Verra's ALM/IFM Methodology Minor Update

This article is an automatically translated version of the original Japanese article. Please refer to the Japanese version for the most accurate information.

This is a newsletter from sustainacraft Inc.

Methodology Updates is a series that covers carbon and biodiversity Credit Methodologies. This article introduces two Verra Methodology updates announced from last month to this month.

- Revised version (v2.2) of VM0042 Methodology for Improved Agricultural Land Management (IALM)

- Publication of VT0015 Calculation of Reductions and Removals for VM0003, VM0005, VM0012, and VM0034, v1.0, a common carbon accounting tool for IFM methodologies

For inquiries, please contact us here.

*Author of this article: Nick Lau (Applied Scientist)

Introduction

This month, Verra introduced two changes impacting Project Developers of agricultural and forestry projects.

One is the release of VM0042 Methodology for Improved Agricultural Land Management v2.2. This updates methods for demonstrating Additionality, selecting Emission Factors, monitoring Soil Carbon, and quantifying Leakage in agricultural projects. Although described as "minor" changes, they encompass various updates. Specifically, these include stricter data requirements, clearer Common Practice Tests, reduced burden for Soil Organic Carbon (SOC) monitoring through the allowance of Digital Soil Mapping, and changes to Leakage quantification methods. These changes may result in a partially increased reporting burden for Project Developers and potential changes in the volume of issued Credits.

The second is the introduction of VT0015 Calculation of Reductions and Removals for VM0003, VM0005, VM0012, and VM0034. Currently, Verra's Improved Forest Management (IFM) methodologies consist of multiple methodologies with different target activities and eligible regions, each adopting a different format. VT0015 enables unified carbon accounting across the four existing IFM methodologies. While there are no major changes to the Credit calculation itself, Project Developers will now need to report results using standardized monitoring parameters and clearly distinguish between Emission Reductions and Removals. Furthermore, Projects seeking labeling of mitigation outcomes may need to utilize updated reporting templates, carefully map existing model outputs to the VT0015 structure, and potentially perform retrospective recalculations.

These updates enhance the transparency and consistency of Verra's overall Agriculture, Forestry and Other Land Use (AFOLU) portfolio, and Project Developers should anticipate increased analytical and reporting procedures in future project development and reporting.

The two revisions are explained in detail below.

1. VM0042: Revision of the IALM Methodology

<Source: https://verra.org/vm0042-update-verra-publishes-minor-revisions-to-ialm-methodology/>

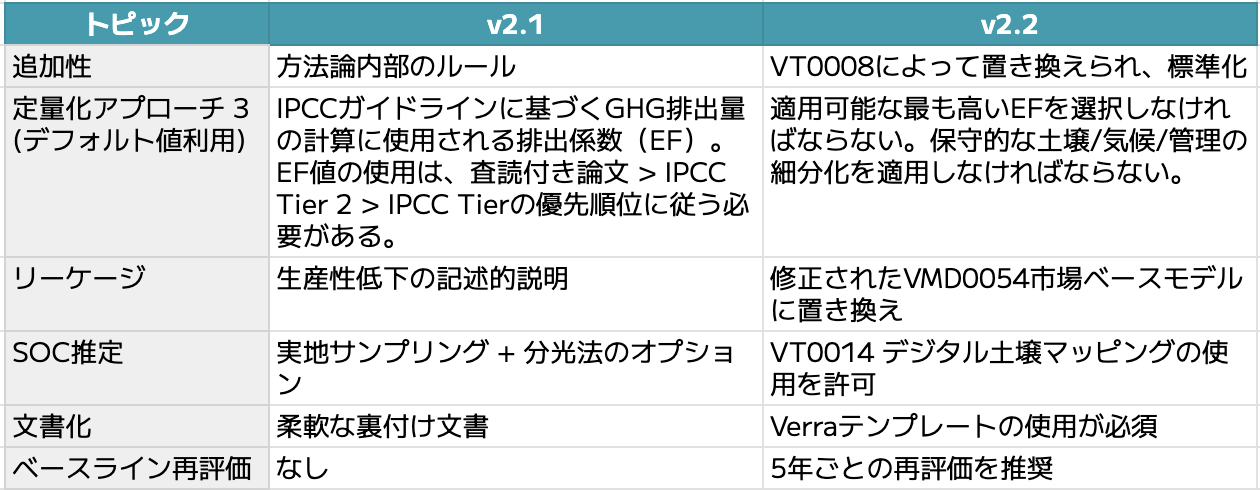

The updated VM0042 v2.2, though designated as "minor" by Verra, introduces a series of improvements that collectively enhance the technical rigor and consistency of the Methodology. These changes impact how agricultural projects demonstrate Additionality, quantify emissions, account for Leakage, and monitor Soil Organic Carbon (SOC). Table 1 provides an overview of the changes between the previous v2.1 and the updated v2.2. The following sections elaborate on some of the key changes.

Table 1: Comparison of Changes between VM0042 v2.1 and v2.2

1.1 Additionality Analysis using VT0008

Additionality determines whether project activities would not have occurred without carbon finance. For VM0042, improved agricultural practices such as No-till cultivation, optimized fertilizer use, diversified crop rotation, and improved grazing are considered additional only if they are not already Common Practice, not legally required, and not easily achievable without addressing institutional or financial barriers.

In the previous v2.1, VM0042 included its own internal procedures for Additionality assessment. Barrier Analysis relied on qualitative descriptions of cultural, social, or knowledge-related barriers, supported by research and local evidence. The Common Practice Test assessed whether the set of practices proposed by the project was commonly used in the region, but its procedures and thresholds (e.g., the 20% criterion in CDM Tool 24) were not clearly structured. This led to significant variations in interpretation across projects and sometimes ambiguous evidence requirements.

In the updated v2.2, these internal procedures have been replaced by the standardized VT0008 Additionality Assessment.

First, for Barrier Analysis, VT0008 provides:

- Definitions of barrier categories (institutional, financial, technical, and informational)

- Clear rules for documentation and consistent evidence standards

For the Common Practice Test, it establishes a two-step procedure:

- Step 1: Determine if the project activity is adopted in less than 20% of the agricultural area in the relevant region. If the adoption rate is less than 20%, the practice is considered not common (i.e., additional).

- Step 2: If the adoption rate exceeds 20%, or if adoption data is insufficient, it is necessary to consider whether there are additional socio-economic or agronomic factors preventing the widespread adoption of the project practice.