Monthly: VCM Updates (March 2024)

This article is an automatically translated version of the original Japanese article. Please refer to the Japanese version for the most accurate information.

This is the newsletter from sustainacraft Inc. While Retirement volumes were not as high as last month, they remain at a high level. We will report on the activities of companies undertaking notable Retirements. Regarding regulatory trends, we will cover announcements from the Science Based Targets initiative (SBTi) and the U.S. Securities and Exchange Commission (SEC) concerning planning and disclosure.

Monthly VCM Update

This month's topics include:

A. Voluntary Carbon Credit Market Trends

- Issuance / Retirement Analysis

- Project Pipeline Analysis

B. Major Overseas Regulatory Trends

- SBTi Releases Report on Beyond Value Chain Mitigation (BVCM)

- U.S. Securities and Exchange Commission (SEC) Adopts Rule Proposal to Enhance and Standardize Climate-Related Disclosures for Investors

A. Voluntary Carbon Credit Market Trends (Verra)

Reference: We have published a market trends report on Voluntary Carbon Credits up to the end of 2023, which was used in a seminar at the end of last year (English version, Japanese version).

1) Issuance / Retirement Analysis

(Correction and Apology, Added 2024.4.22) There was an error in the monthly aggregation below, which has been corrected.

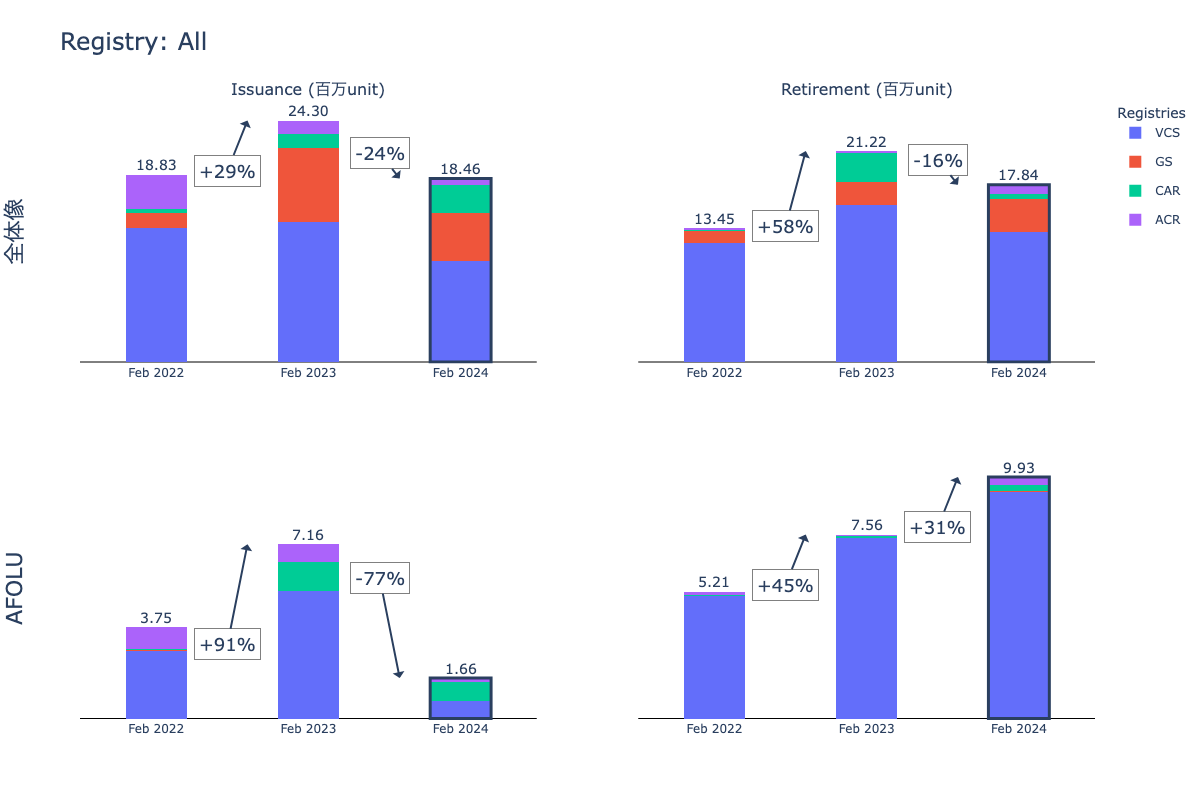

In February 2024, Voluntary Carbon Credits in the Verra, Gold Standard (GS), Climate Action Reserve (CAR), and American Carbon Registry (ACR) registries saw 18.46 million units newly Issued and 17.84 million units Retired. These figures represent a year-over-year change of -24% and -16% respectively.

