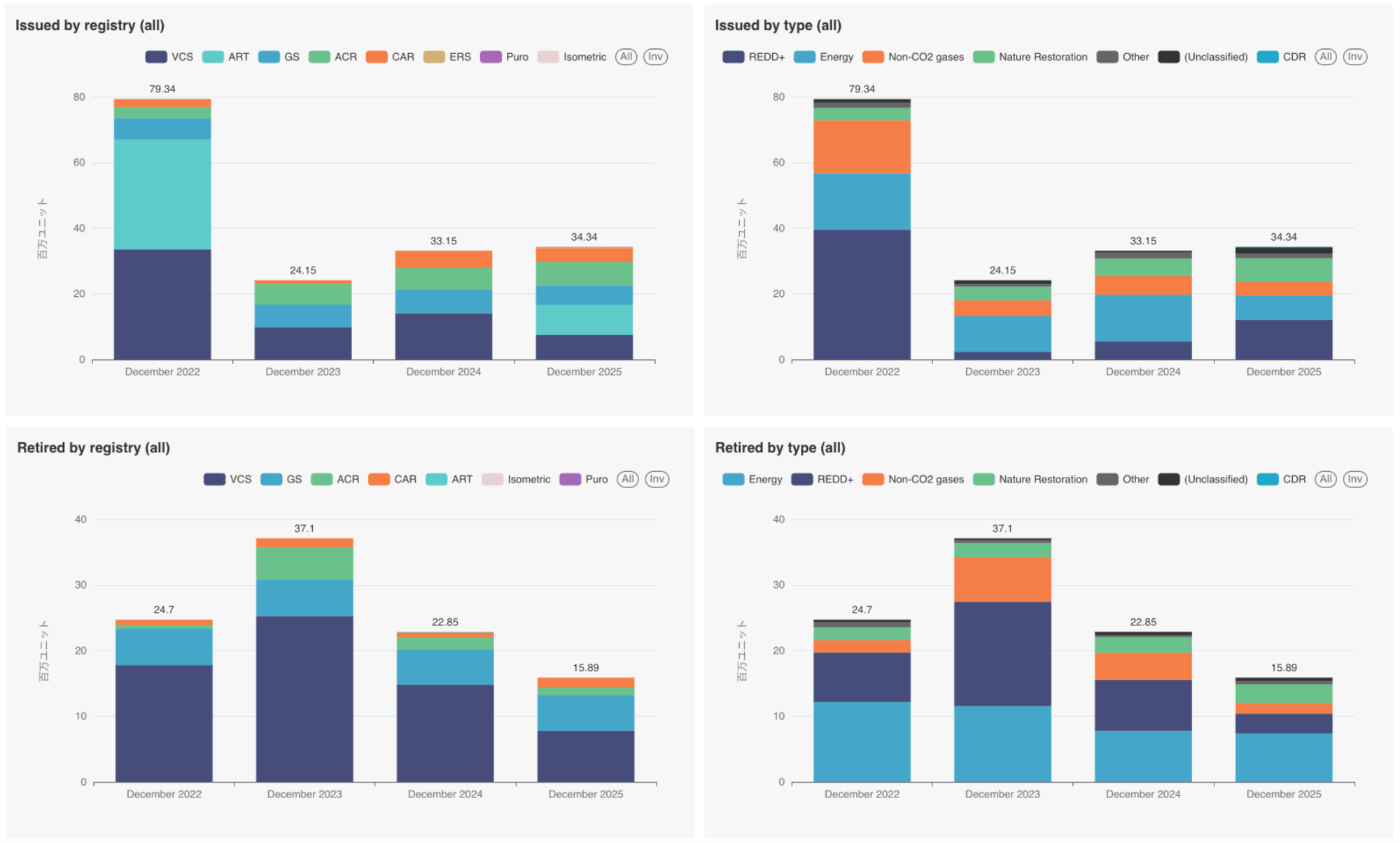

- Notes: Please be aware that companies that retire Credits are not obligated to register their real names with the registries, and therefore, accuracy cannot be guaranteed. Additionally, there may be delays in reflecting data in the registries, so please note that the number of projects or their status may change for the current reporting period.The Issuance and Retirement performance for December 2025 is as follows:

- Issuance Performance: 34.34 million (approximately same as previous year)

- The number of Credit Issuances for the target period remained approximately the same as the previous year, again falling below 30 million units.

- Looking at data by registry, Architecture for REDD+ Transactions (ART-TREES) significantly increased, accounting for over a quarter of the total. This was the highest proportion. Meanwhile, Verra / Verified Carbon Standard (VCS) decreased considerably, accounting for approximately 20% of the total this time.

