Monthly: VCM Updates (April 2024)

This article is an automatically translated version of the original Japanese article. Please refer to the Japanese version for the most accurate information.

This is the newsletter from Sustainacraft Inc.

While the volume of Retirements was not as high as last month, it remained at a high level. We will report on the activities of companies that made notable Retirements. Regarding regulatory trends, we will introduce statements from the Integrity Council for the Voluntary Carbon Market (IC-VCM) regarding Core Carbon Principles (CCP) and from the Science Based Targets initiative (SBTi) regarding Scope 3.

SBTi has issued a statement suggesting the use of environmental attribute certificates (EACs), including Voluntary Carbon Credits, for Scope 3 emission abatement purposes, which has sparked significant discussion. Previously, SBTi only allowed the use of Carbon Credits for "neutralization of Residual Emissions after achieving a long-term target of 90% or more reduction in Scope 1+2+3," with the exception of Beyond Value Chain Mitigation (BVCM). If the revisions suggested in this statement are adopted, companies could see significant changes in both the timing and quantity of Carbon Credit usage compared to previous expectations. Details have not yet been released, with a draft expected in July. It is also important to note that this statement has not been approved by the SBTi Technical Council.

Please contact us here for inquiries.

Announcement: Seminar Held (from 13:00 on Thursday, April 25)

We will hold a quarterly seminar on Thursday, April 25, 2024, from 13:00, looking back at the approximately three months since the New Year. Please check details and register here.

The seminar will cover both quantitative trends regarding Credit Retirement and project Pipeline, as well as qualitative aspects such as key announcements concerning SBTi, CCP, and their impacts.

Monthly VCM Update

This month, we introduce the following content:

A. Voluntary Carbon Credit Market Trends

- Issuance / Retirement Analysis

- Project Pipeline Analysis

B. Key International Regulatory Trends

- IC-VCM announces American Carbon Registry (ACR), Climate Action Reserve (CAR), and Gold Standard (GS) as the first carbon programs to meet Core Carbon Principles (CCP) criteria (link)

- SBTi issues a statement suggesting the use of environmental attribute certificates, including Voluntary Carbon Credits, for Scope 3 emission abatement purposes (link)

A. Voluntary Carbon Credit Market Trends (Verra)

Reference: We have published a market trends report on Voluntary Credits until the end of 2023, which was used in a seminar at the end of last year (English version, Japanese version).

1) Issuance / Retirement Analysis

(Apology and Correction) There was an error in last month's February 2024 tabulation, so we have updated last month's article.

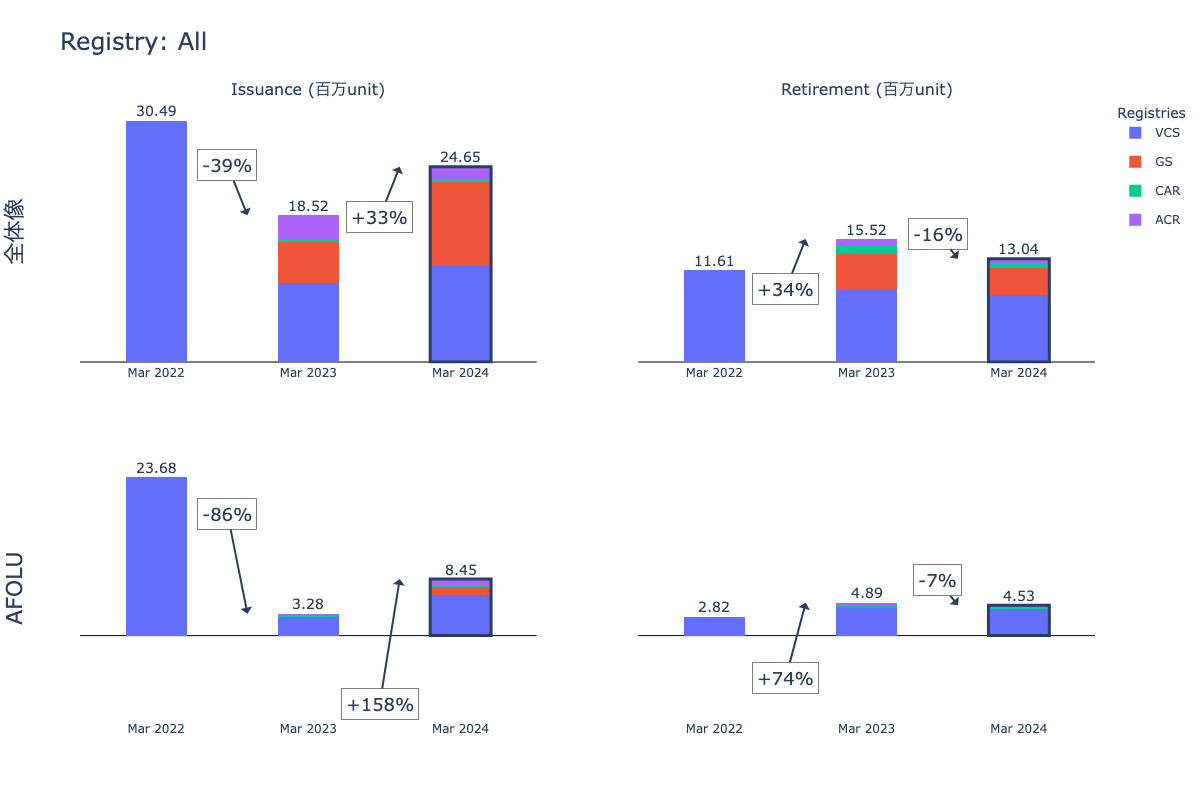

In March 2024, 24.65 million units of Voluntary Carbon Credits were newly Issued, and 13.04 million units were Retired across the Verra, Gold Standard (GS), Climate Action Reserve (CAR), and American Carbon Registry (ACR) registries. This represents a year-on-year change of +33% and -16% respectively. Issuances from GS continued to be high, similar to last month.