For Agriculture, Forestry and Other Land Use (AFOLU) projects specifically, 1.66 million units were Issued and 9.93 million units Retired. These figures represent a year-over-year change of -77% and +31% respectively.

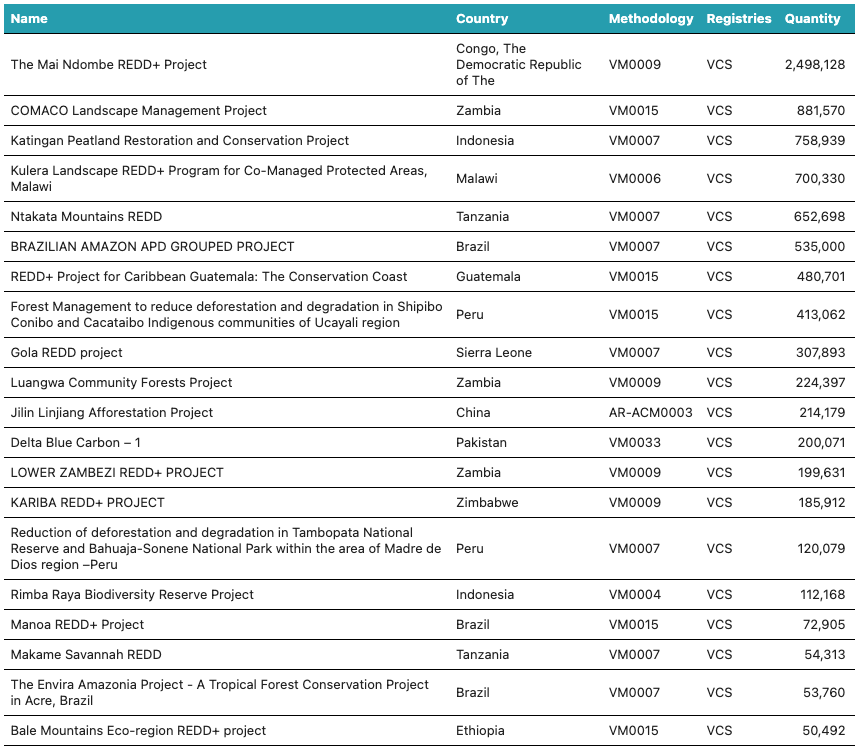

Following January, Verra's new Issuance volume continues to decrease significantly. Below is a list of Verra projects (AFOLU sector only) Retired in February 2024. The top 20 projects account for 90% of total Retirements. By country, Congo is the largest (26.8%), followed by Zambia (14%), Indonesia (10%), Brazil (9%), and Tanzania (8%). The Mai Ndombe REDD+ project, which saw the largest number of Credits Retired, was largely Retired by the Italian oil company Eni.