- By type, Reducing Emissions from Deforestation and Forest Degradation (REDD) projects significantly increased due to the impact of ART-TREES, accounting for over 30% of the total. On the other hand, energy (mainly Gold Standard (GS) and Verra / Verified Carbon Standard (VCS)) and non-CO2 gases (such as American Carbon Registry (ACR) and Climate Action Reserve (CAR)) decreased.

- Retirement Performance: 15.89 million (43.8% decrease year-on-year)

- Retirements in December significantly decreased year-on-year, reaching their lowest level within the target period, falling below 20 million units.

- Looking at the proportion by registry and project type, Verra / Verified Carbon Standard (VCS) accounted for the majority of the total, but Retirement volumes continued to decline. While energy-related Retirement volumes remained approximately the same as the previous year, REDD significantly decreased, accounting for approximately 20% of the total.

<List of Issued Projects>

All Credit labels displayed below are based on information provided by each certification body (registry). Therefore, please note the following:

・Even if a Methodology itself is CORSIA eligible or CCP approved, Credits will not be counted as labeled in the table below unless label information is included in the registry's data.

・Only Verra / Verified Carbon Standard (VCS) and Gold Standard (GS) registries provide information on Article 6 labels.

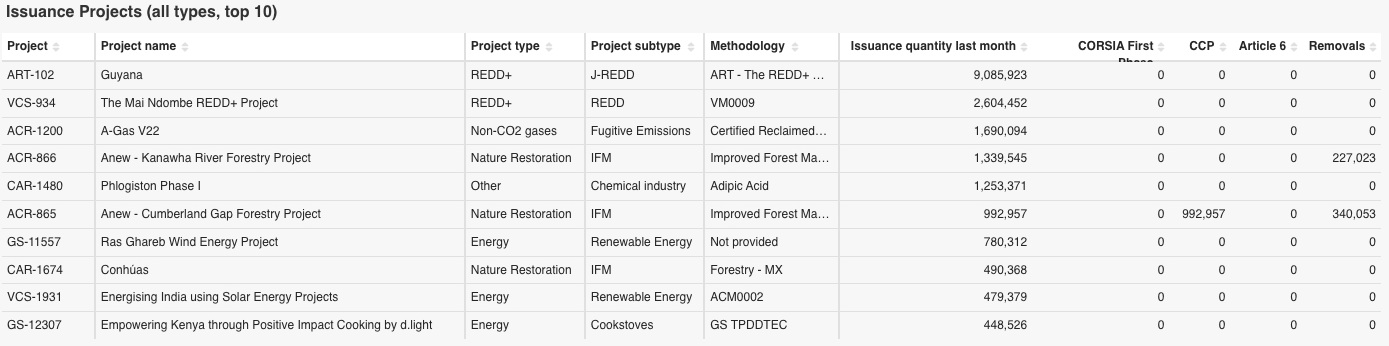

Below is a list of the top 10 projects for which Carbon Credits were issued in December 2025, and a list of projects for which labels (Article 6, Core Carbon Principles (CCP), Carbon Offsetting and Reduction Scheme for International Aviation (CORSIA), Removal) were issued.

Top Issued Projects List

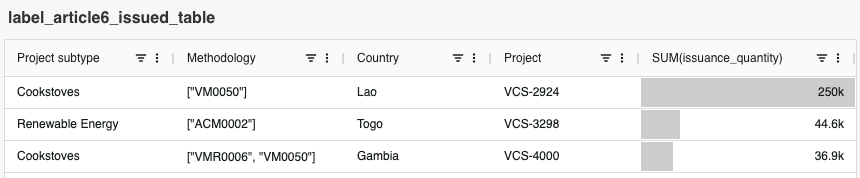

Label Issuance Performance (Article 6)

In December, the number of projects increased by one compared to the previous month. Article 6 labels were issued for Cookstoves projects in Gambia and Laos, and a renewable energy project in Togo. The Issuance from Laos was not only the largest for December but also the largest volume of Article 6 labeled Credits issued from Laos to date. Furthermore, the Issuance from Togo marks the first Article 6 labeled Credit Issuance from the country in two years.