For Agriculture, Forestry and Other Land Use (AFOLU) projects alone, 8.45 million units were Issued, and 4.53 million units were Retired. This represents a year-on-year change of +158% and -7% respectively.

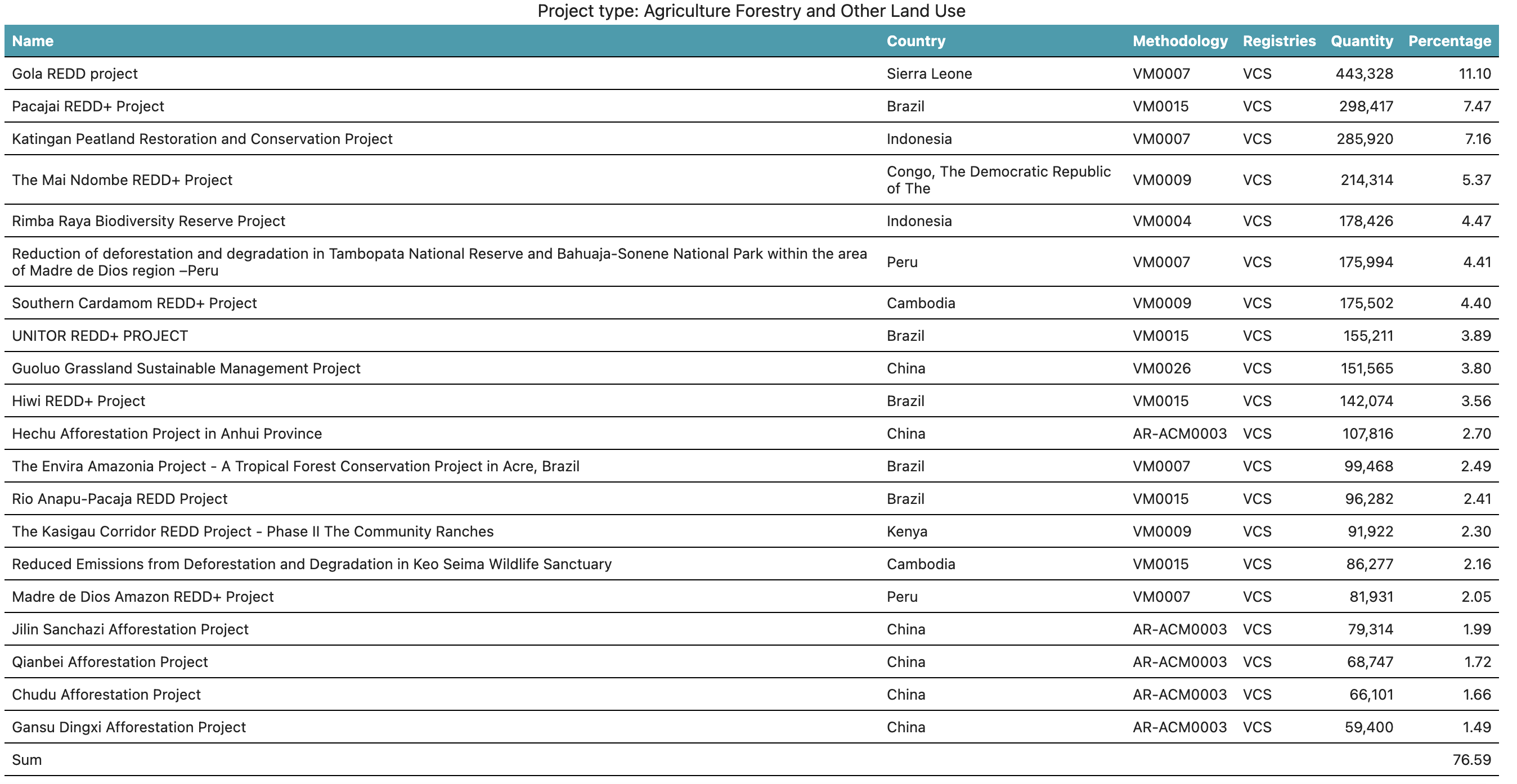

The list of Verra projects Retired in March 2024 (AFOLU sector only) is as follows. The top 20 projects accounted for approximately 80% of total Retirements. The majority were Reducing Emissions from Deforestation and Forest Degradation (REDD+) projects.

