Monthly VCM Updates: June

This article is an automatically translated version of the original Japanese article. Please refer to the Japanese version for the most accurate information.

This is Sustainacraft Inc.'s newsletter. This issue delivers a Monthly VCM Update, focusing primarily on topics related to the Voluntary Carbon Market and international regulations announced in May 2023.

Monthly VCM Update

This month, we introduce the following topics:

A. Voluntary Carbon Credit Market Trends

- Trove Research Report: “Corporate emission performance and the use of carbon credits”

B. Major International Regulatory Developments

- Zimbabwe: Immediate Invalidation of Domestic Carbon Credit Contracts Declared

- Class Action Lawsuit Against Delta Airlines' Environmental Claims

- Discussion on Engineered CDR

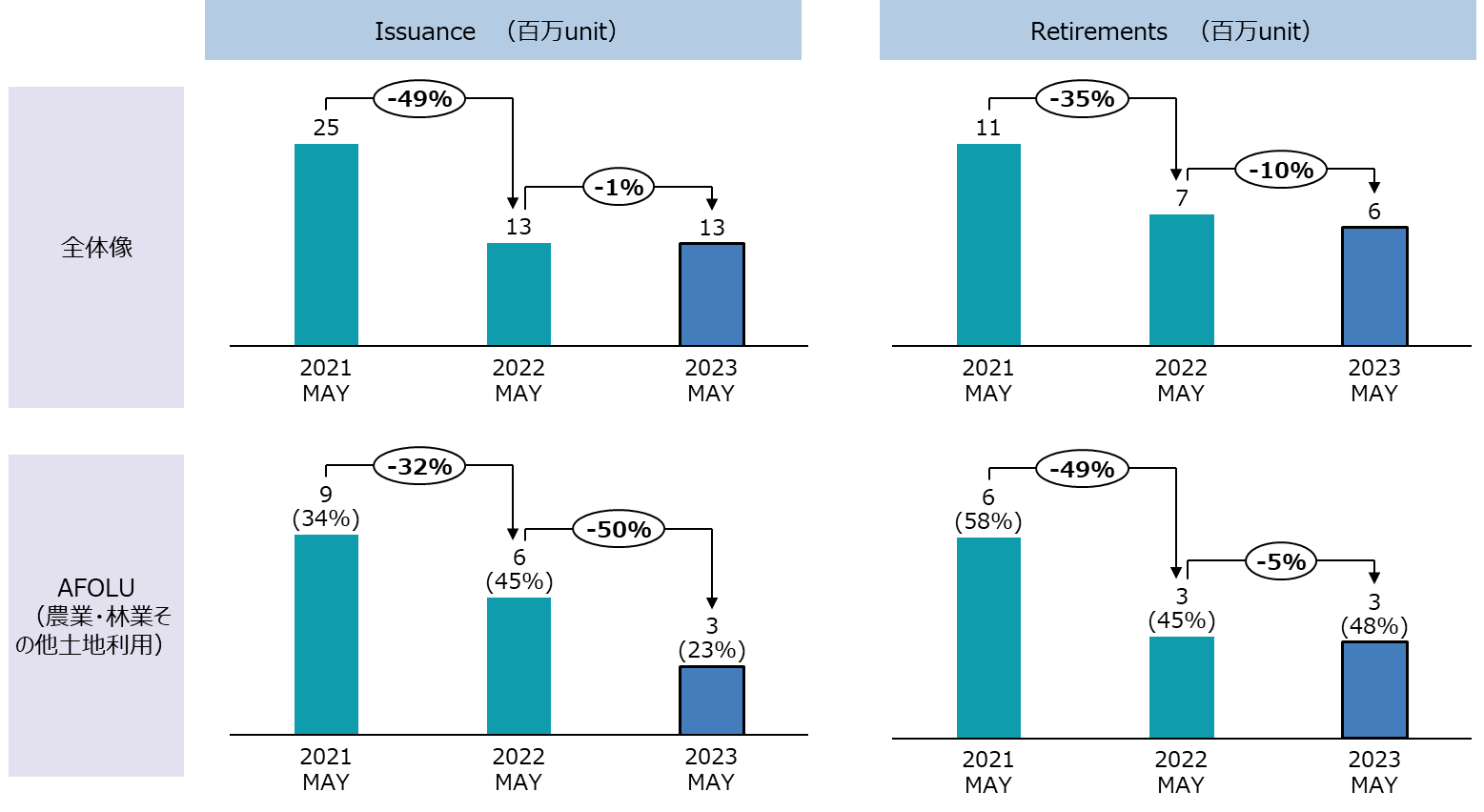

A. Voluntary Carbon Credit Market Trends (Verra)

In May 2023, 12,844,883 Verra Voluntary Carbon Credit units were newly Issued, and 6,267,040 units were Retired. This represents a decrease of -1% and -10% respectively compared to the same month last year.

Focusing on the AFOLU (Agriculture, Forestry and Other Land Use) sector, 2,936,112 units were Issued and 2,996,204 units were Retired. These figures represent a decrease of -50% and -5% respectively compared to the same month last year.

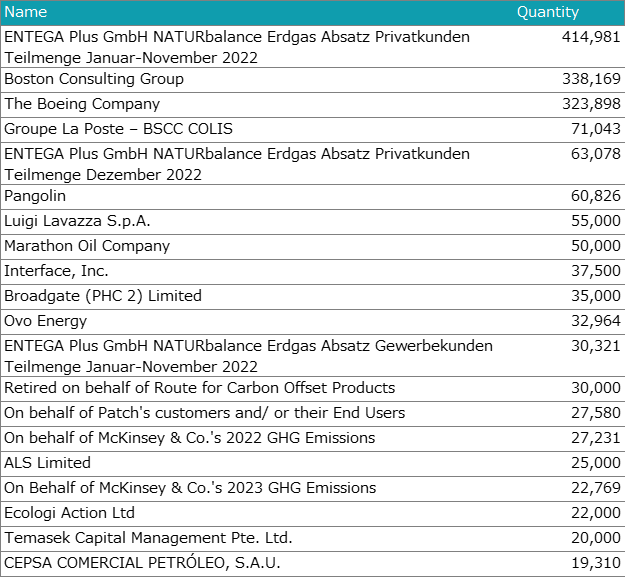

This is a list of projects Retired in May 2023 (AFOLU sector only). The top 20 projects accounted for 80% of all Retirements. By country, Brazil was the largest (46%), followed by Indonesia (10%), Peru (10%), Cambodia (9%), and Uruguay (4%).

The top 20 companies that Retired Carbon Credits in the Verra AFOLU sector are listed below. Companies from the Energy, Consulting, Manufacturing, and Postal Service industries made Retirements.

A-1: Trove Research Report: “Corporate emission performance and the use of carbon credits”

(Source: Trove Research)