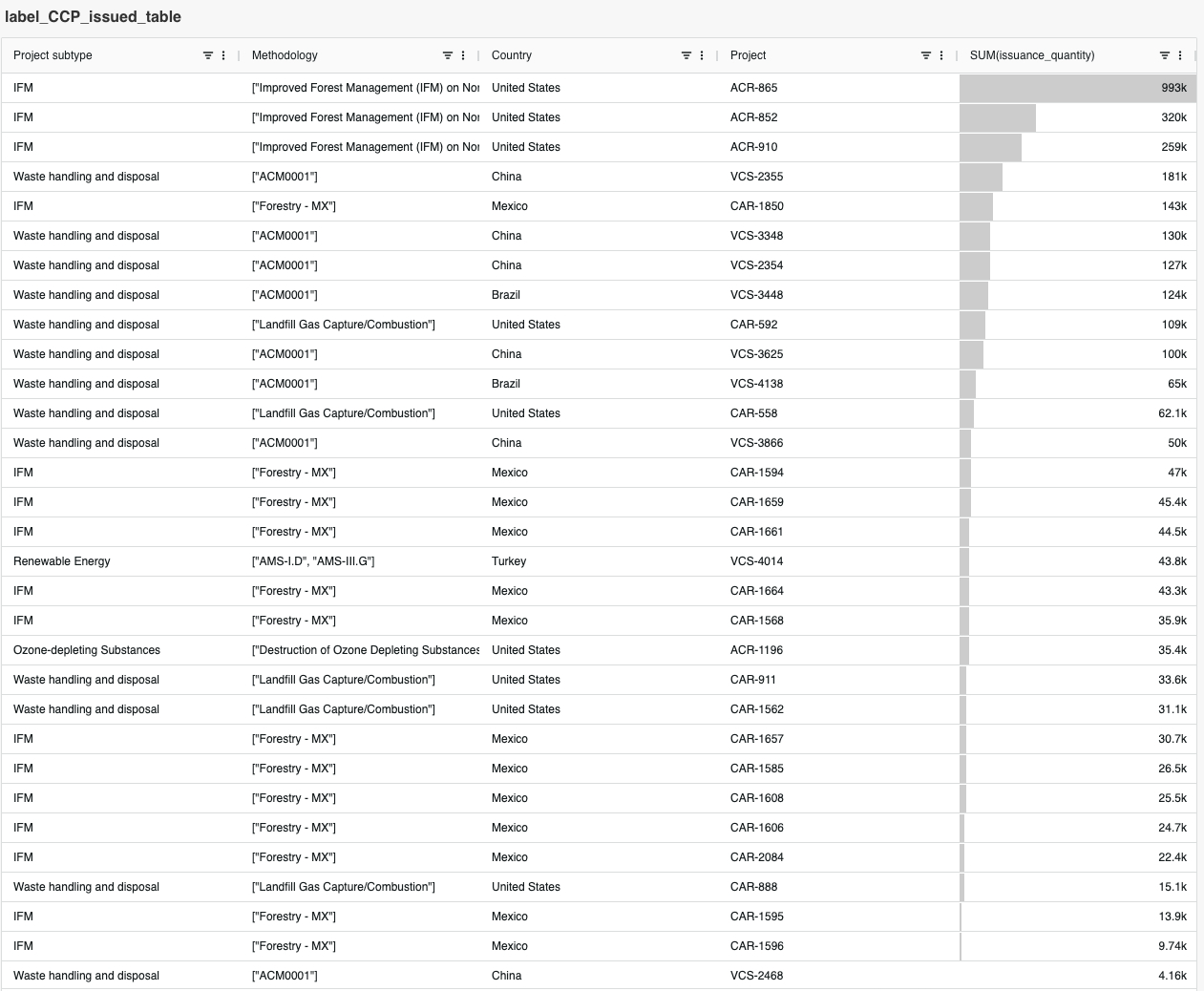

Label Issuance Performance (Core Carbon Principles - CCP)

Regarding Core Carbon Principles (CCP) labels, the number of projects in December significantly increased. They were issued for Improved Forest Management (IFM) projects in the US and Mexico, waste management projects in the US, Brazil, and China, ozone-depleting substance projects in the US, and renewable energy projects in Turkey. As in the previous month, the largest Issuance volume was for US IFM projects, totaling 933,000 units. Additionally, the project in Turkey recorded 43,800 units, marking the largest Issuance volume of CCP labeled Credits for renewable energy to date.

Label Issuance Performance (Carbon Offsetting and Reduction Scheme for International Aviation - CORSIA)

In December, a total of approximately 2.9 million Carbon Offsetting and Reduction Scheme for International Aviation (CORSIA) labels were issued for the aforementioned Article 6 labeled Cookstoves projects in Laos (VCS-2924) and Gambia (VCS-4000) (Phase 1, Vintage 2024-2026). For Phase 1 (2024-2026), an LoA (Letter of Authorization) is required for all Vintages (2021-2026). Since an LoA is required for the Credits confirmed for Issuance this time, we have confirmed that Laos and Gambia had each issued an LoA as of 2024.