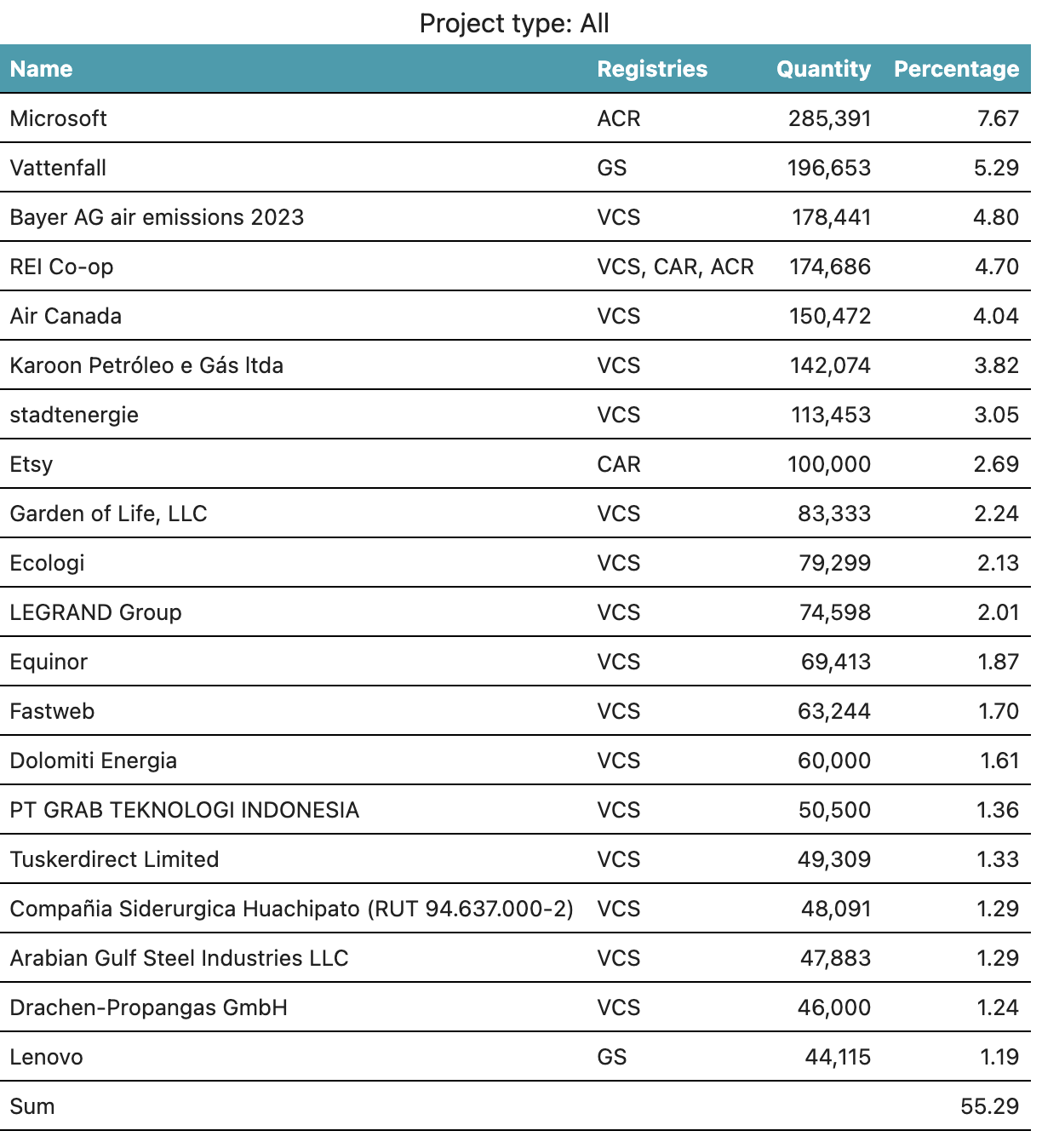

The top 20 companies that Retired Credits in March 2024 are as follows. This list includes projects other than Verified Carbon Standard (VCS) and AFOLU this time.

The top two companies by volume of Retirements are Microsoft and Vattenfall (a Swedish power company), with projects from ACR and GS, respectively. They are followed by pharmaceutical giant Bayer (VCS) and REI Co-op (VCS, CAR, ACR).

Microsoft's Retirements

Technology company Microsoft is taking an ambitious approach to achieve Net Zero by 2030, aiming to Remove from the atmosphere an amount of Carbon equivalent to its historical emissions since its founding in 1975 (Source).

The company's Scope 1+2 emissions are already Net Zero through Power Purchase Agreements (PPAs), green tariff programs, and renewable energy certificates. The latter are being temporarily purchased to Offset some Scope 3 emissions, and the company plans to phase them out across all Scopes in the future (Source).