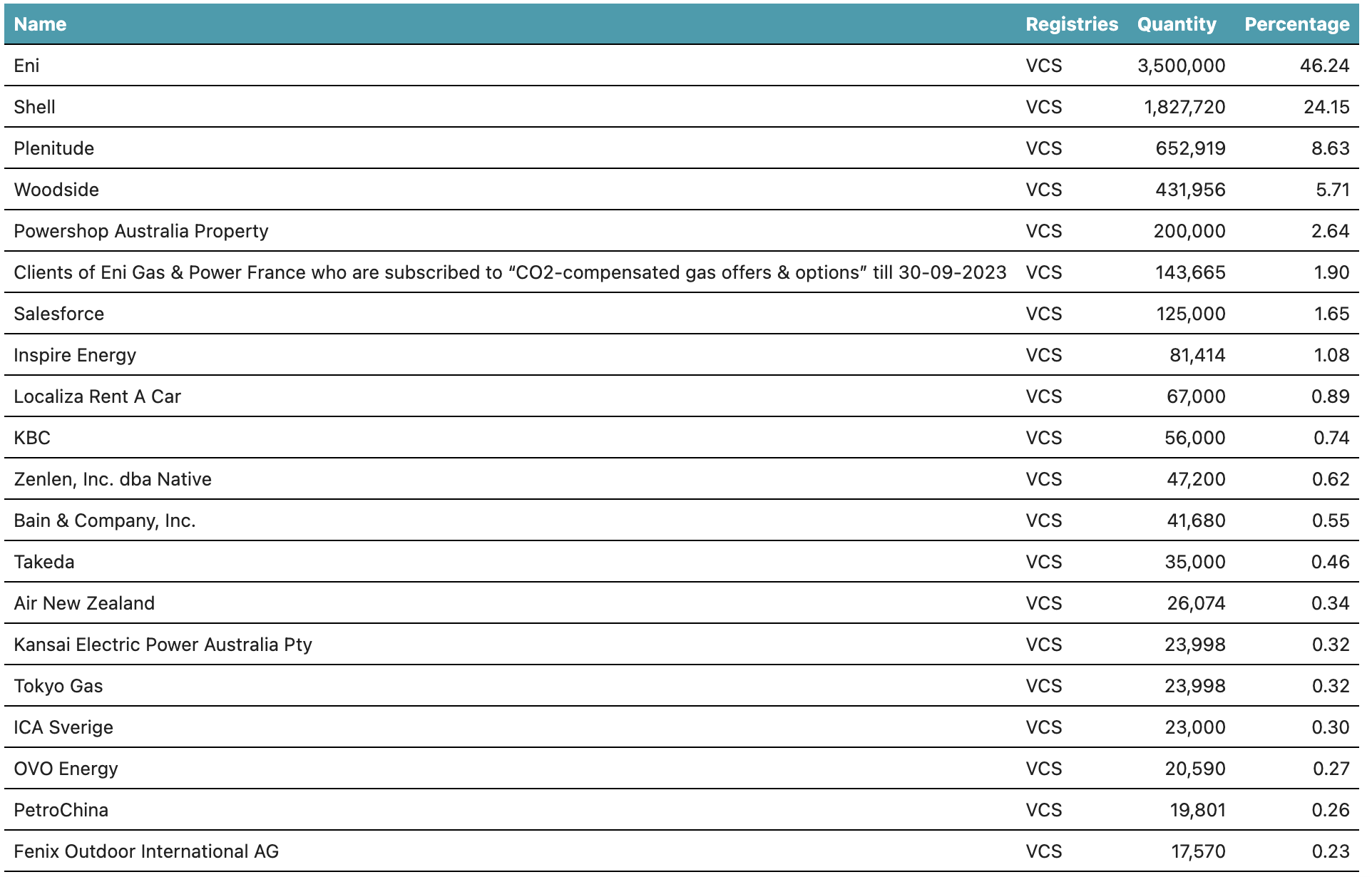

The top 20 companies that Retired Carbon Credits from Verra's AFOLU sector are listed below. In February 2024, Eni's Retirements were the largest. Plenitude, ranked 3rd, is an Eni affiliate handling renewable energy, and it is also noted in 6th place that Eni's customers used Credits for Offset, indicating an aggressive Retirement policy. Additionally, Australian oil company Woodside Retired a large number of Credits.

Eni has announced its Greenhouse Gas (GHG) Emission Reduction targets as follows: -65% (Scope 1+2) by 2025 compared to 2018, -35% (Scope 1+2+3) by 2030, -80% (Scope 1+2) and -50% (Scope 1+2+3) by 2040, and Net Zero including Scope 3 by 2050. Within this, the company plans to Offset Carbon Dioxide (CO2) emissions of 15M, 20M, and <25MtCO2 by 2030, 2040, and 2050 respectively. (Source)