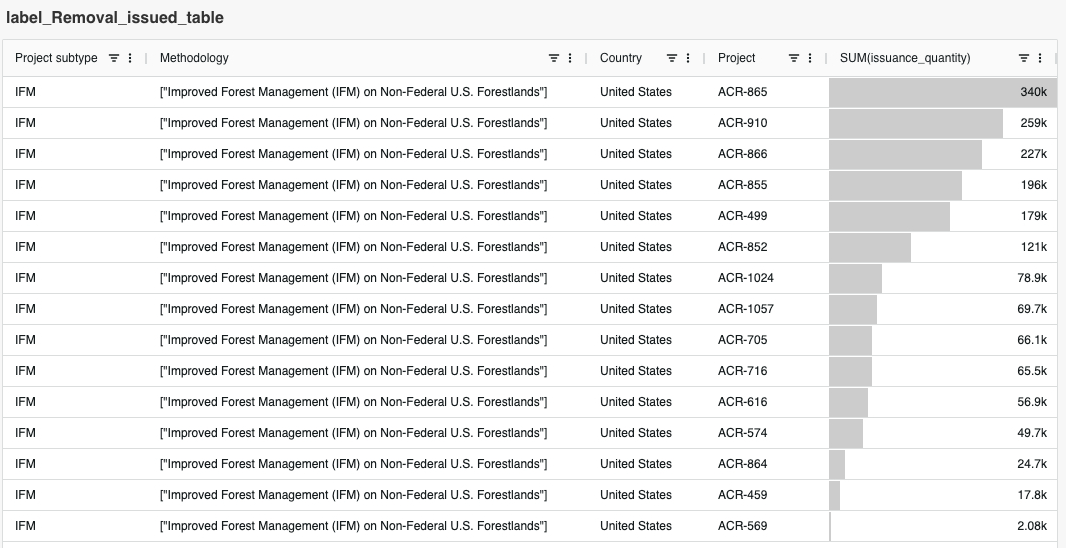

Label Issuance Performance (Removal)

Finally, regarding Removal labels, as in the previous month, Issuances occurred for US Improved Forest Management (IFM) projects (all American Carbon Registry (ACR)) in December. The largest Issuance volume was for the aforementioned project with a Core Carbon Principles (CCP) label (ACR-865), totaling 340,000 units. Looking at cumulative Issuance performance to date, US IFM projects account for approximately 90%.

<List of Retired Projects>

The list of the top 10 nature-based projects with the highest Retirement volumes in December 2025 is as follows:

The largest Retirement was confirmed for a Reducing Emissions from Deforestation and Forest Degradation (REDD) project in Guatemala (VCS-1622), with over 540,000 units retired. Following that, a REDD project in the Democratic Republic of Congo (VCS-934) saw over 450,000 units retired.

<List of Retiring Companies>

The top 10 companies that retired Carbon Credits from nature-based projects in December 2025 are as follows:

The company that retired the most was Shell, a British energy and petrochemical group, with approximately 900,000 units. To date, the company has cumulatively retired 3.54 million units from Reducing Emissions from Deforestation and Forest Degradation (REDD) and nature restoration projects. These include the large-scale REDD projects Katingan (VCS-1477) in Indonesia and Cordillera Azul (VCS-985) in Peru.

<Investment Trends in Nature-based and CDR Projects>

- Target Projects: Investments in nature-based and Carbon Dioxide Removal (CDR) are covered.

- Target Period: December 2025

Notes: For "Credits" and "Group investment" fields, only publicly announced figures are recorded, so there may be blanks. In this table, "Beneficiary" refers to the investing company or the company purchasing the Credits, and "Investment into" indicates whether the investment target is a project or a fund.

In December, there were 19 significant investments in nature-based and Carbon Dioxide Removal (CDR) projects. For details on these, please refer to Section A-3: Detailed Commentary Section.

A-2: Project Pipeline Analysis

- Target Registries: Verra / Verified Carbon Standard (VCS), Gold Standard (GS), Climate Action Reserve (CAR), American Carbon Registry (ACR), Architecture for REDD+ Transactions (ART-TREES), Puro.earth, Isometric

Target Projects: Pipelines related to nature-based solutions and Carbon Dioxide Removal (CDR)

Target Period: October-November 2025

Notes: Please be aware that there may be a slight time lag in reflecting data in the registries, so the number of projects or their status may change for the current reporting period.