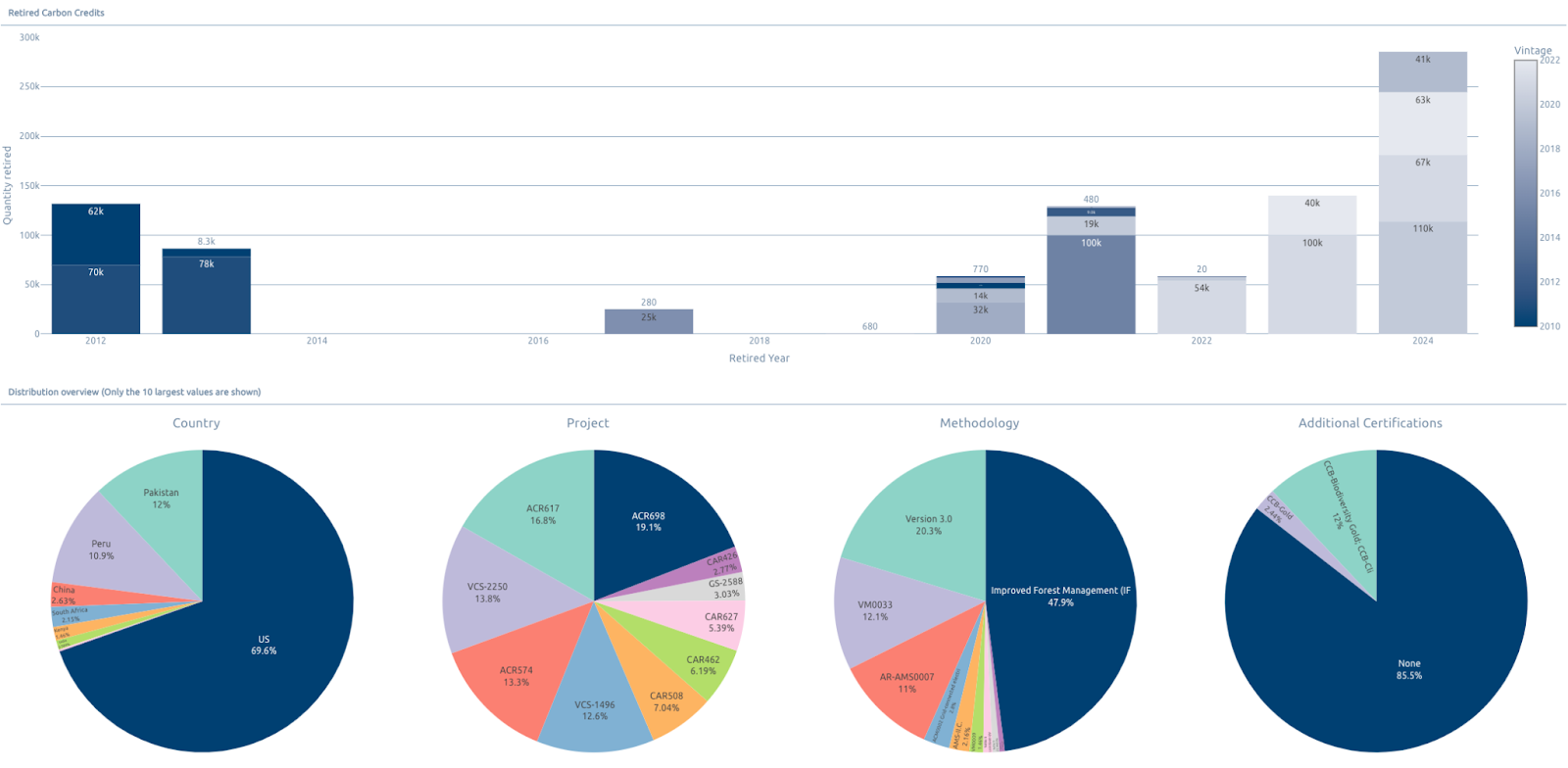

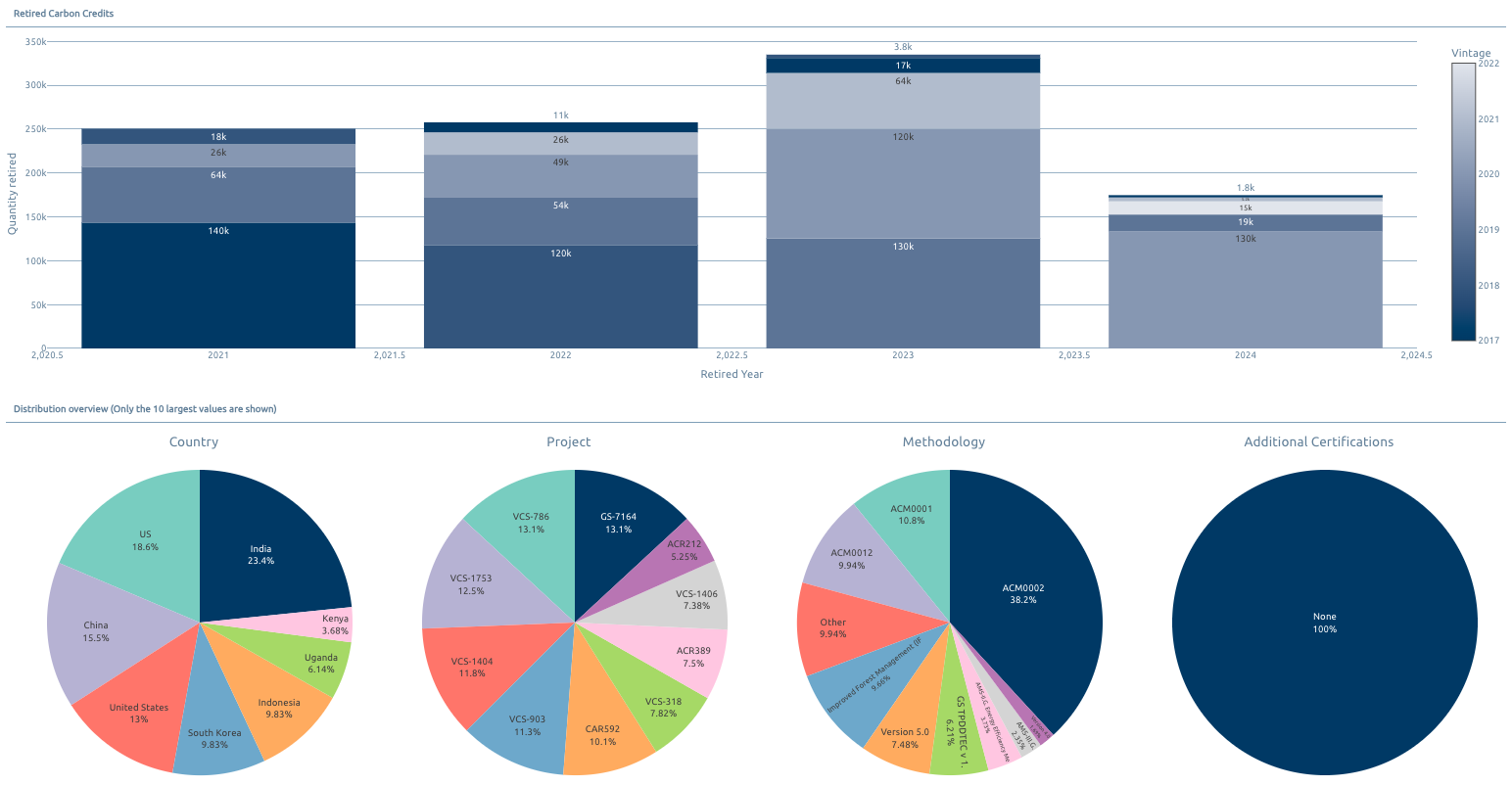

To date, 50% of the company's total portfolio consists of projects from the ACR registry. In March, it Retired Credits from U.S. Improved Forest Management (IFM) projects (ACR-617 and ACR-698). As shown in the graph below, 70% of the Credits Retired by the company to date were generated in the U.S.