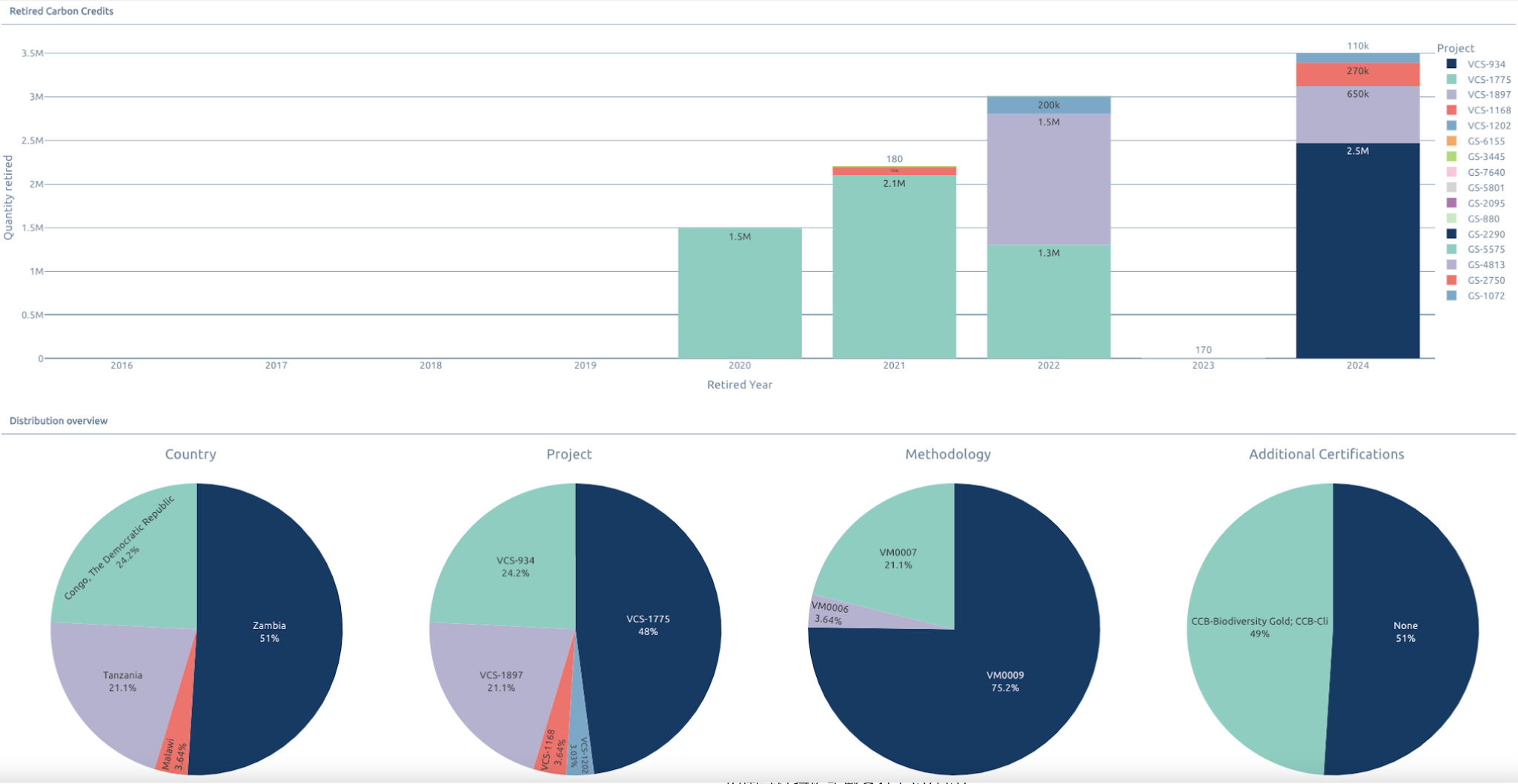

Regarding historical Carbon Credit Retirements (Verra and Gold Standard shown below), Credits from REDD projects in Zambia, Tanzania, and Congo account for the majority. In February 2024, the largest Retirement to date, 3.5M, occurred, with the majority coming from REDD projects in Congo.

Eni is not only sourcing Credits but has also announced its involvement in the development of REDD+ and Cookstoves projects in Vietnam and Rwanda, as follows:

- April 2022: Signed a Memorandum of Understanding (MoU) with the Quang Tri Provincial People's Committee in Vietnam to assess potential opportunities for REDD+ (Reducing Emissions from Deforestation and Forest Degradation) initiatives and natural climate solutions (NCS) for Carbon Credit generation in the region.