On June 1st, Trove Research released a report titled “Corporate emission performance and the use of carbon credits.” The report attempts a quantitative verification of a constantly debated point regarding Carbon Credits: whether purchasing them acts as a "license to pollute" for companies (as stated in the report).

The conclusion refutes the above claim. Specifically, it has been quantitatively demonstrated that **companies utilizing Carbon Credits are significantly more advanced in their own Emission Reduction efforts** compared to companies that do not. This trend holds true across industries and company regions. On average, the Emission Reduction rate for companies using Carbon Credits was -6%, while for those not using them, it was -3%.

The analytical approach was straightforward: calculate the change in Scope 1 and 2 emissions for each company between 2017 and 2022, and then analyze the relationship between the resulting Emission Reduction rate and each company's Credit purchases. "Companies utilizing Carbon Credits" were defined as those that used 100 tCO2e of Credits annually and Offset at least 5% of their Scope 1 and 2 emissions.

Why do companies that purchase Carbon Credits also achieve their own Emission Reductions more quickly? The report suggests that companies purchasing Carbon Credits are **voluntarily assigning a price to their emissions.** In other words, when companies purchase Carbon Credits for voluntary Offsetting purposes, the more they advance their Emission Reductions through their own efforts, the less Carbon Credits they need to procure. This helps companies in their investment and budget approval processes for initiatives aimed at reducing their own emissions.

B. Major International Regulatory Developments

This section reports on important regulatory updates concerning the usage and quality of Voluntary Carbon Credits, as well as the protection of forests and natural resources.