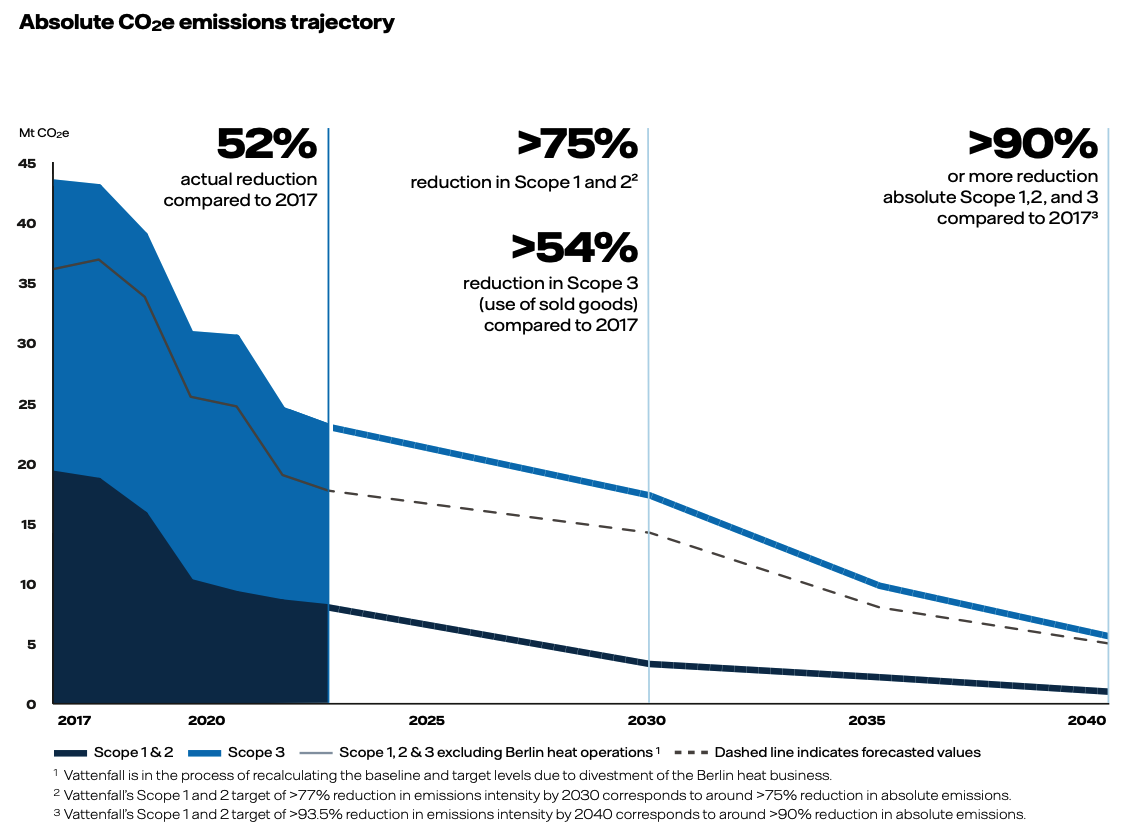

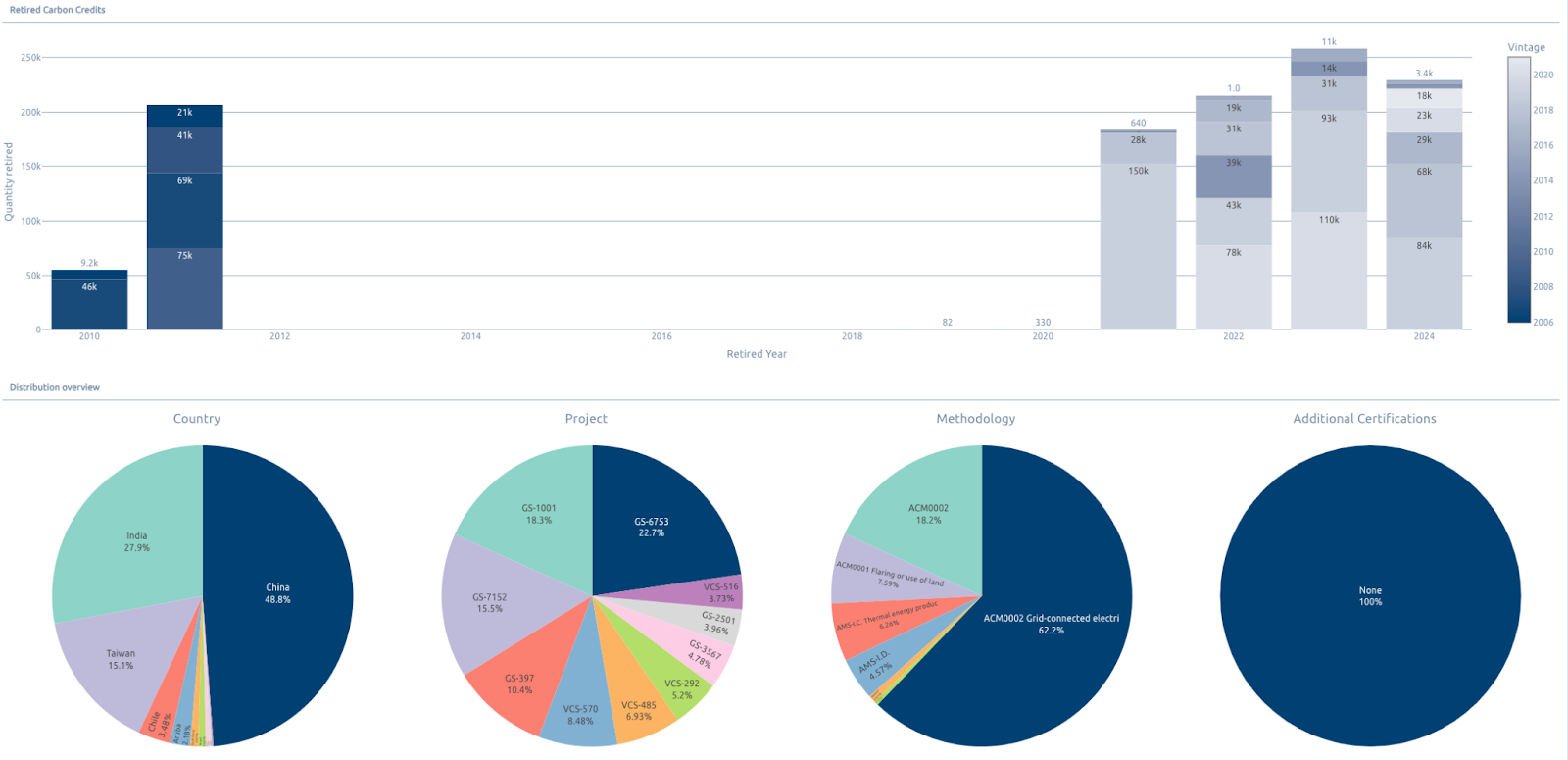

Vattenfall's Retirements

Vattenfall is a Swedish power company that produces electricity from various energy sources, including hydropower, nuclear, wind, solar, biomass, waste, coal, and natural gas (Source). The company's Greenhouse Gas (GHG) Emission Reduction targets are -75% (Scope 1+2) and -54% (Scope 3) by 2030 compared to 2017 levels. Subsequently, it aims to achieve Net Zero by 2040, defined as at least a -90% reduction for Scope 1+2+3, with remaining GHG Emissions planned to be neutralized through Carbon Dioxide Removal (CDR). These targets have been reviewed and approved by SBTi (Source, Source).

75% of the company's total portfolio consists of projects from the GS registry. By country, approximately 50% of its Retired Carbon Credits originate from China, 28% from India, and 15% from Taiwan.

REI Co-op's Retirements

REI Co-op is an American retail company primarily focusing on products for outdoor activities (such as camping and hiking). The company's Greenhouse Gas (GHG) Emission Reduction targets are -47% (Scope 1+2+3) by 2030 compared to 2019 levels. Subsequently, it aims to achieve Net Zero by 2050, defined as a -90% reduction in Scope 1+2+3. These targets have been reviewed and approved by SBTi (Source).

Regarding project composition, the company has a diverse portfolio. It has Retired Credits from various projects, with each accounting for approximately 7% to 13%. VCS accounts for the majority of its registry holdings, but it has also Retired Credits from GS, ACR, and CAR.