- December 2023: Initiated the distribution of household Cookstoves in Rwanda. The goal is to supply and monitor 500,000 improved cooking stoves over the next 10 years, aiming to reduce CO2 emissions and improve health conditions during cooking.

On the other hand, oil companies including Eni face criticism for environmental destruction caused by their past oil development, such as in the Niger Delta region mentioned below:

- Shell began exploration in the 1930s, followed by multiple oil majors, including Eni, commencing operations.

- May 2023: A new report announced that oil and gas companies, led by Shell, Eni, Chevron, Total, and ExxonMobil, had spilled 110,000 barrels of oil in Nigeria's Bayelsa state over the past 50 years.

- September 2023: Eni sold its wholly-owned subsidiary NAOC Ltd., which focuses on onshore oil and gas exploration, production, and power generation in Nigeria, to Nigerian company Oando PLC.

This month, in the same region, a 30-year agreement was announced by Serendib Capital from the UK to restore Mangrove and seagrass beds (Source). This initiative is expected to absorb approximately 5 million tons of carbon annually through the Avoidance of 250,000 hectares of deforestation and the Reforestation of 20,000 hectares. The article suggests that oil majors could become Offtakers for Carbon Projects in areas potentially impacted by their own operations, from the perspective of financing these projects.

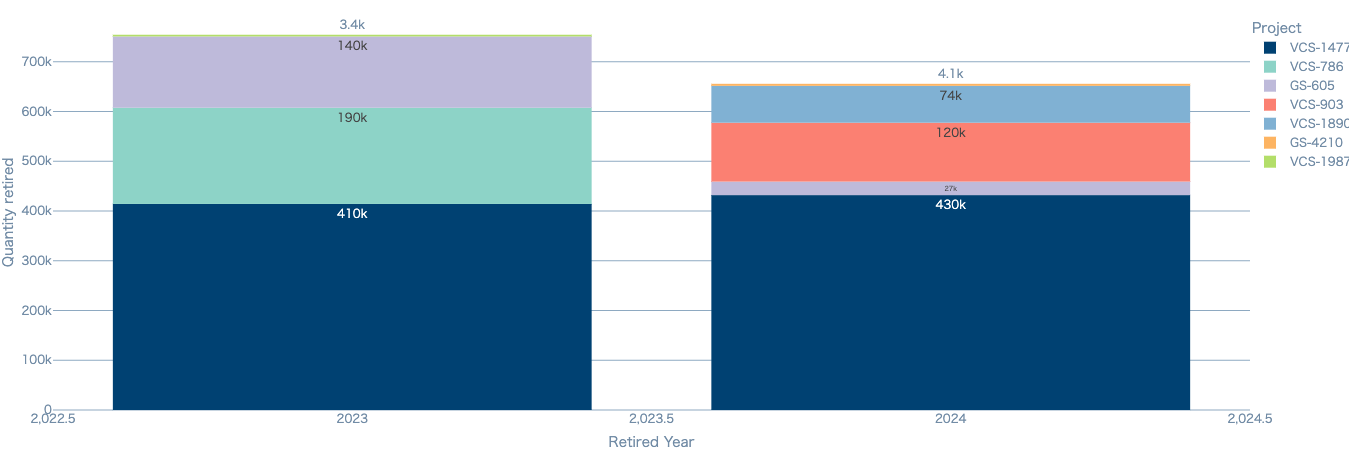