Terminology: Annual ER refers to annual Emission Reductions / Removals (tCO₂e).This section covers new Pipeline projects for nature-based solutions and Carbon Dioxide Removal (CDR) from last month, as well as updates to the Pipeline from the month before last, which were introduced in the previous newsletter.

Please note that the application dates (Listing Date) in this database are either directly obtained from registries or estimated. Therefore, we do not guarantee the completeness or accuracy of the data.

<Nature-based Project Pipeline>

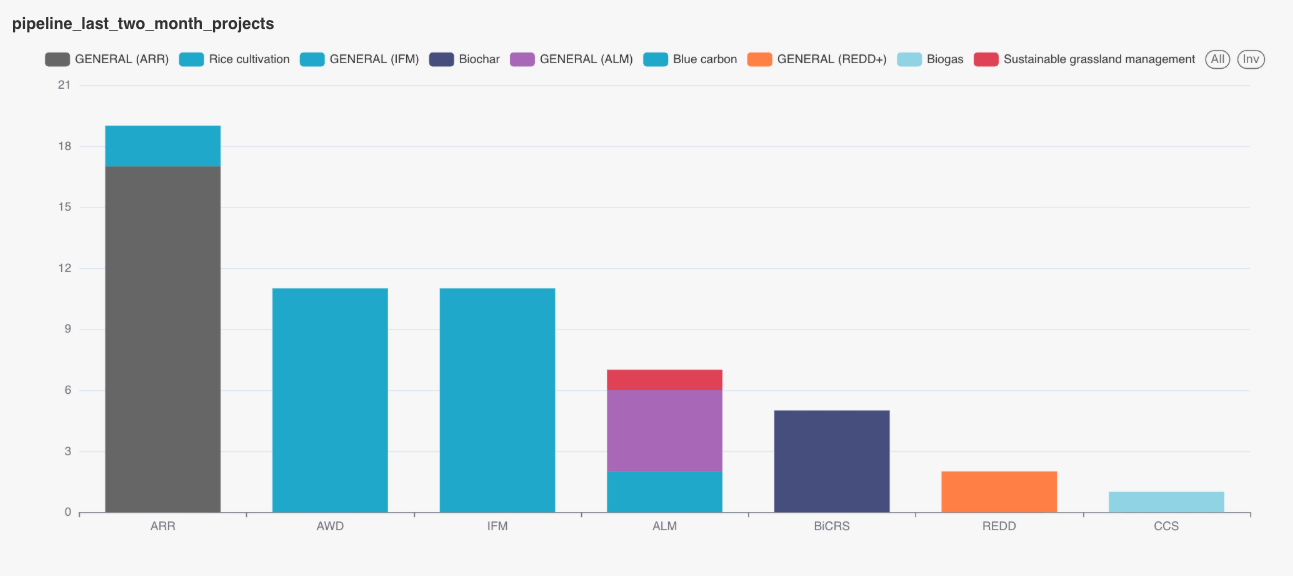

The December 2025 Pipeline includes 57 projects, while the November Pipeline was updated after last month's newsletter was published and now contains 30 projects.

Throughout these two months, Afforestation, Reforestation and Revegetation (ARR) projects accounted for the largest number of projects. Many of these are projects under Verra / Verified Carbon Standard (VCS) (Brazil and Zambia) and Gold Standard (GS) (India and Italy), among others.

The December Pipeline includes Afforestation, Reforestation and Revegetation (ARR) projects (Zambia, India, Brazil, Indonesia, Senegal, Italy, Argentina), Reducing Emissions from Deforestation and Forest Degradation (REDD) projects (Brazil), Agricultural Land Management (ALM) projects (Rwanda, US), and Improved Forest Management (IFM) projects (Mexico, US). Due to potential time lags in information sharing by registries, the November Pipeline was updated with 10 additional projects after the previous month's newsletter was written, adding a Reducing Emissions from Deforestation and Forest Degradation (REDD) project in Paraguay, two Afforestation, Reforestation and Revegetation (ARR) projects in India, ARR projects in Ghana, Guam, France, and the US, and Agricultural Land Management (ALM) projects in Myanmar, Thailand, and Romania.

The emergence of new Pipeline projects in Brazil, Zambia, and Rwanda indicates that policy preparations in host countries are progressing, and actual supply is beginning to materialize under newer, more reliable Methodologies.