According to its published Carbon Credit portfolio report, the company intentionally blended international and domestic projects, with a particular focus on projects with Co-benefits. For example, the Winston Creek Forest Carbon Project (ACR-389, approximately 7.5% of the portfolio) offers Co-benefits such as improved water management and Biodiversity conservation, while the UPM Blandin Native American Hardwood Conservation & Carbon Sequestration Project (ACR-212, 5.2%) provides Co-benefits including improved air quality and community recreation (Source).

Meanwhile, focusing solely on AFOLU projects for comparison with the top companies in last month's newsletter, there were no significant Retirements in March. Incidentally, in February, three oil and gas companies (Eni and its affiliate Plenitude, Shell, and Woodside) Retired over 5 million Credits.

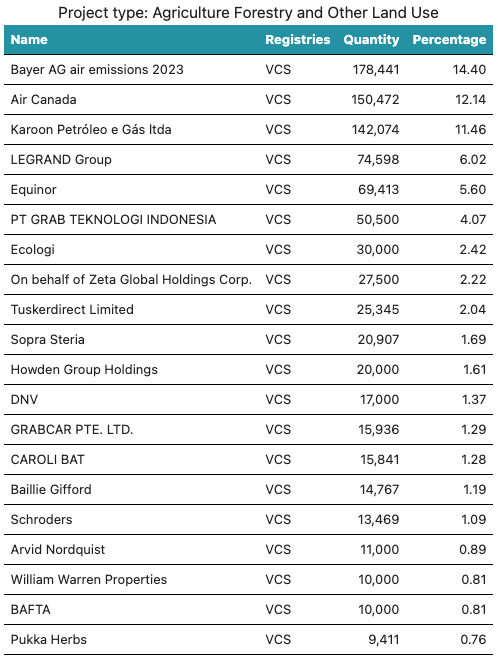

In March, pharmaceutical company Bayer had the highest volume of AFOLU project Retirements, followed by Air Canada and the Brazilian oil and gas company Karoon.

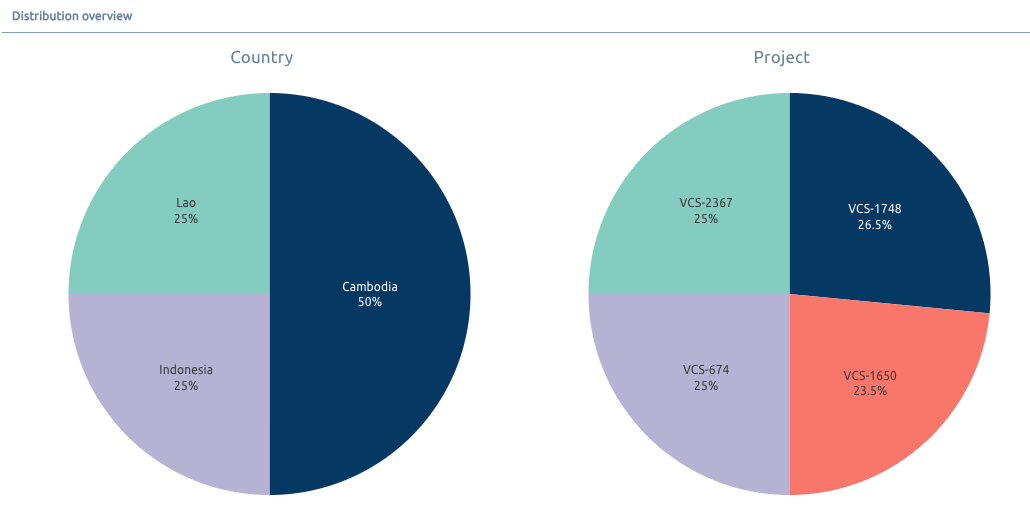

Bayer's Retirements

This represents Bayer's largest Retirement to date and is stated to Offset Emissions from air travel (Source). Half (1/2) came from Cambodian projects VCS-1748 and VCS-1650, one quarter (1/4) from the Laotian project VCS-2367, and the remaining quarter (1/4) from the Indonesian project VCS-674. Details on some of these projects will be discussed later.