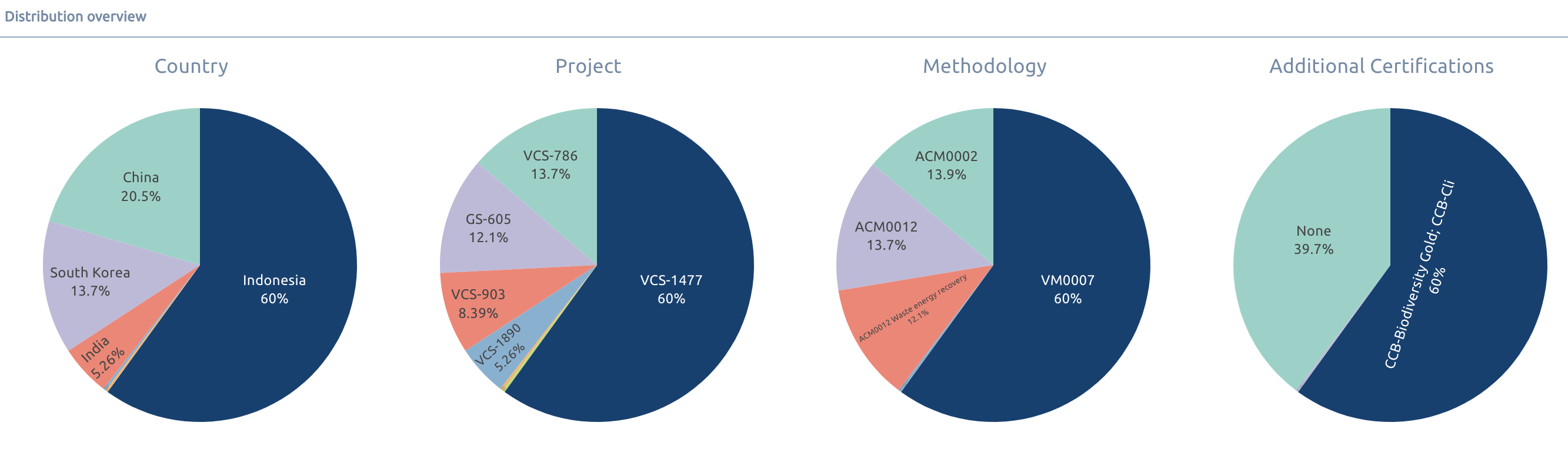

The breakdown of Retirements by Australian oil company Woodside, which saw significant Retirements in February 2024, is as follows: since 2023, the company has Retired Credits generated from projects in regions outside Australia, such as Indonesia, South Korea, China, and India (this only includes Verra and Gold Standard, not ACCUs). Indonesia, which accounts for a large proportion, primarily features Credits from the Katingan project (VCS-1477), which Shell and others also Retire.

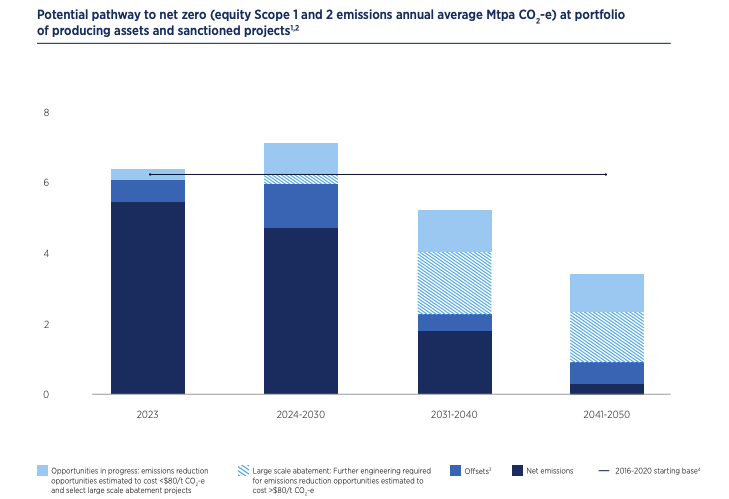

Woodside's 2023 Sustainability Report outlines an aspiration to reduce Scope 1 and 2 emissions by 30% by 2030 and achieve Net Zero by 2050. The reduction plan involves combining reduction initiatives that can be implemented at a cost below an internal carbon price of $80/t-CO2e with Offsets until 2030, and from 2040 onwards, adding projects including Carbon Capture, Utilization, and Storage (CCUS) exceeding $80/t-CO2e. The company plans to procure over 1 million t-CO2e of Credits annually from 2024 to 2030. The importance of Credits is highlighted as a hedging tool against risks such as fluctuating emissions, delays in reduction plans, and insufficient improvements in the cost-efficiency of Carbon Dioxide Removal (CDR) technologies. Furthermore, by building Carbon Credit management capabilities and a procurement portfolio, Woodside aims to hedge against the risk of rising regulatory carbon prices.