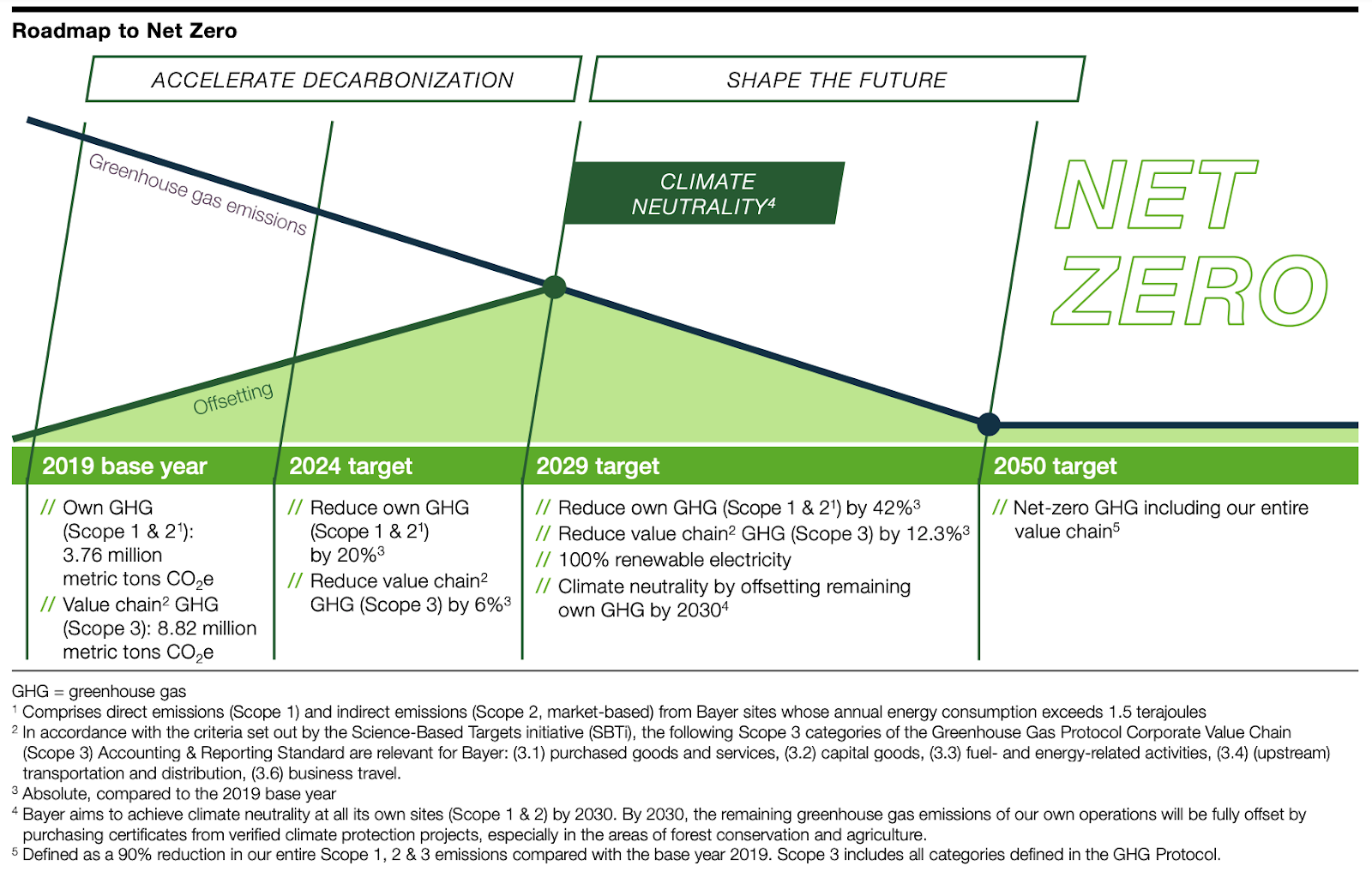

The company has set short-term GHG Emission Reduction targets of -20% (Scope 1+2) and -6% (Scope 3) by 2024, compared to the 2019 baseline. Subsequently, by 2029, it aims to fully Offset Residual Emissions after reductions with forest protection and agriculture-related projects (Source).

Specifically, compared to 2019, the company's GHG Emission Reduction targets are -42% (Scope 1+2) and -12.3% (Scope 3) by 2029, and Net Zero (Scope 1+2+3) by 2050. Net Zero is defined as reducing Greenhouse Gas (GHG) Emissions by -90% and neutralizing the remaining 10%, and these targets have been reviewed and approved by SBTi.

The company aims to primarily Offset Credits generated by Nature-based Solutions (NbS) for climate action, but it also recognizes that such initiatives have faced criticism from the media. Nevertheless, it strives for improved transparency and quality by complying with multiple disclosure requirements (SASB, TCFD, SFDR, GRI, UNGC) and by working closely with and promoting Voluntary Carbon Market initiatives. As an example, the company joined Brazil's Voluntary Carbon Market initiative in 2022 (Source).

The company has consistently Retired Carbon Credits since 2022, with the Kariba REDD+ Project in Zimbabwe (VCS-902, 36.7%) leading its portfolio, alongside the Southern Cardamom REDD+ Project and Keo Seima Wildlife Sanctuary REDD Project in Cambodia (VCS-1748 and VCS-1650, accounting for 17.7% and 10.2% respectively). Other projects include the REDD+ Project in Brazil (VCS-2252, 12.2%), an agroforestry Afforestation, Reforestation and Revegetation (ARR) Project in Laos (VCS-2367, 10.9%), and the Rimba Raya Project in Indonesia (VCS-674, 10.9%). Other countries such as Nicaragua and Uruguay are also mentioned in its Offset report.

The Kariba project in Zimbabwe (VCS-902) and the Southern Cardamom project in Cambodia (VCS-1748) constitute a significant portion of its portfolio. These projects are very large-scale, and while multiple major companies have Retired Credits from them, project VCS-902 has drawn significant attention due to allegations of trophy hunting and financial irregularities, and VCS-1748 due to human rights concerns. We will cover these issues comprehensively on another occasion.

While the pharmaceutical industry has not historically been a major player in Voluntary Credits, several international pharmaceutical companies are successively announcing large-scale investments in forest regeneration projects and other initiatives, indicating an accelerating trend to secure Removal Credits for neutralizing Residual Emissions after achieving SBTi's long-term targets.

2) Project Pipeline Analysis

Below shows the monthly Pipeline trends by project sub-type. The upper chart shows the number of projects, and the lower chart is based on annual ER (Emission Reduction or Removals). The horizontal axis is based on Listing Date1