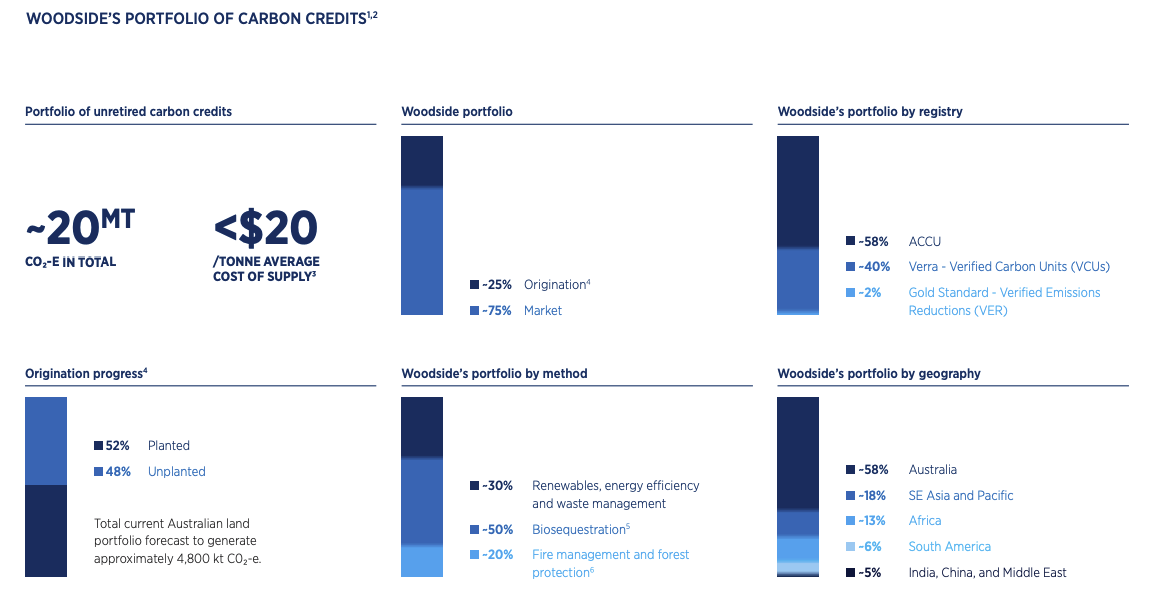

Woodside commenced its Carbon Credit business in 2018, investing a cumulative $150M in Carbon Credits, with one-third disclosed as proprietary projects. Its current portfolio is approximately 20M t-CO2e in size, with an average supply cost below $20/t, indicating an active stance towards investment in Carbon Projects. Increasing the proportion of Project Development is said to contribute to accumulating in-house expertise in managing acquisition costs and quality.

The acquired Credits are composed of 58% Australian Carbon Credit Units (ACCUs), which are domestic Australian Credits, and 40% Verra. ACCUs are acquired domestically in Australia, while Voluntary Carbon Credits are procured for other regions.

Currently, Avoidance and Emission Reduction Credits constitute the majority, but the company plans to focus more on Removal/Sequestration in the future, with a policy to make Nature-based Solutions (NbS) account for 50% of its portfolio, indicating an active approach to NbS initiatives.

It is important to note the context that this report was issued in response to criticisms from some climate-related organizations prior to its release, regarding the high reliance on Credits for the 2025-2030 reduction targets and the lack of mention of Scope 3. Woodside's report acknowledges some of these risks while emphasizing the importance of Emission Reduction and Avoidance within the Supply Chain. Regarding the use of Credits, the company's policy is to adhere to standards such as the Integrity Council for the Voluntary Carbon Market (IC-VCM), Core Carbon Principles (CCP) (formerly CCPI), and Oxford Principles, prioritize quality assessment, and manage risks through diversification of its Credit portfolio. Furthermore, at the company's general shareholder meeting in 2022, 49% of shareholders voted against the Climate Report's content, and in 2023, opposition to the re-election of some directors intensified due to insufficient climate measures, indicating the strong scrutiny from shareholders regarding climate action.

2) Project Pipeline Analysis

Below shows the monthly Pipeline trends by project sub-type. The upper chart represents the number of projects, and the lower chart is based on annual Emission Reduction (ER) or Removals. The horizontal axis is based on the Listing Date1